Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A form of mortgage refinancing where the initial mortgage is paid off, and a new mortgage is established

A cash-out refinance is a form of mortgage refinancing where the initial mortgage is paid off, and a new mortgage is established. The new mortgage loan is larger than the pre-existing loan amount, so the home equity is converted into a cash payout.

Within real estate investing, refinancing is the process of replacing an existing mortgage with one that extends better, more favorable terms to the borrower. A mortgage is essentially a loan taken out to finance the purchase of a real estate asset, such as a house, office, warehouse, etc.

A mortgage is a very commonly used debt instrument that is secured by the underlying property that is being purchased. Thus, mortgage loans are thought of as being one of the safest loans to provide from the lenders’ perspective.

By refinancing the mortgage, the borrower who is purchasing the property may be able to customize the terms of the mortgage, for example:

Typical types of mortgages are 30-year fixed-rate or 15-year fixed-rate mortgages; however, the term (length of the loan) can vary. Generally, a longer-term mortgage means lower monthly payments, however higher overall interest is paid over the life of the mortgage.

In a fixed-rate mortgage, the borrower agrees to pay the same interest rate for the life of the loan. It makes the monthly payments predictable; however, it limits the benefits of favorable market interest rates in the future.

In a variable-rate mortgage, the borrower agrees to pay an interest rate that fluctuates with the interest rates of the market. The initial interest rate is generally below the market rate to make it appear more favorable; however, there is a risk from the borrower’s perspective that the interest rate will increase in the future.

The most common form of mortgage loan refinancing is known as the rate-and-term refinancing. The rate-and-term type of refinancing allows the borrower to refinance at a lower interest rate or adjust the term of the mortgage loan. It is beneficial from the borrower’s perspective because they can take advantage of an economic environment where interest rates are decreasing. Also, the borrower might have realized that they can afford higher monthly payments and decides to shorten the term of the loan, which leads to lower overall interest paid.

However, with cash-out refinancing, the objective is not to obtain more favorable terms within the mortgage. Instead, the goal is to create a larger mortgage and receive the difference between the two loans in tax-free cash. It is a tax-free payout since the money received does not contribute to an increase in taxable income.

The additional cash-out loan is generally charged a higher interest rate than the initial mortgage loan; however, it saves the borrower the troubles of renegotiating a separate personal loan, which may be at an even higher interest rate.

From the lender’s perspective, the risk of the borrower substantially increases if they provide the new loan since the borrower is more likely to default or walk away from the loan afterward.

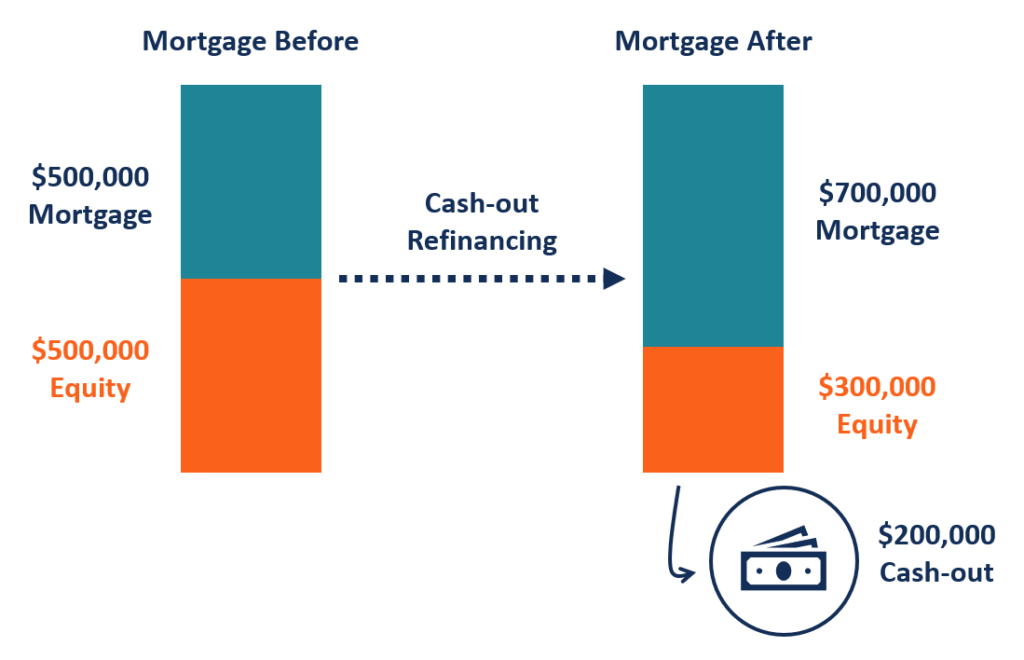

For example, there is a mortgage loan on a $1,000,000 property that is half paid off. Therefore, there is $500,000 of the loan remaining and $500,000 of equity value in the property from the borrower. Now, the borrower wants to convert a portion of the $500,000 equity into cash. Therefore, the borrower opts to initiate a cash-out refinance.

The borrower may wish to convert $200,000 of his equity value into cash, and therefore, can refinance by taking out a new mortgage loan with a total value of $700,000. The excess $200,000 over the original mortgage value will be paid out as cash to the borrower.

Here, the borrower has effectively transferred the equity value of the property into cash. However, the new mortgage of $700,000 will likely have a higher associated interest rate than the prior $500,000 loan in order to reflect the increased risk for the lender.

Although a cash-out refinance may sound similar to a home equity line of credit (HELOC), and they have similar goals – namely allowing the borrower to receive cash by utilizing the underlying equity of a real estate asset – there is a key difference between the two.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: