De Minimis Tax Rule

A law that governs the treatment and accounting of small market discounts

What is the De Minimis Tax Rule?

The de minimis tax rule is a law that governs the treatment and accounting of small market discounts. Translated “about minimal things,” the de minimis amount determines whether the market discount on a bond is taxed as capital gain or ordinary income.

The de minimis tax rule states that if a discount is less than 0.25% per year between the time purchased and maturity, the discount is considered too small and tax-exempt.

Capital Gain Tax vs. Ordinary Income Tax

Capital Gains Tax (CGT): The capital gains tax is a form of tax applied when profit is gained from the sale of non-inventory assets such as bonds and property. In the U.S., short-term capital gains (assets purchased and sold within a year) are taxed the same as ordinary income tax and more heavily than long-term capital gains.

Ordinary Income Tax: The ordinary income tax is a form of tax applied to a variety of items, such as salaries, wages, commissions, etc. Apart from the basic forms of income, ordinary income tax can be applied to dividends, partnerships, royalties, and even gambling winnings.

How to Determine which Form of Tax is Paid

Below are the mathematical steps needed to be taken when determining if a bond is subject to capital gain tax or ordinary income tax regarding the de minimis rule.

1. Multiply the face value (bond price when issued) by 0.25%.

2. Take the result above and multiply it by the number of full years between the time you purchased the discounted bond and its maturity.

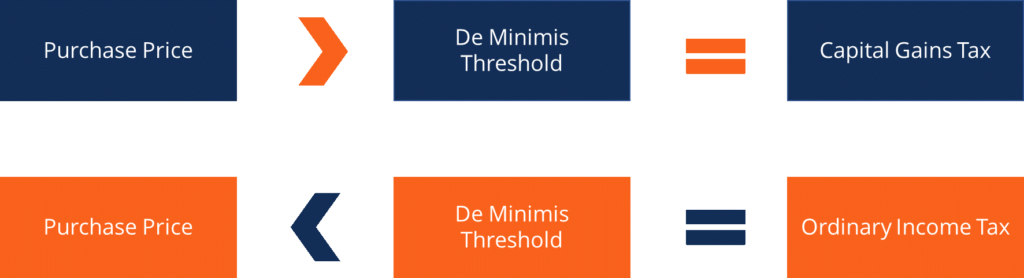

3. Subtract the result from face value. It will determine the minimis threshold. The diagram below depicts how purchase price and de minimis threshold correlate to taxation.

Example with Calculation

You are given a 15-year bond with a face value of $1,500, and it matures in six years. What form of tax will be applied once the bond is sold? The steps are shown below:

1. $1,500 x .0025 = $3.75

2. $3.75 * 6 years = 22.50

3. $1,5000 – $22.75 = $1,447.50 (de minimis threshold)

The calculation above that the de minimis threshold is $1,477.50. With the figure, we can determine which form of tax is applied based on the purchase price.

If the purchase price is above $1,477.50, it will be treated as capital gains tax. If the purchase price is below $1,477.50, it will be treated as ordinary income tax.

De Minimis Fringe Benefits

De minimis tax rule also applies to fringe benefits offered by employers. Since the de minimis benefits offered are so small, it will be unreasonable to account for them, and they are exempt from taxation. These are some of the main de minimis benefits:

- Snacks and coffee brought into the workplace to increase employee morale

- Holiday gifts offered by the firm for their employees

- Tickets for special work events or certain occasions

- Personal use of office equipment such as the photocopier

- Occasional meal allowance given to outstanding employees

- Transport expenses for employees who choose to work overtime

- Cocktail parties or special events organized to boost employee motivation

De minimis benefits cannot assume a tangible monetary value. In other words, money cannot be given as a gift to increase morale without it being taxed. Due to the frequency and small monetary value of the items listed above, de minimis benefits avoid taxation.

De Minimus Safe Harbor

De minimis safe harbor refers to an annual tax return election that allows taxpayers to deduct various purchases that are usually affected by taxation.

It allows businesses that prepare financial statements to deduct up to $2,500. The figure can reach $5,000 if a company uses an applicable financial statement (AFS). An AFS is any type of financial statement registered by the Securities and Exchange Commission (SEC) or audited by a CPA firm.

Why Expense Rather Than Capitalize?

During the process of creating year-end financial statements, accountants are faced with the decision to allocate cost as an expense or to capitalize it. As mentioned above, the de minimis safe harbor emphasizes allocating costs of assets as an expense. Here’s why:

- Capitalization: When a firm capitalizes a cost, it is directed towards capital expenditures. The cost will be accounted for as an asset on the balance sheet and subject to depreciation expense. In general, capitalization lowers the future net income of a firm.

- Expensing: When a cost is expensed, it is added to the company’s income statement and is subtracted from revenue, reducing profit. It may not seem beneficial, but the expensing of costs reduces the overall income tax burden. In general, expensing lowers total assets and shareholder’s equity of a firm.

Related Readings

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.