Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The weighted average of the time to receive the cash flows from a bond

Macaulay duration is the weighted average of the time to receive the cash flows from a bond. It is measured in units of years. Macaulay duration tells the weighted average time that a bond needs to be held so that the total present value of the cash flows received is equal to the current market price paid for the bond. It is often used in bond immunization strategies.

In Macaulay duration, the time is weighted by the percentage of the present value of each cash flow to the market price of a bond. Therefore, it is calculated by summing up all the multiples of the present values of cash flows and corresponding time periods and then dividing the sum by the market bond price.

Where:

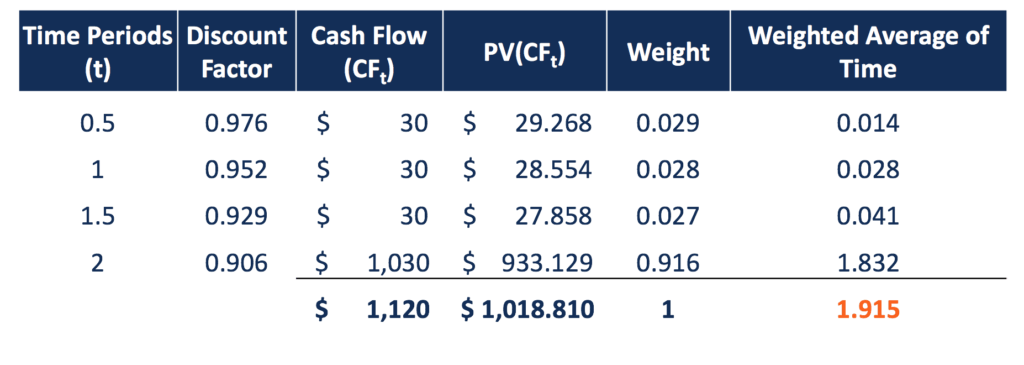

For example, a 2-year bond with a $1,000 par pays a 6% coupon semi-annually, and the annual interest rate is 5%. Thus, the bond’s market price is $1,018.81, summing the present values of all cash flows. The time to receive each cash flow is then weighted by the present value of that cash flow to the market price.

The Macaulay duration is the sum of these weighted-average time periods, which is 1.915 years. An investor must hold the bond for 1.915 years for the present value of cash flows received to exactly offset the price paid.

The Macaulay duration of a bond can be impacted by the bond’s coupon rate, term to maturity, and yield to maturity. With all the other factors constant, a bond with a longer term to maturity assumes a greater Macaulay duration, as it takes a longer period to receive the principal payment at maturity. It also means that Macaulay duration decreases as time passes (term to maturity shrinks).

Macaulay duration takes on an inverse relationship with the coupon rate. The greater the coupon payments, the lower the duration is, with larger cash amounts paid in the early periods. A zero-coupon bond assumes the highest Macaulay duration compared with coupon bonds, assuming other features are the same. It is equal to the maturity for a zero-coupon bond and is less than the maturity for coupon bonds.

Macaulay duration also demonstrates an inverse relationship with yield to maturity. A bond with a higher yield to maturity shows a lower Macaulay duration.

Modified duration is another frequently used type of duration for bonds. Different from Macaulay duration, which measures the average time to receive the present value of cash flows equivalent to the current bond price, Modified duration identifies the sensitivity of the bond price to the change in interest rate. It is thus measured in percentage change in price.

Modified duration can be calculated by dividing the Macaulay duration of the bond by 1 plus the periodic interest rate, which means a bond’s Modified duration is generally lower than its Macaulay duration. If a bond is continuously compounded, the Modified duration of the bond equals the Macaulay duration.

In the example above, the bond shows a Macaulay duration of 1.915, and the semi-annual interest is 2.5%. Therefore, the Modified duration of the bond is 1.868 (1.915 / 1.025). It means for each percentage increase (decrease) in the interest rate, the price of the bond will fall (raise) by 1.868%.

Another difference between Macaulay duration and Modified duration is that the former can only be applied to the fixed income instruments that will generate fixed cash flows. For bonds with non-fixed cash flows or timing of cash flows, such as bonds with a call or put option, the time period itself and also the weight of it are uncertain.

Therefore, looking for Macaulay duration, in this case, does not make sense. However, Modified duration can still be calculated since it only takes into account the effect of changing yield, regardless of the structure of cash flows, whether they are fixed or not.

In asset-liability portfolio management, duration-matching is a method of interest rate immunization. A change in the interest rate affects the present value of cash flows, and thus affects the value of a fixed-income portfolio. By matching the durations between the assets and liabilities in a company’s portfolio, the change in interest rate will move the value of assets and the value of liabilities by exactly the same amount, but in opposite directions.

Therefore, the total value of this portfolio remains unchanged. The limitation of duration-matching is that the method only immunizes the portfolio from small changes in interest rate. It is less effective for large interest rate changes.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Macaulay Duration. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: