Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

How a company prioritizes the repayment of its debts

Senior and subordinated debt refers to their rank in a company’s capital stack. In the event of a liquidation, senior debt is paid out first, while subordinated debt is only paid out if funds remain after paying off senior debt. To compensate an investor for the risk, subordinated debt has a higher interest rate than senior debt.

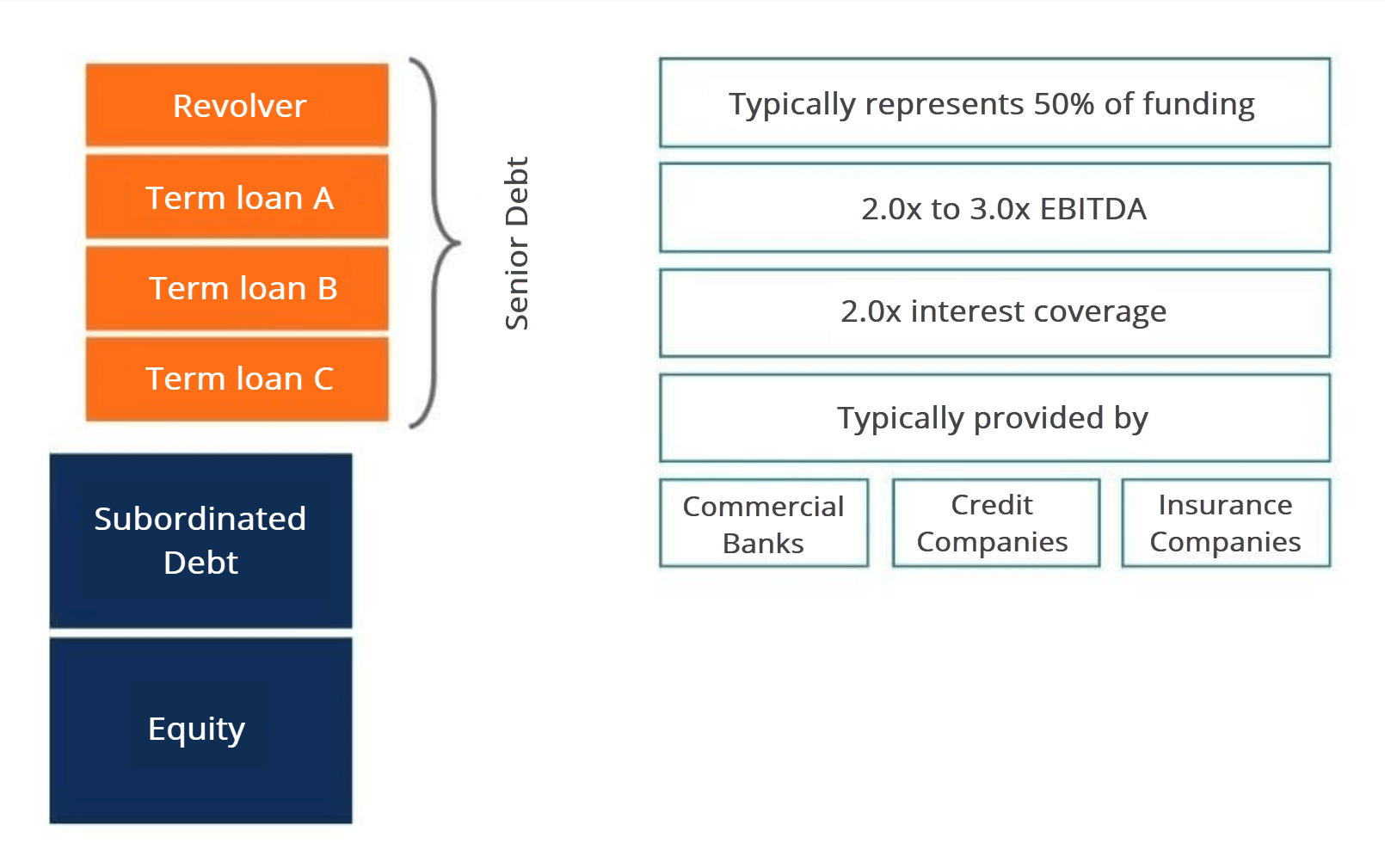

In order to understand senior and subordinated debt, we must first review the capital stack. Capital stack ranks the priority of different sources of capital, including senior debt, subordinated debt, and equity. The stack exhibits two findings.

First, senior debt creditors will be paid first in the event of financial distress, while shareholders will divide what remains after all creditors are paid. Secondly, the return profile of debt and equity is inverse to the priority list. Shareholders with an equity stake have the highest return profile, whereas senior debt creditors have the lowest.

There are a few main components in senior debt. Typically, companies have a revolving line of credit facility and various tranches of term loans. The entire senior debt portion commonly accounts for 50% of funding in an acquisition, which roughly equates to two to three times debt to EBITDA or twice the interest coverage.

For example, if a company’s EBITDA is stable and reliable, perhaps banks would lend the company two to three times its EBITDA for its senior debt. Another example would require the company to generate sufficient cash flow to cover the interest expense of senior debt twice over.

Common senior debt lenders include commercial banks, credit companies, and insurance companies.

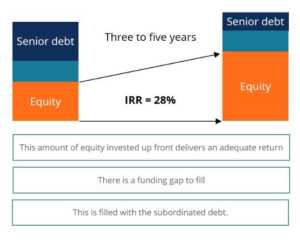

How does debt affect equity returns? An investor can use senior and subordinated debt to enhance equity returns. Over time, as a business grows, the original capital structure of a company also changes. Let’s assume that the capital stack in the first year was 40% senior debt, 20% subordinated debt, and 40% equity. How will this change over a time horizon of three to five years?

As the business grows and expands, the equity piece will grow significantly over the next three to five years. The subordinated debt piece will remain the same, while the senior debt piece will shrink, as its principal has been repaid over its amortization period.

Hence, the value of the business has grown, but the majority of that growth has only been transferred to shareholders. This growth rate in equity is how private equity firms generate an Internal Rate of Return (IRR). The standard IRR range is usually between 20% to 30% return.

From the point of view of a private equity firm, it is important that the amount of equity invested upfront delivers an adequate return. However, if a funding gap exists, it is usually filled with subordinated debt.

To learn more about debt modeling, the use of leverage, and calculating IRR, please see our financial modeling courses.

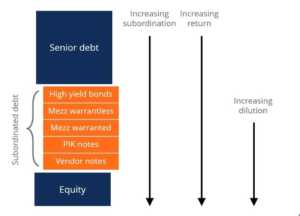

Continuing our discussion of senior and subordinated debt, let’s move down the capital stack to subordinated debt, which is considered any type of debt that will not be paid until all senior debt is paid in full. However, even within subordinated debt, there are various types of loans with different priorities.

Types of subordinated debt include high yield bonds, mezzanine with and without warrants, Payment in Kind (PIK) notes, and vendor notes, ordered from the highest to the lowest priorities, respectively. In some private-equity transactions or closely held firms, the “debt” portion may include a shareholder loan (subordinated debt) that ranks below senior bank debt in the capital stack.

Another way to express the different priorities of securities is with a subordination scale. For example, high-yield bonds have the lowest subordination, while vendor notes have the highest.

For varying levels of subordination, there are varying levels of expected return. Therefore, investors make decisions based on this risk and reward tradeoff.

For instance, high yield bond investors have the highest priority to collect debt in case of financial distress, but will incur the lowest return out of all subordinated debt creditors. On the other hand, vendor note creditors have the lowest priority to collect debt but will incur the highest expected return out of all lenders.

Finally, with increasing subordination comes increasing equity dilution. Thus, it is important for management to seek sources of capital at the top of the capital stack to minimize equity dilution.

A business can only take on so much debt. So how much subordinated debt can a company handle?

There are several measures to typically estimate a company’s maximum subordinated debt:

The appropriate capital structure must be constructed within these constraints.

High yield bonds are publicly traded securities, allowing for transactions in a secondary market. However, mezzanine finance is not tradeable.

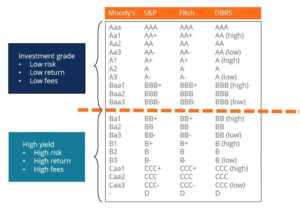

In order to understand the risks of purchasing bonds, credit rating agencies provide credit scores on each bond based on their evaluation of default risk. Bonds with AAA rating are the most secure, with the lowest probability of default, whereas bonds with D rating are the least secure, with the highest probability of default.

Moreover, bonds with a rating of BBB- and higher are considered investment grade, while those with a rating of BB+ or lower are classified as non-investment grade, high-yield, or junk bonds.

Mezzanine debt is a non-tradeable security, which is subordinated to senior debt. It often has a bullet repayment, accrued cash return, and can have equity warrants attached. Equity warrants provide lenders with exposure to equity upside on top of the expected return on the actual interest payments.

Also, mezzanine debt includes convertible loan stocks, which can be converted entirely into equity, or convertible preferred shares, which can be converted entirely into preferred shares.

Debt with warrants, convertible loan stocks, and convertible preference shares all have equity exposures built into the debt security.

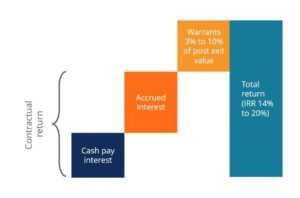

Mezzanine lenders typically target an Internal Rate of Return (IRR) of 15% to 20%. The IRR consists of several components. The first is the cash interest that is paid by the company to the investor. The second piece is the accrued interest, which is interest accrued to be repaid with the principal.

The above two components comprise the contractual returns that the company owes to the creditors. The final component is the upside equity exposure from warrants. These warrants are typically 3% to 10% of the post-exit value of the business, which significantly increases the IRR of a debt investor.

Thank you for reading this guide to senior and subordinated debt. To keep learning and advancing your career, we highly recommend these additional CFI resources below: