Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The fixed rate of a swap determined by the parties involved in a transaction

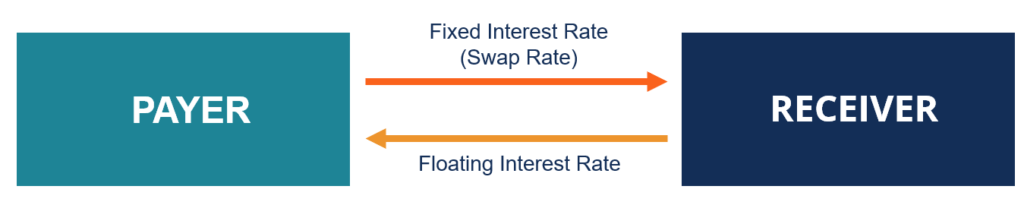

The swap rate is the fixed rate of a swap determined by the parties involved in the contract. The swap rate is demanded by a receiver (i.e., the party that receives the fixed rate) from a payer (i.e., the party that pays the fixed rate) to be compensated for the uncertainty regarding fluctuations in the floating rate utilized in a swap.

The swap rate can be found in either interest rate swaps or currency swaps. It is typically based on a risk-free reference rate for interest rate swaps.

The most common type of interest rate swap involves exchanging a fixed interest rate for a floating interest rate.

The floating rate is typically tied to a widely used benchmark index, such as the Secured Overnight Financing Rate (SOFR) in the United States, the Sterling Overnight Index Average (SONIA) in the United Kingdom, or other risk-free rates adopted in global markets, plus or minus a spread. In this arrangement, the fixed interest rate is referred to as the swap rate (or reference rate).

In interest rate swaps, the swap/reference rate is used to determine the total value of the swap’s fixed leg, which must be equal to the total value of the floating leg of the swap. After the swap becomes effective, the fixed rate remains the same until the swap’s maturity, while the floating interest rate is reset periodically at predetermined dates, based on the fluctuations of the index to which the rate is attached.

Similar to interest rate swaps, currency swaps are a popular type of swap. Currency swaps may come in several forms. One of them is the fixed vs. floating rate currency swaps. In currency swaps, the swap/reference rate is referred to as the exchange rate associated with the fixed leg of a currency swap.

In currency swaps, the swap rate is primarily used as the exchange rate to convert the principal notional amounts set in different currencies. The principal notional amounts are specified prior to the start of the swap’s agreement. Like interest rate swaps, in currency swaps, the reference rate remains unchanged until the swap’s maturity.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: