Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The Home Equity Line of Credit (HELOC) calculator can calculate the maximum line of credit available for a homeowner. A HELOC is similar to a mortgage, as both types of loans use a house as collateral. However, there are no fixed principal repayments or pre-set interest rates for a home equity line of credit.

This template includes the calculations for:

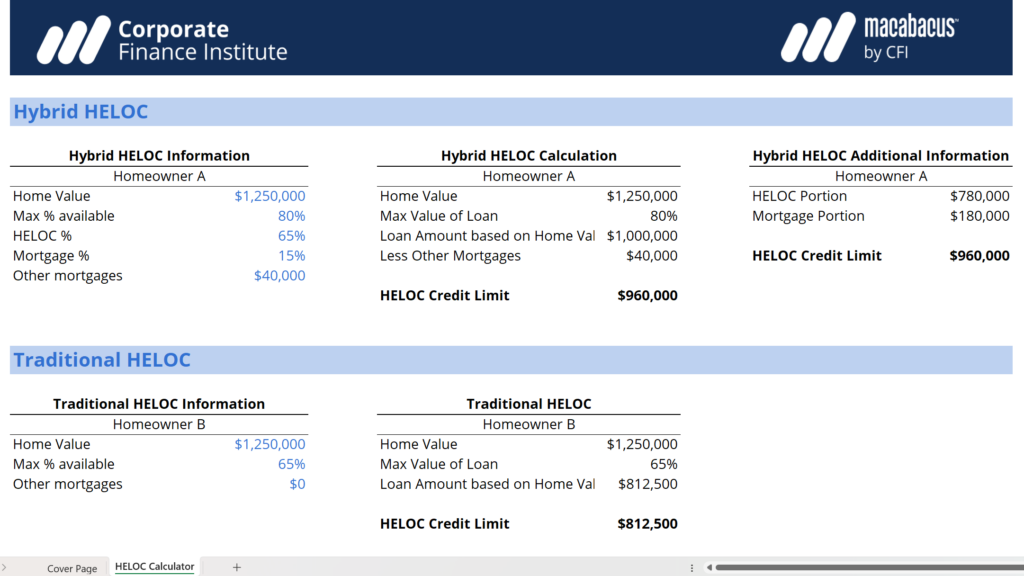

Here is a quick preview of CFI’s HELOC calculator:

Click the button below to download our free Home Equity Line of Credit (HELOC) calculator!

As stated before, a HELOC is a loan that uses a house as collateral. It is similar to a mortgage except for the fact that the entire sum of the mortgage is given upfront. Also, mortgages require principal and interest payments on a monthly basis.

On the other hand, HELOC is a line of credit, which means that the borrower can take out any amount at any time. It is similar to a credit card in which the user only uses it when needed. Also, for a HELOC, only interest payments are required. The principal payment is only necessary when the HELOC expires.

For a traditional HELOC, borrowers can only borrow up to 65% of a house’s value. The borrower also needs to own at least 20% of the house. To determine the maximum amount of line of credit available, multiply the house’s appraised value by 65%. Like the hybrid HELOC, it is also necessary to subtract the outstanding mortgage already on the house.

A hybrid HELOC is a combination of a traditional HELOC and a mortgage. For a hybrid HELOC loan, the borrower is eligible for a line of credit worth up to 80% of the home’s appraised value. To calculate the maximum amount of the line of credit, multiply the value of the house by 80%. After determining the maximum amount available, subtract the amount of an outstanding mortgage, if any. It ensures the total amount of loan using the house as collateral does not exceed 80%. In a hybrid loan, the mortgage portion amortizes while the other portion is the same as a traditional HELOC.

For more resources, check out CFI’s business templates library to download numerous free Excel modeling, PowerPoint presentation, and Word document templates. See also our financial modeling resources and Excel resources.