Get In-Demand Finance Certifications

A kind of accounting risk that arises due to fluctuations in currency exchange rates

Translation exposure is a kind of accounting risk that arises due to fluctuations in currency exchange rates.

The assets, liabilities, equities, and earnings of a subsidiary of a multinational company are usually denominated in the currency of the country it is situated in. If the parent company is situated in a country with a different currency, the values of the holdings of each subsidiary need to be converted into the currency of the home country.

Such conversion can lead to certain inconsistencies in calculating the consolidated earnings of the company if the exchange rate changes in the interim period. It is translation exposure.

For example, an Austrian subsidiary of an American company purchases a building worth €100,000 on September 1, 2019. On this date, the euro-dollar exchange rate is €1 = $1.20, so the value of the building converted into dollars is $120,000.

The company decides to convert all of its foreign holdings into dollars, to present a consolidated balance sheet on March 31, 2020. On that day, the exchange rate changes to €1 = $1.15, so the value of the building falls to $115,000.

Translation exposure can often depict a distorted representation of a company’s international holdings if foreign currencies depreciate considerably compared to the home currency.

Accountants can choose among several options while converting the values of foreign holdings into domestic currency. They can choose to convert at the current exchange rate or at a historical rate prevalent at the time of occurrence of an account.

Whichever rate they choose, however, needs to be used consistently for several years, in accordance with the accounting principle of consistency. The consistency principle requires companies to use the same accounting techniques over time to maintain uniformity in the books of account.

In case a new technique is adopted, it should be mentioned clearly in the footnotes of the financial statements.

Consequently, there are four methods of measuring translation exposure:

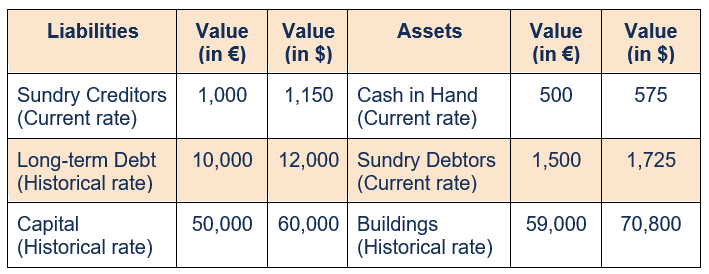

The values of current assets and liabilities are converted at the exchange rate that prevails on the date of the balance sheet. On the other hand, non-current assets and liabilities are converted at a historical rate.

Items on a balance sheet that are written off or converted into cash within a year are called current items, such as short-term loans, bills payable/receivable, and sundry creditors/debtors. Any item that remains on the balance sheet for more than a year is a non-current item, such as machinery, building, long-term loans, and investments.

Consider the following balance sheet of a European subsidiary of an American company, which follows the method. Assume that the historical exchange rate is €1 = $1.20, and the current rate is €1 = $1.15.

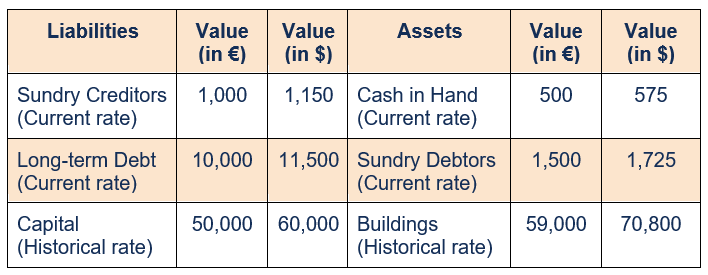

All monetary accounts are converted at the current rate of exchange, whereas non-monetary accounts are converted at a historical rate.

Monetary accounts are those items that represent a fixed amount of money, either to be received or paid, such as cash, debtors, creditors, and loans. Machinery, buildings, and capital are examples of non-monetary items because their market values can be different from the values mentioned on the balance sheet.

The balance sheet prepared using the monetary/non-monetary method will be as follows:

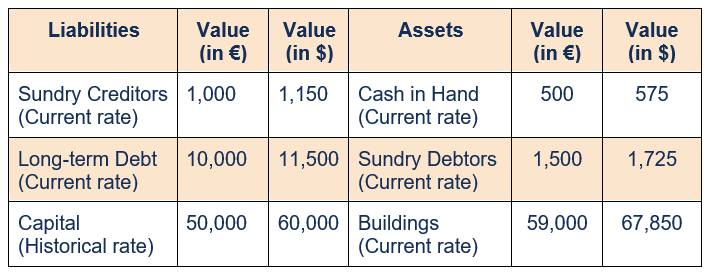

The current rate method is the easiest method, wherein the value of every item in the balance sheet, except capital, is converted using the current rate of exchange. The stock of capital is evaluated at the prevailing rate when the capital was issued.

The balance sheet prepared using the current rate method will be as follows:

The temporal method is similar to the monetary/non-monetary method, except in its treatment of inventory. The value of inventory is generally converted using the historical rate, but if the balance sheet records inventory at market value, it is converted using the current rate of exchange.

In the example above, if there is an inventory of goods recorded in the balance sheet at its historical value of, say €1,000, its value in dollars after conversion will be $(1,000 x 1.2), or $1,200.

However, if the inventory of goods is recorded at the current market value of, say €1,050, then its value will be $(1,050 x 1.15), or $1,207.50.

In each of the methods used above, there is a mismatch between the total values of assets and liabilities after conversion. While calculating income and net profit, variations in exchange rates can distort the amounts to a great extent, which is why accountants often use hedging to do away with this risk.

Thank you for reading CFI’s explanation of Translation Exposure. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: