Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The risk associated with prematurely paying back the principal amount (or a portion) outstanding on a loan

Prepayment risk refers to the risk that the principal amount (or a portion of the principal amount) outstanding on a loan is prematurely paid back. In other words, prepayment risk is the risk of early repayment of a loan by a borrower.

Prepayment risk may sound counter-intuitive in that repaying a loan in a shorter period of time is considered a risk. However, to a lender, it may be preferable to have a loan outstanding for a longer period of time. To understand prepayment risk, we introduce an example.

Consider a loan with a face value of $1,000. The loan has a 10% interest rate on the face value of the loan. The borrower is to make annual interest payments over a period of three years. As such, the lender would be receiving $1,300 over the life of the loan. The loan’s payment schedule is illustrated below:

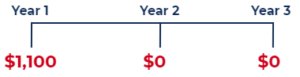

Next, assume that the borrower has the option to repay the face value amount before the end of three years. In this scenario, the borrower can theoretically repay the face value of $1,000 at the end of Year 1 and end up not having to pay interest in Years 2 and 3 (due to the face value being repaid at the end of Year 1). In doing so, the lender would only end up receiving $100 in profit on the loan. The payment schedule in this scenario is illustrated below:

As such, prepayment risk is the risk that the borrower repays the outstanding principal amount (or a portion of the outstanding principal amount) prematurely and, in turn, causes the lender to receive less in interest payments.

Mortgage-backed securities (MBS) commonly face prepayment risk. A mortgage-backed security is made up of a bundle of home loans that investors can purchase. Investors in mortgage-backed securities collect interest payments made by the underlying home loans. As such, when the homeowners repay their loans earlier than expected, investors in mortgage-backed securities face the risk of having lower future interest payments generated from the underlying home loans.

To mitigate the prepayment risk faced by investors in mortgage-backed securities, prepayment penalties are commonly imposed on homeowners who repay their home loans earlier than expected.

Although there are numerous factors that can cause a borrower to repay their loan earlier than expected, the driving factor tends to be changes in interest rates.

For example, consider a homeowner that takes out a floating-rate home loan (i.e., the interest rate on the home loan increases as market interest rate increases and vice versa).

As such, changes in interest rates play a key role in increasing the prepayment risk faced by lenders.

A homeowner takes out a mortgage at an interest rate of 15%. At the time of taking out a mortgage, the market interest rate was 15%. Two years later, the market interest rate is 10%. Explain the prepayment risk, if any, faced by the lender.

Solution: The lender faces prepayment risk on the mortgage due to the change in market interest rates from 15% to 10%. The homeowner has an incentive, assuming that there are no prepayment penalties or refinancing fees, to refinance the mortgage from an interest rate of 15% to an interest rate closer to the current market interest rate of 10%. In doing so, the lender will forego the interest payments (at the higher interest rate) that would have been made by the homeowner over the life of the mortgage.

CFI offers the Commercial Banking & Credit Analyst (CBCA®) certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant CFI resources below: