Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The probability of a decline in the value of an asset resulting from unexpected fluctuations in the interest rate

Interest rate risk is the probability of a decline in the value of an asset resulting from unexpected fluctuations in interest rates. Interest rate risk is mostly associated with fixed-income assets (e.g., bonds) rather than with equity investments. The interest rate is one of the primary drivers of a bond’s price.

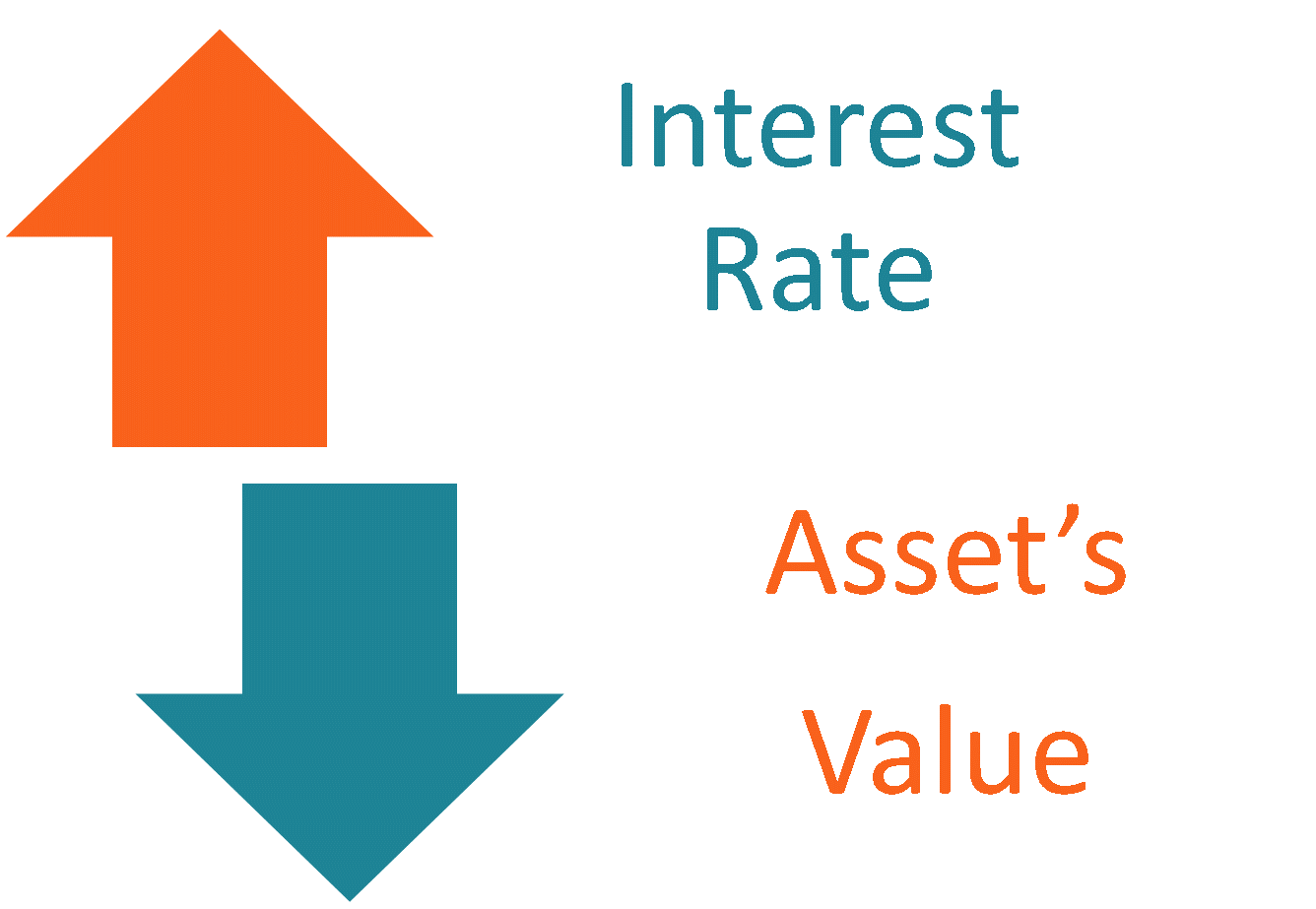

The current interest rate and the price of a bond demonstrate an inverse relationship. In other words, when the interest rate increases, the price of a bond decreases.

The inverse relationship between the interest rate and bond prices can be explained by opportunity risk. By purchasing bonds, an investor assumes that if the interest rate increases, he or she will give up the opportunity of purchasing the bonds with more attractive returns. Whenever the interest rate increases, the demand for existing bonds with lower returns declines as new investment opportunities arise (e.g., new bonds with higher return rates are issued).

Although the prices of all bonds are affected by interest rate fluctuations, the magnitude of the change varies among bonds. Different bonds show different price sensitivities to interest rate fluctuations. Thus, it is imperative to evaluate a bond’s duration while assessing the interest rate risk.

Generally, bonds with a shorter time to maturity carry a smaller interest rate risk compared to bonds with longer maturities. Long-term bonds imply a higher probability of interest rate changes. Therefore, they carry a higher interest rate risk.

Similar to other types of risks, interest rate risk can be mitigated. The most common tools for interest rate mitigation include:

If a bondholder is afraid of interest rate risk that can negatively affect the value of his portfolio, he can diversify his existing portfolio by adding securities whose value is less prone to interest rate fluctuations (e.g., equity). If the investor has a “bonds only” portfolio, he can diversify the portfolio by including a mix of short-term and long-term bonds.

The interest rate risk can also be mitigated through various hedging strategies. These strategies generally include the purchase of different types of derivatives. The most common examples include interest rate swaps, options, futures, and forward rate agreements (FRAs).

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Interest Rate Risk. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: