Get Certified for

Business Intelligence (BIDA®)

Develop analytical superpowers by learning how to use programming and data analytics tools such as VBA, Python, Tableau, Power BI, Power Query, and more.

The mathematical formula for bet sizing frequently used by investors

The Kelly Criterion is a mathematical formula for bet sizing, which is frequently used by investors to decide how much money they should allocate to each investment or bet through a predetermined fraction of assets. It is popular because it typically leads to higher wealth in the long run compared to other types of strategies.

The Kelly Criterion was developed in 1956 by an American scientist, John L. Kelly, who worked as a researcher at AT&T’s Bell Labs in New Jersey. Kelly originally developed the formula to help the company with its long-distance telephone signal noise issues.

Later, it was picked up by the betting community, who realized its value as an optimal betting system since it would allow gamblers to maximize the size of their earnings.

Although it was reported that Kelly never used his formula for personal gain, it is still quite popular today and is used as a general money management system for investing. One reason behind its popularity is how frequently it is used by prominent investors, such as Warren Buffett of Berkshire Hathaway.

Investors often face a tough decision when trying to decide how much money to allocate, as staking either too much or too little will result in a large impact either way.

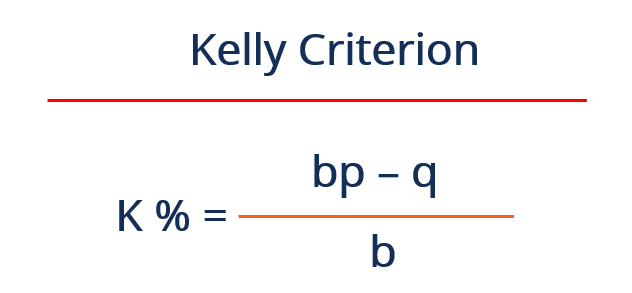

The Kelly criterion is a money-management formula that calculates the optimal amount to ensure the greatest chance of success. The formula is as follows:

Where:

When a dice is thrown, the chance of it landing on a 1, 2, or 3 is 50%, while the same percentage applies to an outcome of 4, 5, or 6.

Now, let us imagine that the dice can rest on a 1, 2, or 3 with a probability of 60%, meaning the probability of it landing on 4, 5, or 6 is 40%. The variables will look as follows:

Based on the Kelly criterion, K% = (1 × 0.60 – 0.40) / 1 = 0.20 or 20%

The formula is, therefore, suggesting that 20% of the portfolio be staked 20% of your bankroll. If the dice bias was less, at 53%, the Kelly criterion recommends staking 6%.

In such a case, the Kelly criterion suggests that if one were to go over 20% repeatedly on a low number, there is a high chance one would eventually go broke.

Under-betting less than 20%, on the other hand, would lead to a smaller profit, which means that adhering to the Kelly criterion will maximize the rate of capital growth for the long term.

The Kelly Criterion results in the K%, which refers to a percentage that represents the size of the portfolio to devote to each investment. Basically, the Kelly percentage provides information on how much one should diversify.

One should not commit more than 20% to 25% of the capital into single equity regardless of what the Kelly criterion says since diversification itself is important and essential to avoid a large loss in the event a stock fails.

Some investors prefer to bet less than the Kelly percentage due to being risk-averse, which is understandable, as it means that it reduces the impact of possible over-estimation and depleting the bankroll. It is known as Fractional Kelly.

On the other hand, if the Kelly percentage results in a percentage less than 0%, it means that the Kelly Criterion recommends that one walk away and not bet anything at all since the odds do not seem to be in one’s favor based on the formula and mathematical calculation.

Following the Kelly criterion typically results in success due to the formula is based on a simple formula using pure mathematics.

However, factors that can impact success include accurate inputs of the probabilities of winning and losing, as an incorrect percentage would be detrimental.

In addition to that, there may be unexpected events, such as stock market crashes, which would impact all stocks regardless if the Kelly Criterion was used or not.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Kelly Criterion. The following CFI resources will help further your financial education and advance your career: