Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Learn about the different growth theories

The Classical Growth Theory postulates that a country’s economic growth will decrease with an increasing population and limited resources. Such a postulation is an implication of the belief of classical growth theory economists who think that a temporary increase in real GDP per person inevitably leads to a population explosion, which would limit a nation’s resources, consequently lowering real GDP. As a result, the country’s economic growth will start to slow.

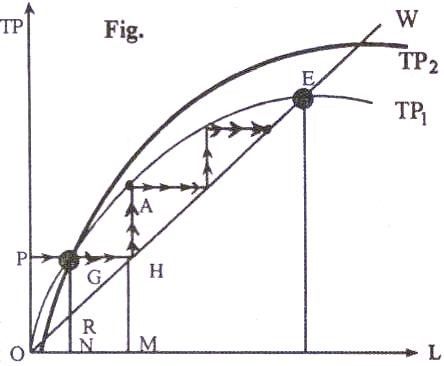

In the chart above, the y-axis represents total production, and the x-axis represents labor. Curve OW outlines the total subsistence wages. If the level of population (labor) is ON, and the level of output is OP, the per capita wage is represented by NR. Consequently, the surplus or profit is RG.

Because of the surplus, the capital formation process comes into effect. Consequently, the demand for labor increases, leading to a rise in total wages, as the curve moves to GH. If the total population remains constant at ON, and wages exceed subsistence wages, i.e., NG > NR, then total population or total manpower will increase as the curve moves toward OM. Because of the increase in population, surplus can be generated.

In such a manner, the process will continue until the economy reaches point E, as depicted by the arrow. Point E represents a stationary situation wherein wages and total output equalize, and no surplus can be generated. However, according to classical economists, with technological progress the production function will shift upward, as depicted by the curve TP2. Also, according to the Classical Growth Theory, economic stagnation can be postponed, although ultimately not avoided.

The Neoclassical Growth Theory is an economic model of growth that outlines how a steady economic growth rate results when three economic forces come into play: labor, capital, and technology. The simplest and most popular version of the Neoclassical Growth Model is the Solow-Swan Growth Model.

The theory postulates that short-term economic equilibrium is a result of varying amounts of labor and capital that play a vital role in the production process. The theory argues that technological change significantly influences the overall functioning of an economy. Neoclassical growth theory outlines the three factors necessary for a growing economy. However, the theory puts emphasis on its claim that temporary, or short-term equilibrium, is different from long-term equilibrium and does not require any of the three factors.

The Neoclassical Growth Model claims that capital accumulation in an economy, and how people make use of it, is important for determining economic growth.

It further claims that the relationship between capital and labor in an economy determines its total output. Finally, the theory states that technology augments labor productivity, increasing the total output through increased efficiency of labor. Therefore, the production function of the neoclassical growth model is used to measure the economic growth and equilibrium of an economy. The general production function in the neoclassical growth model takes the following form:

Where:

Also, because of the dynamic relationship between labor and technology, an economy’s production function is often re-stated as Y = F (K, AL). This states that technology is labor augmenting and that workers’ productivity depends on the level of technology.

The Endogenous Growth Theory states that economic growth is generated internally in the economy, i.e., through endogenous forces, and not through exogenous ones. The theory contrasts with the neoclassical growth model, which claims that external factors such as technological progress, etc. are the main sources of economic growth.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to the Theories of Growth. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: