Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The change in the price of the bond for every 100 bps (basis points) of change in the interest rate

Dollar duration is a bond analysis method that helps an investor ascertain the sensitivity of bond prices to interest rates changes. The method measures the change in the price of a bond for every 100 bps (basis points) of change in interest rates.

Dollar duration can be applied to any fixed income products, including forwarding contracts, zero-coupon bonds, etc. Therefore, it can also be used to calculate the risk associated with such products.

The risks associated with bonds include:

The coupon rate payable on a bond is inversely related to the prevailing market interest rates. It means that as interest rates fall, bond coupon rates increase. Short-term bonds are less sensitive to interest changes, while a 20-year long-term bond may be more sensitive to interest rate changes.

Bonds with a low coupon rate are more sensitive to interest changes and vice versa. Price risk is more relevant to investors intending to hold the bond for a short period of time and resell it before it matures.

The return that can be earned by reinvesting the coupon payments is positively or directly correlated with the market rate of interest. It is more relevant for investors intending who intends to hold the bond until maturity, as when rates go up, the investor will earn more.

Since both risks move in opposite directions and offset each other, a duration that minimizes the exposure to both risks and maximizes the profit that can be earned can be calculated. The duration refers to the holding period where price risk and reinvestment rate risk offset each other.

Dollar duration is represented by calculating the dollar value of one basis point, which is the change in the price of a bond for a unit change in the interest rate (measured in basis points). The dollar value per 100 basis point can be symbolized as DV01 or Dollar Value Per 01. A 1% unit change in the interest rate is 100 basis points.

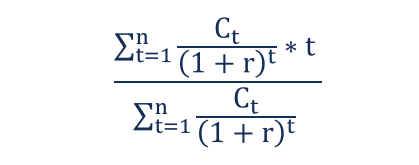

The formula for calculating duration is:

Where:

The formula for calculating dollar duration is:

Alternatively, if the change in the value of the bond and the yield is known, another formula can be used:

Where:

Dollar duration is not an accurate measure of the effect of interest rates on bond prices, as the relationship between the two is not linear. It means that the aforementioned formulas can accurately predict price changes in bonds for given interest rates only for small changes.

To keep learning and developing your knowledge base, please explore the additional relevant resources below: