Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A note payable that comes with a maturity within five to ten years

A medium-term note (MTN) usually refers to a note payable that comes with a maturity date that is within five to ten years.

A note, or note payable, is a legal document that represents an amount owed from a borrower to a lender or investor. Notes generally include a principal amount, or face value, that is lent to the borrower and is expected to be repaid at a later date, in addition to scheduled interest payments. Notes can be thought of as a form of fixed income security that is similar to a bond.

The notes can be issued by various organizations and entities, including federal governments, state or provincial governments, municipal governments, corporations, non-profit organizations, etc.

Examples of notes include:

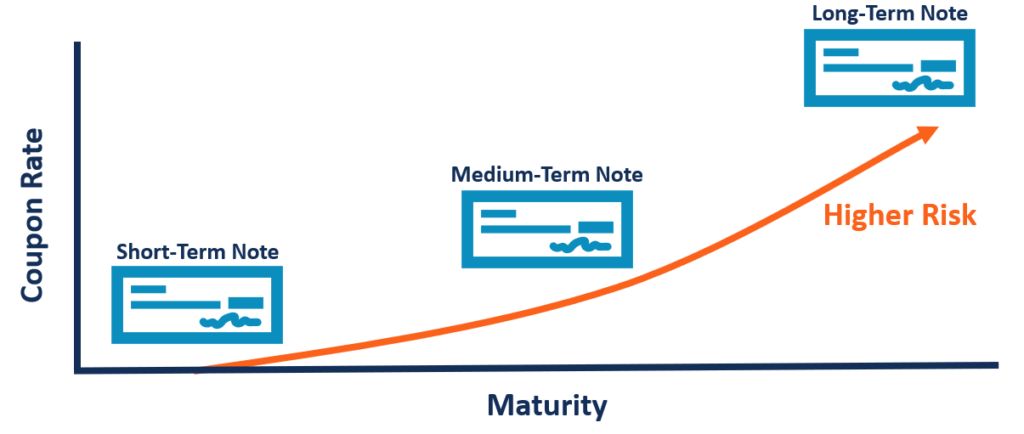

In order to distinguish medium-term notes from other notes, the definition of “medium term” must be identified. Generally, when comparing fixed-income securities, all else being equal, medium-term notes will come with a higher stated rate or coupon rate than shorter-term notes.

It is because, to compensate for the risks associated with lending money for a longer period of time, an investor will demand a higher yield. Following that logic, a long-term note will generally offer a higher stated rate than a medium-term note.

Various organizations or corporations may issue MTNs and can continuously offer the notes through a dealer. A dealer represents market actors who buy and sell securities from their own account to provide liquidity and make markets within the securities markets.

It is in contrast to brokers, who buy and sell securities on behalf of another party. Investors can select different maturities ranging from short term (less than a year) to long term (30+ years). However, medium-term notes are distinguished by offering a maturity of five to ten years.

Investors may prefer medium-term notes if they match the time horizon that the investors are seeking. Some investors may not need capital in the short term but may eventually need funds in the long term. The investors may want higher yields than short-term notes but may still require liquidity in the long term.

For the investors, medium-term notes are an ideal alternative since they offer a higher interest rate than short-term investments and are preferable as opposed to continuously renewing low-yield, short-term investments.

Making repeated short-term investments exposes investors to reinvestment risk, which is the risk that an investor may not be able to reinvest cash flows at the desired rate of return. The risk is more pronounced in an economic environment with decreasing interest rates. Medium-term notes allow investors to remove this risk in the medium term and lock in a specific yield over the life on the investment.

Medium-term notes offer investors the advantage of offering a wider range of investment options to choose from. Investors looking to invest within the medium-term notes market can choose among several investment options regarding the nature, size, and time length of the investment.

Issuers of medium-term notes can benefit from the consistent cash flow generation provided by offering the notes to investors. It allows issuers to issue notes as needed to meet their financing needs. For example, if a company needs to fund a large upcoming project but is short on cash, it can issue medium-term notes to investors to raise funds at a lower cost than issuing a long-term note.

Issuers also retain the flexibility to issue notes with embedded options such as call options.

A call option on a note is also referred to as a callable note or redeemable note, and it allows the issuer to redeem a note before its stated maturity date. Essentially, it gives an issuer more flexibility if they wish to pay off their debt early.

It may be ideal in an environment when interest rates are decreasing, since an issuer can repay the note, then either refinance or issue a new note at a lower interest rate. Because of the flexibility, investors typically demand a higher interest rate on a callable note, as opposed to a non-callable note, to compensate for the risk that an issuer may redeem the note early.

Thank you for reading CFI’s guide on Medium-Term Note (MTN). To keep advancing your career, the additional CFI resources below will be useful: