Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Learn more about the three accounting terms

Income, revenue, and earnings are probably the three most widely used concepts in accounting and finance. All the terms denote measures of a company’s profitability. Although they are defined differently, they are frequently confused with one another.

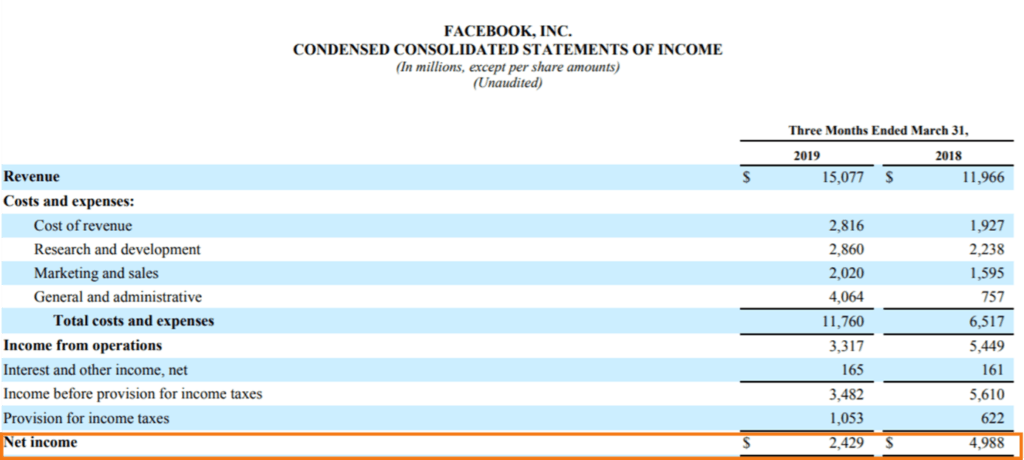

Income (net income) is the amount of money a company retains after subtracting all expenses associated with operations. Therefore, net income is known as the bottom line of a company’s income statement. Earnings and net income are commonly used as synonyms.

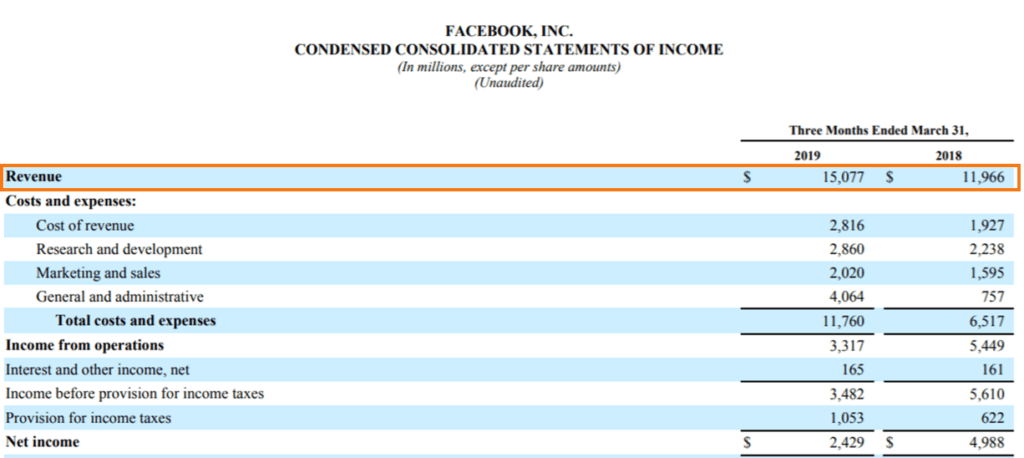

Revenue is the total amount of money a company generates from its core operations. It is the first line on a company’s income statement.

The basic meaning of income is the amount of money an individual or an organization receives for selling goods, providing services, or investing capital. For example, as an employee in a company, income is the wage the individual earns for work rendered. Additionally, they may earn a side income from an investment portfolio of financial assets (e.g., stocks, bonds, etc.). Any type of income is generally taxable. Note that the tax regulations regarding income types may vary among tax jurisdictions.

In the context of business operations, income is the amount of money a company retains internally after paying all expenses and taxes. In this sense, income is commonly referred to as net income. Similar to revenue, net income appears on the company’s income statement. Note that it is reported at the bottom of the statement. Due to this reason, net income can be frequently referred to as the bottom line.

Net income is also used as a profitability measure of a company. The main advantage of net income over other profitability measures is that it indicates what amount of money a company can actually retain internally after accounting for all operating and non-operating revenues and expenses. At the same, investors and analysts view net income as a somewhat deceiving profitability measure that provides a distorted picture of the company’s operating efficiency.

Revenue is the total amount of money a company generates in the course of its normal business operations. Most businesses earn their revenue by selling goods and/or services to the clients. For example, a local coffee shop’s revenue is the total amount of money earned from the sale of coffee and snacks to the customers.

A company’s revenue is reported on an income statement. The first line on every income statement is revenue. As a result, revenue can sometimes be referred to as the top line.

Revenue is the most basic yet important indicator of a company’s profitability and its overall financial performance. It is a critical measure of financial performance that reveals how well a company can generate money from its primary business operations. Generally, analysts and investors carefully assess the company’s revenues from different periods to identify their growth trends.

In some cases, the reliability of revenue can be questionable as the metric is prone to potential manipulation. For example, the management of a company can artificially inflate revenues by applying aggressive revenue recognition principles.

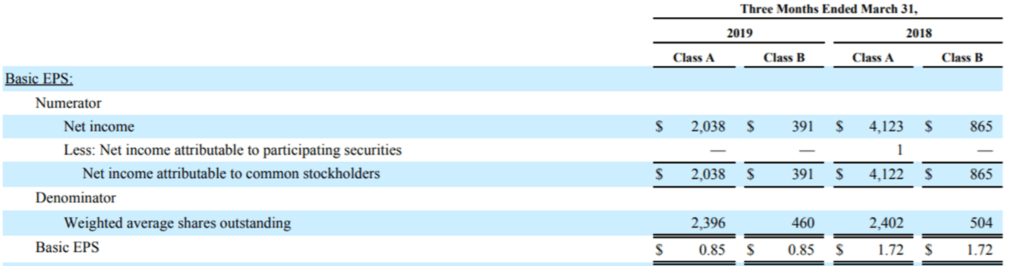

Earnings are the company’s profits. In other words, earnings represent the net income of a company.

Also, earnings can be referred to as the pre-tax income of a company. In such a context, there are many variations of earnings measures such as earnings before taxes (EBT), earnings before interest and taxes (EBIT), and earnings before interest, taxes, depreciation & amortization (EBTIDA). Also, companies commonly report earnings per share (EPS), which indicates their earnings on a per-share basis.

Earnings are considered one of the most critical determinants of a company’s financial performance. For public companies, equity analysts make their own estimates of the company’s anticipated earnings periodically (quarterly and annually). Public companies are concerned with the difference between the actual earnings and the estimates provided by the analysts.

For example, if the company’s actual earnings are lower than the estimated earnings, it may indicate poor performance of the company. On the other hand, the fact that a company beats its earnings estimates is an indicator of its solid performance.

Although manipulation of the company’s earnings is both unethical and illegal, some companies still leverage the flaws in current accounting reporting standards to hide some deficiencies in the operating performance of a company.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: