Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Fixed income securities are a broad class of very liquid and highly traded debt instruments, the most common of which is a bond.

Fixed income securities are a broad class of very liquid and highly traded debt instruments, the most common of which is a bond. They generally provides returns in the form of regular interest payments and repayments of the principal when the security reaches maturity.

They are different from equities, or stocks, since fixed income securities do not represent an ownership interest in a company, but they confer a seniority of claim, as compared to equity interests, in cases of bankruptcy or default.

The instruments are issued by governments, corporations, and other entities to finance their operations. Investors buy fixed income securities to provide a predictable cashflow and to provide diversification from stocks and other asset classes.

The term fixed income refers to the interest payments that an investor receives, which are based on the creditworthiness of the borrower and current interest rates.

Generally speaking, fixed income securities such as bonds pay a higher interest, known as the coupon, the longer their maturities. This is because borrowers are willing to pay more interest in return for being able to borrow the money for a longer period of time and investors demand higher rates to commit their savings for a longer amount of time.

At the end of the security’s term or maturity, the borrower returns the borrowed money, known as the principal or “par value.” The illustration below shows the cash flows that an investor might receive if they purchase a 3 year bond (where t denotes the time in years).

The most common type of fixed income security is a bond, both issued by companies and government entities, but there are many examples of fixed income securities as money market instruments, asset-backed securities, preferreds and derivatives.

The topic of bonds is, by itself, a whole area of financial or investing study. In general terms, they can be defined as loans made by investors to an issuer, with the promise of repayment of the principal amount at the established maturity date, as well as regular coupon payments (generally occurring every six months), which represent the interest paid on the loan. The purpose of such loans ranges widely. Bonds are typically issued by governments or corporations that are looking for ways to finance projects or operations.

Money market instruments include securities such as commercial paper, banker’s acceptances, certificates of deposit (CD), repurchase agreements (“repo”) and the most traded, US Government Treasury Bills, called T-bills for short.

Considered the safest short-term debt instrument, Treasury bills are issued by the US federal government. With maturities ranging from one to 12 months, these securities most commonly involve 28, 91, and 182-day (one month, three months, and six months) maturities. These instruments offer no regular coupon, or interest, payments.

Instead, they are sold at a discount to their face value, with the difference between their market price and face value representing the interest rate they offer investors. As a simple example, if a Treasury bill with a face value, or par value, of $100 sells for $90, then it is offering roughly 10% interest.

Asset-backed Securities (ABS) are fixed income securities backed by financial assets that have been “securitized,” such as credit card receivables, auto loans, or home-equity loans. ABS represents a collection of such assets that have been packaged together in the form of a single fixed-income security. For investors, asset-backed securities are usually an alternative to investing in corporate debt.

Sometimes called Subordinated Debt, these type of fixed income securities rank lower on the capital stack. Preferred fixed income securities may not pay their coupon or principal should the creditworthiness of the issuer deteriorate. This risk is called loss-absorption and hence Preferreds are sometimes viewed as a hybrid security between fixed income and equities.

In capital markets, there have been many financial contracts that have different payoffs depending on how other securities behave. These are called “Derivatives” and in fixed income, we see these derivatives such as swaps, options, and structured products actively traded for speculation, hedging, and getting access to additional assets or markets.

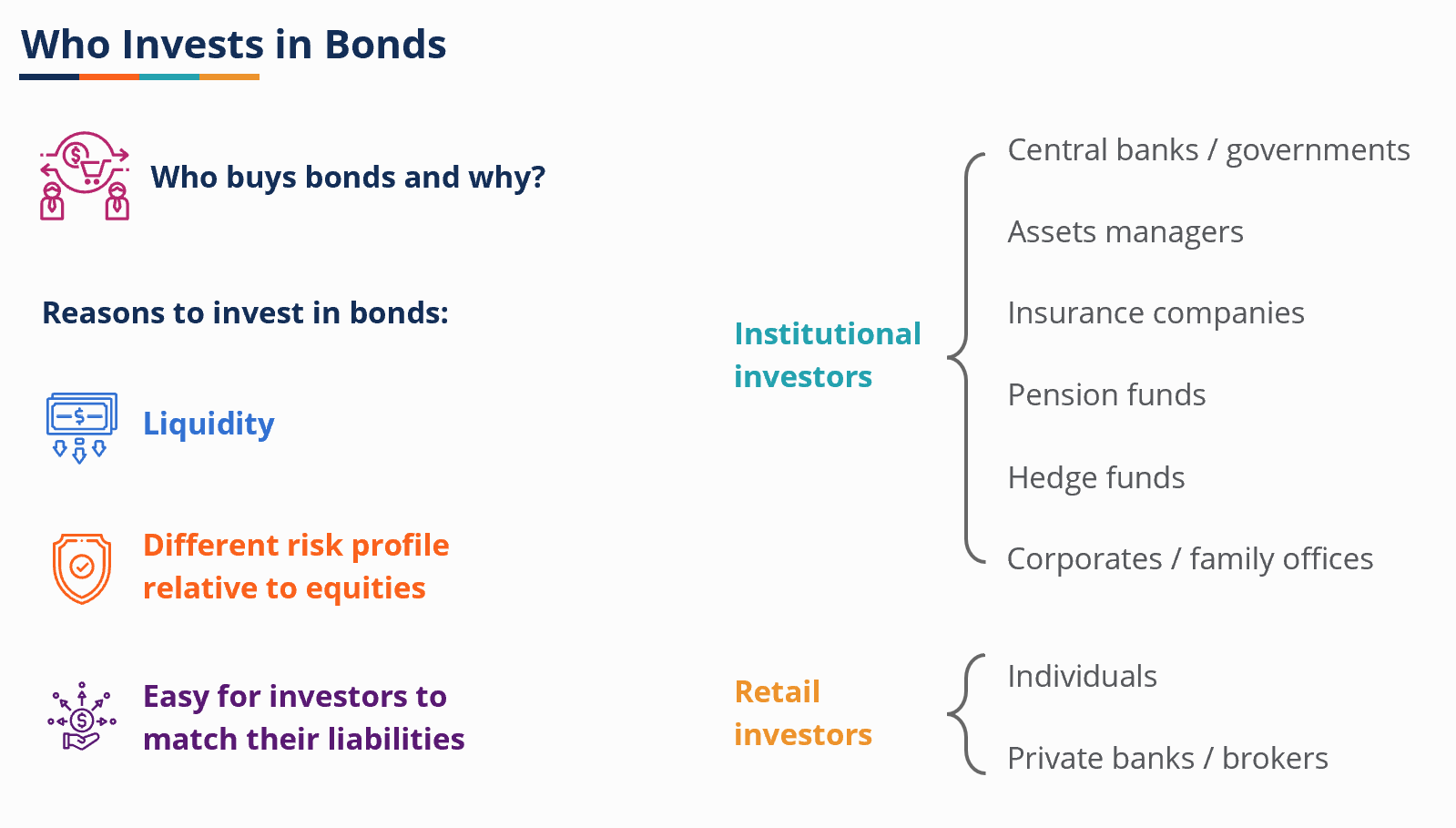

Institutional Investors and Retail Investors both invest in Fixed Income Securities. Each one of these types of investors has different considerations when investing in fixed income, though.

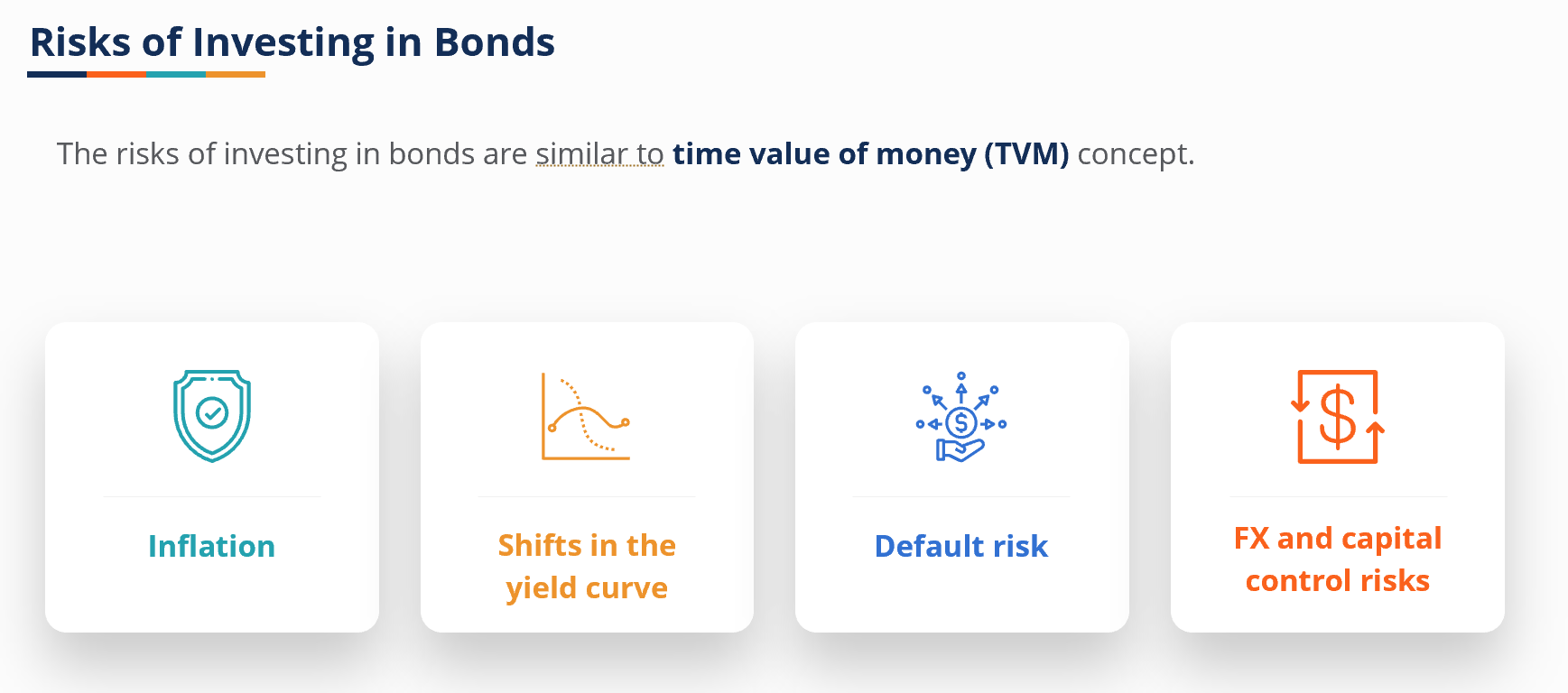

It is important to remember that while certain types of bonds are low-risk, bonds are not always less risky than equities.

In general, investors in Fixed Income Securities face four major risks:

Thank you for reading CFI’s guide to Fixed Income Securities. To keep advancing your career, the additional CFI resources below will be useful: