L Bond

An unrated life insurance bond that finances the purchase and premium payments of life insurance contracts

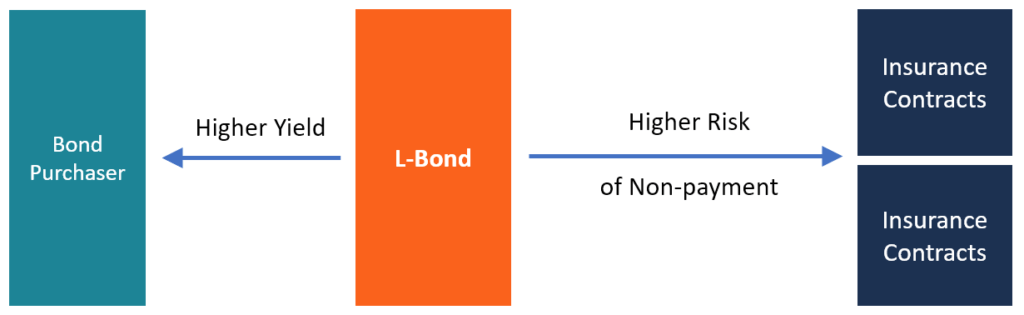

What is an L Bond?

An L Bond refers to an unrated life insurance bond that finances the purchase and premium payments of life insurance contracts bought in the secondary market. The bond offers a higher yield than other publicly traded offerings to compensate for the risk that the insurance policy benefits may not be paid. People buy life insurance policies from insurance providers with the goal of protecting their beneficiaries after they die. The protection may be in the form of monetary compensation to bridge the gap left by the policyholder.

The policyholder may decide to sell the policy in the secondary market when they are unable to continue paying the insurance premiums, no longer need the insurance protection, or are in need of urgent cash flow. The person who purchases the policy now becomes the beneficiary. When the original policyholder dies, the buyer will receive compensation from the insurer.

After the purchase, the buyer is now responsible for making the premium payments to the insurance carrier. The buyer purchases the life insurance policy for more than the surrender value but less than the benefits expected. The buyer profits from the transaction by aligning the expected returns/benefits with the life expectancy of the original policyholder.

How an L Bond Works

Minnesota-based company GWG Holdings, the parent company of GWG Life, buys life settlements contracts from policyholders at prices that exceed the surrender value. The company finances these purchases through the sale of high-yield bonds to buyers looking to invest in instruments that have a higher yield.

GWG Holdings sells unrated bonds, which therefore come with a higher risk. According to the firm’s fact sheet, L Bonds are considered speculative and are subject to a higher degree of risk.

Maturities of L Bonds

L Bonds come with maturities ranging from two to seven years. Previously, GWG offered bonds with 6-month and 1-year maturities, but the company stopped that practice in September 2016. The bonds are illiquid, so investors must wait until maturity to access their investments.

Preferred Stock

GWG Holdings also issues preferred stocks that pay a dividend of 7% and come with a conversion option. The issuer can recall them before the maturity date and their proceeds correlate to the life insurance policy purchased from the original policyholders. In a situation where the insurance provider goes bankrupt, the company may be unable to make timely dividend payments. This will affect the prices of its offerings.

Attractiveness of L Bonds

Although these bonds come with a high degree of risk, they are attractive to investors due to their high yields. Also, unlike other alternative investments that are highly correlated to certain segments of the market, they are not correlated to the equity or fixed income markets.

Characteristics of L Bonds

- Investors can purchase the bonds from GWG Holdings or a Depository Trust Company participant.

- The bonds are sold in denominations of $1,000. The minimum amount that an investor can purchase is $25,000.

- They are illiquid investments, and the holders cannot sell them on the secondary market. They need to wait until the bonds mature to redeem the principal amount. It is highly unlikely that these bonds can be purchased in the secondary market.

- The interest rate for a bond remains fixed for the entire term of the bond, even if the market interest rates change.

- The bonds are callable. The issuer possesses the right to recall the bond at any time before the maturity date without a penalty. This may occur when market interest rates fall below the interest rate offered by the bonds.

- Holders cannot redeem the bond before the maturity date or the death or disability of the original policyholder. However, if GWG agrees to redeem the bond for any other reason, the bondholder will be charged a penalty of 6%.

- Upon maturity, the bond is automatically renewed unless the bondholder decides to redeem the bond.

- The bonds do not correlate to equity or fixed income markets, and their value is not affected by the volatility of the financial markets.

How GWG Holdings Operates

GWG Holdings is a leading issuer of the high-yield bonds. The company purchases life insurance settlement contracts from seniors in order to make money. For example, the firm may purchase a 5-year $5-million life insurance policy that pays $100,000 a year for $1 million. When the policy matures, or the seller dies, the insurance provider pays GWG Holdings $5 million in life insurance settlements. The funds raised from the policy are used to purchase additional life insurance assets.

The first GWG L Bond issue was in August 2012 for a $250 million offering. The issue was fully subscribed by December 2014. The firm issued the second offering of $1 billion in January 2015 with maturities of 2 to 7 years. In total, the company sold over $400 million worth of bonds through its independent broker-dealer channel of over 5,000 advisors.

The company also entered into an arrangement where the bonds are available through Depository Trust Company. In 2016, GWG announced that it held over 500 policies with total insurance assets valued at $1.15 billion.

Summary

An L Bond is an investment vehicle that offers high yields to compensate investors for the risk that the insurance premiums or benefits may not be paid. It is used to finance the purchase and premium payments of insurance contracts purchased in the secondary market.

Other resources

CFI is a global provider of the Financial Modeling & Valuation Analyst (FMVA)® certification program for finance professionals. To learn more and expand your career, explore the additional relevant resources below: