Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

A scenario where either the buyer or the seller has information about an aspect of product quality that the other party does not have

Adverse selection refers to a scenario where either the buyer or the seller has information about an aspect of product quality that the other party does not have. Adverse selection is a common scenario in the insurance sector, where people in high-risk lifestyles or those engaged in dangerous jobs sign up for life insurance coverage as a way of protecting themselves from impending risk.

Insurance companies, on the other hand, reduce their exposure to such high-risk claims by limiting coverage to such categories of people. Also, the insurance company can choose to raise the premium commensurately with the level of risk exposure as a way of compensating the company for the risk of covering high-risk policyholders.

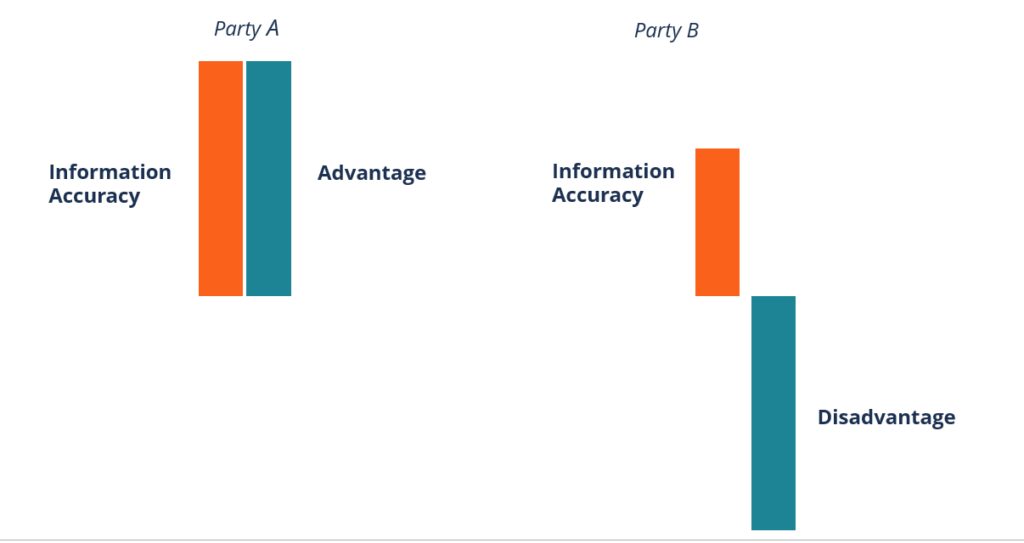

Adverse selection occurs when one party in a transaction possesses more accurate information compared to the other party. The other party, with less accurate information, is usually at a disadvantage since the party with more information stands to gain more from that transaction.

The information imbalance causes inefficiency in the price charged on specific goods or services. Such scenarios may occur in the insurance sector, capital markets, and even in the ordinary marketplaces.

To illustrate the concept of adverse selection, we can take the examples of two potential policyholders who want to take up a life insurance policy with Company ABC. The first person is diabetic and does not exercise, while the second person has no known illness and is a fitness enthusiast who exercises several times each week.

A diabetic person has a shorter life expectancy compared to a healthy person, and failure to exercise regularly increases the risk. Unless the insurance company has information on the health status of the two potential policyholders, the company will be at a disadvantage and will treat both individuals as ordinary policyholders.

During the onboarding process for new policyholders, the insurance company will ask the policyholders to fill out registration forms. The company requires potential clients to be truthful and disclose all relevant information, including health conditions that they are suffering from. Since the diabetic person is aware that disclosing his condition will attract high premiums, he may conceal the information in order to get similar treatment as the other client with no health condition.

Concealing such vital information leads to adverse selection. The insurance company will be at a disadvantage since it will enter into an agreement with a diabetic patient without knowing the health condition that the policyholder has.

Adverse selection may occur when a buyer intends to purchase a product or service from a seller, but the seller has more information about the product. Such a situation places the buyer at a disadvantage since they are entering into an agreement with a seller who may not willingly disclose all the information about the product being sold.

For example, when a buyer is looking for a second-hand car to buy, and a seller offers to sell a car with hidden defects, the buyer will be at a disadvantage unless the seller informs the buyer about the defects. Adverse selection occurs when the buyer purchases the car without the seller disclosing the defects that the vehicle has.

In the capital markets, some securities are more prone to adverse selection than others. For example, a high-growth company may offer equity to investors in the capital markets at a high price. Assuming that the managers at the capital markets have inside information about the company that outside investors are unaware of, that subjects the investor to adverse selection.

For example, the managers may be aware of an internal assessment of the company’s current value that shows that the company’s offer price exceeds the private assessment of the company. Investors will be at a disadvantage because they will purchase the company’s stock without knowing that the company is overvalued. If the managers inform the investors about the overvaluation of the company and the investors proceed to buy the stock, there will no longer be a state of adverse selection.

One of the ways that insurance companies can avoid adverse selection is by grouping high-risk individuals and charging them higher premiums. For example, insurance companies charge different premium rates to clients depending on their age, health condition, weight, medical history, hobbies, lifestyle risk (obesity, smoking, and diabetes), driving record, and occupation.

The abovementioned factors impact a person’s health and life expectancy and can determine the company’s potential to pay a claim. During underwriting, the company should determine whether to give a potential client an insurance policy and calculate the premium to charge the specific client.

To keep learning and advancing your career, the additional CFI resources below will be useful: