Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A cost incurred by an employee running official business functions at a home office

A home office expense refers to the costs incurred through the performance of business activities within a primary residence. When work performed in the home office produces outside income, the Internal Revenue Service allows business owners to make a tax deduction from the annual tax return if they meet certain requirements. Examples of office expenses may include the internet bill, phone lines, utilities, cost of stationery, taxes, etc.

Home office expenses enable self-employed business owners to claim a tax deduction from their annual tax returns for house expenses such as property taxes and mortgage interests. The house expenses can also include additional running costs ranging from an internet subscription to electricity bills. Most often, employees working from home bear zero capital gains tax (CGT) implications for their homes.

Fully deductible utilities are those that are exclusively used to conduct business. For example, computer equipment, phone lines, and office supplies constitute home office expenses. The deductible amounts are determined by several factors – such as homeowner’s earnings and tax remittance. However, home office expense is commonly claimed as an expense as long as they accrue in the course of a business operation.

To claim home office expenses, an individual must exclusively and regularly use the space in question for conducting business. Exclusive use means the office space is meant for nothing other than conducting business. In contrast, regular use implies that the room is utilized regularly, rather than on certain occasions. Under such a framework, a home office must meet either of the following criteria:

A home office does not necessarily need to be permanent, and using such space for the dual purpose of business and personal use disqualifies it from being a home office. A home office can be located in the corner of the house, with arrangements only used to transact business. However, conducting business using a laptop while sitting on the sofa among family members does not qualify for a home office.

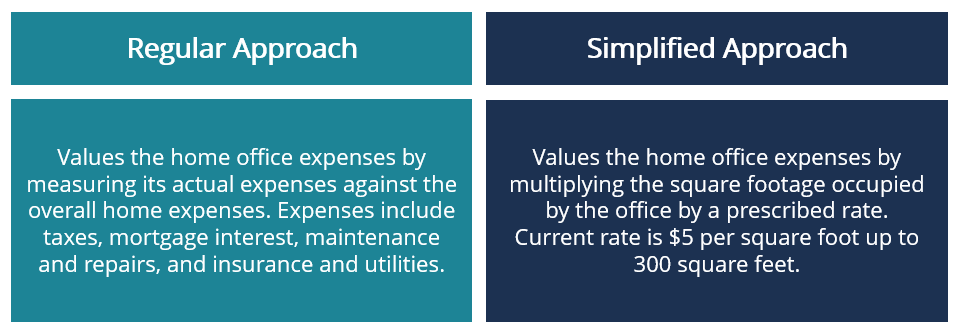

According to the IRS, two approaches are used to calculate the number of deductions and how much space constitutes a home office. One of such methods is the regular method, which involves calculating expenses. The second method is the simplified method, which is relatively ineffective since it may not yield a wide range of deductions.

The regular method requires accurate record-keeping, and the accounting of home expenses starts by finding the following:

Direct expenses are utilities such as aesthetics or renovations in the areas only meant for business. On the other hand, indirect expenses are the costs incurred from general repairs, utilities, and insurance premiums. The IRS further provides the following two methods to establish the allowable portion of a home:

The simplified method is appropriate, especially if a home office is on the small side. The following criteria are considered when calculating home office expenses using the simplified approach:

The forbearing information can be used to calculate home expense deductions by following the procedure below:

However, there are limitations to the above method. For example, in the case of a shared space, they both cannot be deducted. Publication 587 includes additional restrictions of the simplified approach.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: