Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

M&A transactions bring complex accounting challenges that analysts and professionals need to consider

Mergers and acquisitions (M&A) are often used by companies to achieve growth, expand market share, or gain other competitive advantages. Beyond these strategic motivations, M&A brings complex accounting challenges that companies (and analysts) need to understand and consider. This article delves into the key components of M&A accounting, as well as some of the most common challenges and best practices.

Mergers and acquisitions (M&A) refer to the combination of companies or assets through various types of transactions. While the terms “mergers” and “acquisitions” are often used interchangeably, they really have different meanings. Although there is some nuance around these, in general, we will use the following definitions:

M&A can be driven by many factors, including the desire for synergies, market expansion, diversification, and acquiring unique capabilities. M&A transactions can be extremely complex and involve significant changes to the financial statements of the different parties, making accurate accounting essential.

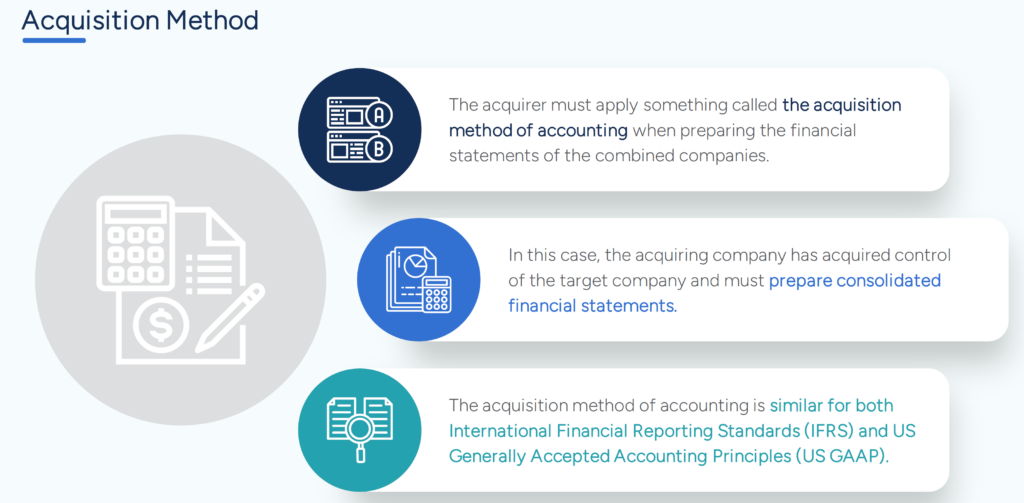

Whether a company prepares its financial statements in accordance with US Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS), business combinations are accounted for using the acquisition method.

The acquisition method requires that after the transaction has been completed, the acquirer will prepare consolidated financial statements, which will include the target company’s financials and results.

Under the acquisition method, accounting rules require that the acquirer performs a purchase price allocation. This means the acquirer will need to measure the target’s identifiable tangible and intangible assets and liabilities at fair value on the acquisition date. Basically, the acquirer will actually restate the target company’s balance sheet at fair value instead of historical cost. This process usually results in write-ups or increases to the target company’s balance sheet.

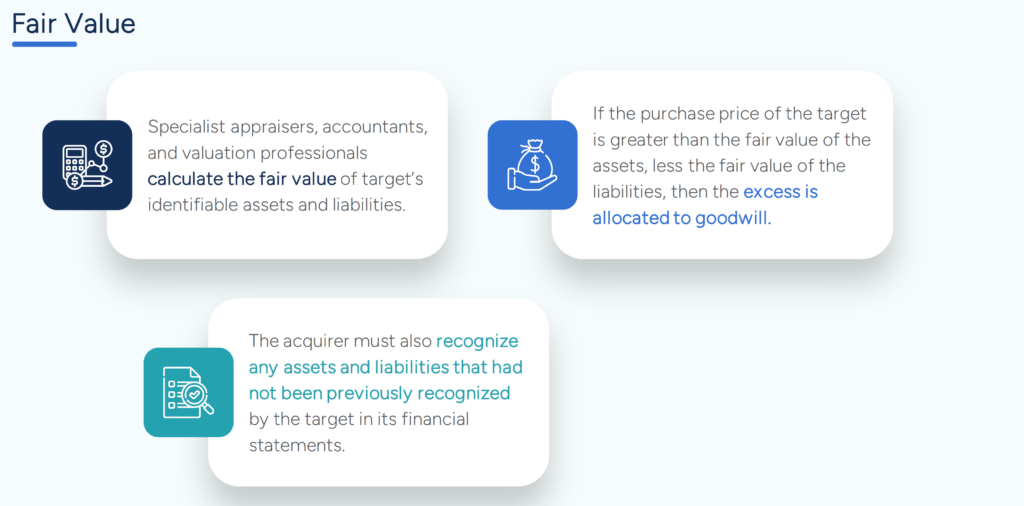

In order to determine the fair value of the target company’s assets and liabilities, the acquiring company will hire specialist appraisers and valuation professionals. These specialists have a deep understanding of accounting principles and valuation methodologies.

For example, if some of the acquired assets are commercial buildings, then a real estate specialist will determine the values. The specialist might look at recent sales of comparable buildings to value the acquired buildings.

After determining the fair value of all of the target’s identifiable assets and liabilities, the fair value of net assets is determined by deducting the liabilities from the assets. If the purchase price of the target is still greater than the fair value of net assets, then the difference between the two is considered goodwill.

Goodwill represents the premium paid over the fair value of the target company’s net assets. Fundamentally, goodwill captures various different unidentifiable assets a company has. These are things like brand value, customer loyalty, management “know-how,” and expected synergies.

Goodwill is only created in an acquisition and cannot be recognized on a balance sheet without an acquisition. In other words, goodwill cannot be created by a company on its own… It’s only a balance sheet asset once the company is acquired.

Additionally, goodwill is considered an indefinite-lived asset, so it is not amortized, but it is tested annually for impairment to ensure it accurately reflects its current value.

However, the purchase price allocation and calculation of the fair value of the target company’s assets and liabilities may have significant tax implications.

Companies maintain two sets of accounting records:

The fair value adjustments impact the accounting records but not the tax records, although this is not always the case, depending on how the transaction is structured.

Because the fair value adjustments impact the accounting records and not the tax records, there is a mismatch between the values on the accounting balance sheet and the tax balance sheet. This mismatch can lead to deferred taxes.

The M&A accounting process involves multiple stages:

M&A accounting presents several challenges, including:

Companies should consider the following best practices to help mitigate the challenges and ensure successful acquisition accounting:

M&A accounting is a critical component of the mergers and acquisitions process that requires careful planning, precise execution, and ongoing attention. By understanding the key elements of M&A accounting, the challenges involved, and the best practices to follow, companies can ensure accurate financial reporting, compliance with accounting standards, and the successful integration of the target company.

As M&A activity continues to be a popular strategy for growth and expansion, mastering the complexities of M&A accounting is essential for financial analysts and business leaders alike.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Accounting for M&A. To keep advancing your career and skills, the following CFI resources will be useful:

CFI’s Accounting for Business Combinations & Other Equity Investments course