Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

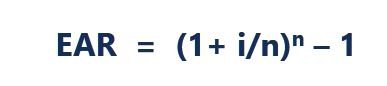

Interest rate adjusted for compounding over a given period

The Effective Annual Interest Rate (EAR) is the interest rate that is adjusted for compounding over a given period. Simply put, the effective annual interest rate is the rate of interest that an investor can earn (or pay) in a year after taking into consideration compounding.

EAR can be used to evaluate interest payable on a loan or any debt or to assess earnings from an investment, such as a guaranteed investment certificate (GIC) or savings account.

The effective annual interest rate is also known as the effective interest rate (EIR), annual equivalent rate (AER), or effective rate. Compare it to the Annual Percentage Rate (APR) which is based on simple interest.

The formula for calculating the effective annual interest rate is given below:

Where:

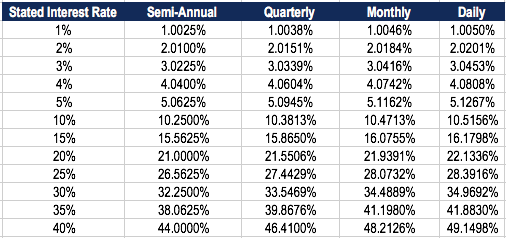

The table below shows the difference in the effective annual rate when the compounding periods change.

Table: CFI’s Fixed Income Fundamentals Course

For example, the EAR of a 1% Stated Interest Rate compounded quarterly is 1.0038%.

The effective annual interest rate is an important tool that allows the evaluation of the true return on an investment or the true interest rate on a loan.

The stated annual interest rate and the effective interest rate can be significantly different, due to compounding. The effective interest rate is important for determining the best loan or for identifying which investment offers the highest rate of return.

In the case of compounding, the EAR is always higher than the stated annual interest rate.

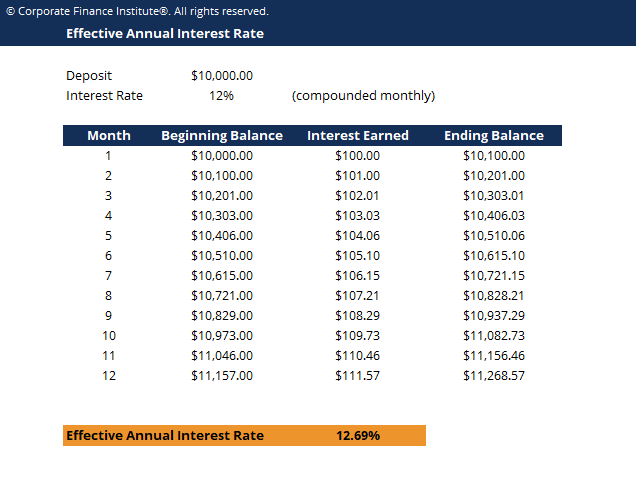

For example, assume the bank offers your deposit of $10,000 a 12% stated interest rate compounded monthly. The table below demonstrates the concept of the effective annual interest rate:

Table: CFI’s Fixed Income Fundamentals Course

Table: CFI’s Fixed Income Fundamentals Course

Month 1 Interest: Beginning Balance ($10,000) x Interest Rate (12%/12 = 1%) = $100

Month 2 Interest: Beginning Balance ($10,100) x Interest Rate (12%/12 = 1%) = $101

The change, in percentage, from the beginning balance ($10,000) to the ending balance ($11,268) is ($11,268 – $10,000)/$10,000 = .12683 or 12.683%, which is the effective annual interest rate. Even though the bank offered a 12% stated interest rate, your money grew by 12.683% due to monthly compounding.

The effective annual interest rate allows you to determine the true return on investment (ROI).

Click the button below to download CFI’s free Effective Annual Interest Rate Calculator!

To calculate the effective interest rate using the EAR formula, follow these steps:

The stated interest rate (also called the annual percentage rate or nominal rate) is usually found in the headlines of the loan or deposit agreement. Example: “Annual rate 36%, interest charged monthly.”

The compounding periods are typically monthly or quarterly. The compounding periods may be 12 (12 months in a year) and 4 for quarterly (4 quarters in a year).

For your reference:

Where:

To calculate the effective annual interest rate of a credit card with an annual rate of 36% and interest charged monthly:

1. Stated interest rate: 36%

2. Number of compounding periods: 12

Therefore, EAR = (1+0.36/12)^12 – 1 = 0.4257 or 42.57%.

When banks charge interest, they use the stated interest rate rather than the effective annual interest rate. This is done to make consumers believe that they are paying a lower interest rate.

For example, for a loan at a stated interest rate of 30%, compounded monthly, the effective annual interest rate would be 34.48%. Banks will typically advertise the stated interest rate of 30% rather than the effective interest rate of 34.48%.

When banks pay interest on your deposit account, the EAR is advertised to make the interest rate appear more attractive than the stated rate.

For example, for a deposit at a stated rate of 10% compounded monthly, the effective annual interest rate would be 10.47%. Banks will advertise the effective annual interest rate of 10.47% rather than the stated interest rate of 10%.

Essentially, they show whichever rate appears more favorable.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Effective Annual Interest Rate. To continue developing your career as a financial professional, check out the following additional CFI resources: