Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A table that provides details of the periodic payments for a reducing loan

An amortization schedule is a table that provides both loan and payment details for a reducing term loan.

Details typically include the original loan amount, the loan balance at each payment, the interest rate, the amortization period, the total payment amount, and the proportion of each payment that is made up of interest vs. principal. Amortization schedules can be easily generated using several basic Microsoft Excel functions.

In general, amortization schedules are provided to borrowers by banks or other financial institutions when credit is extended so that borrowers understand the repayment structure.

A good deal of both consumer credit (like car loans and home mortgages) and business credit (like CAPEX loans for PP&E and commercial mortgages) is repaid by periodic payments, sometimes called installments. These are often monthly, but not always.

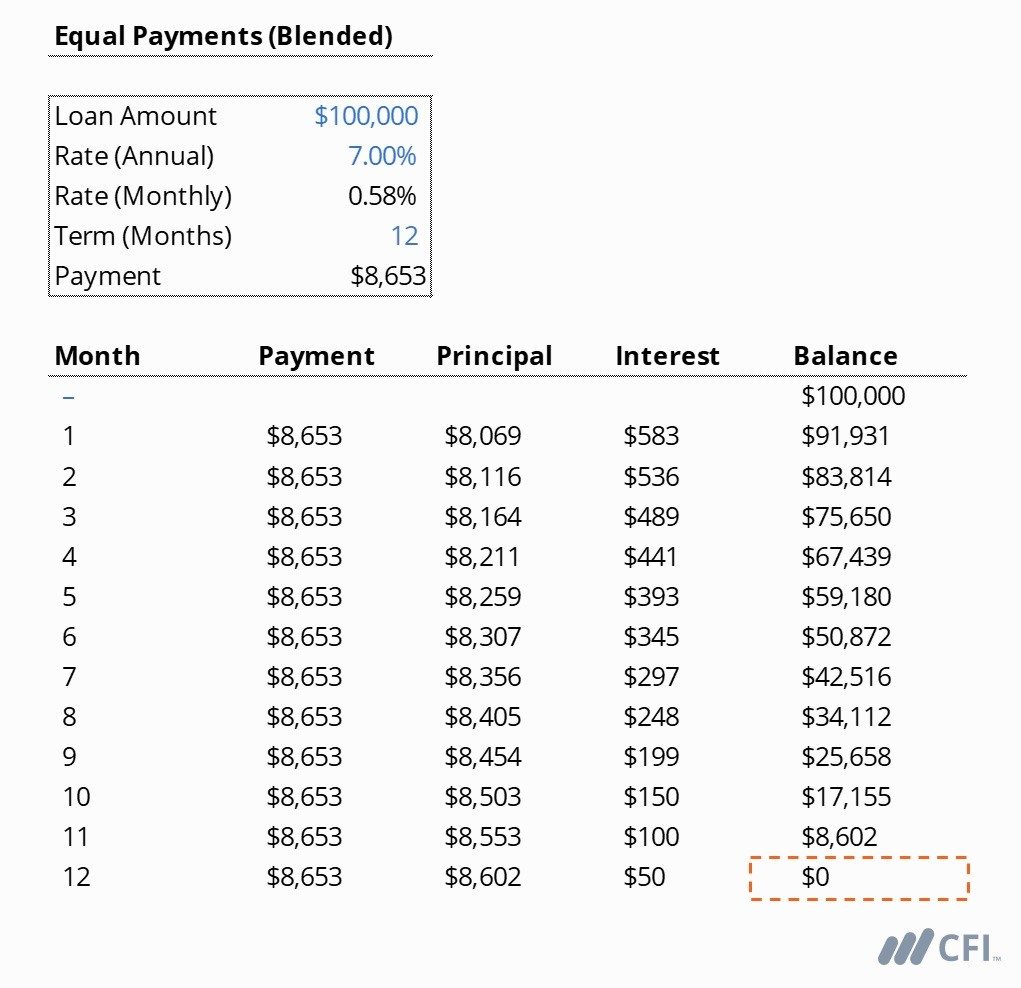

When a loan is repaid in installments, it’s typically referred to as an amortizing loan (or a reducing loan). Below is an example of a $100,000 loan on a 12-month (1-year) amortization.

The point of a reducing loan is that the outstanding balance is paid down to zero at the end of the amortization period:

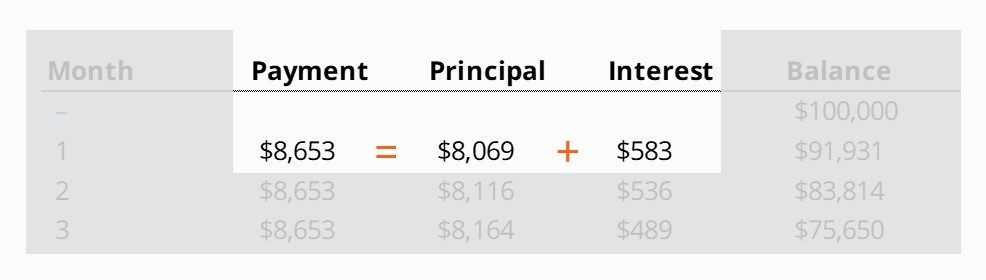

Every loan payment has two components, interest and principal.

With a reducing loan, some portion of the original loan amount is repaid at each installment. Only this principal portion of the loan payment reduces the total loan amount outstanding; the interest portion does not.

The proportion of interest vs. principal depends largely on the interest rate and on whether the loan is structured as an equal amortizing loan or as an equal payment loan (often called blended payments).

Amortization schedules should clearly show if a loan is equal payment or equal amortizing.

This is often referred to as a blended payment structure. The borrower knows exactly how much their loan payment is, and the payment amount will be equal each period. A common example is a residential mortgage, which is often structured this way.

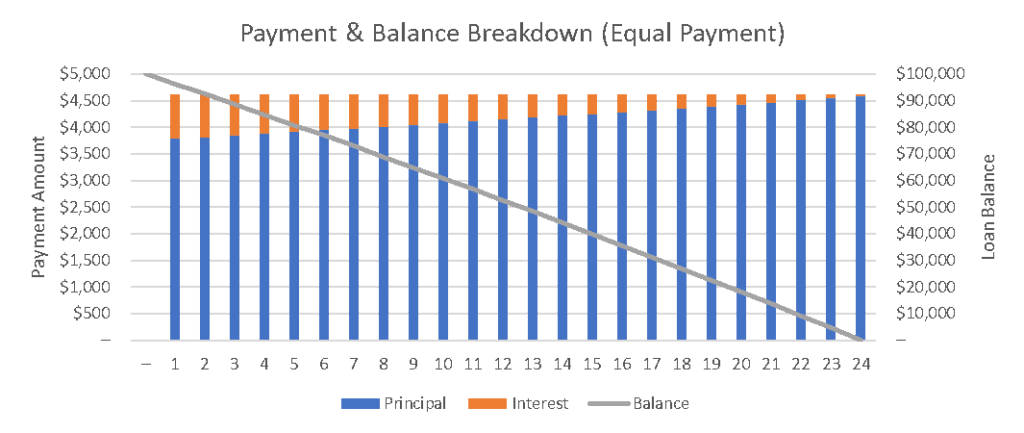

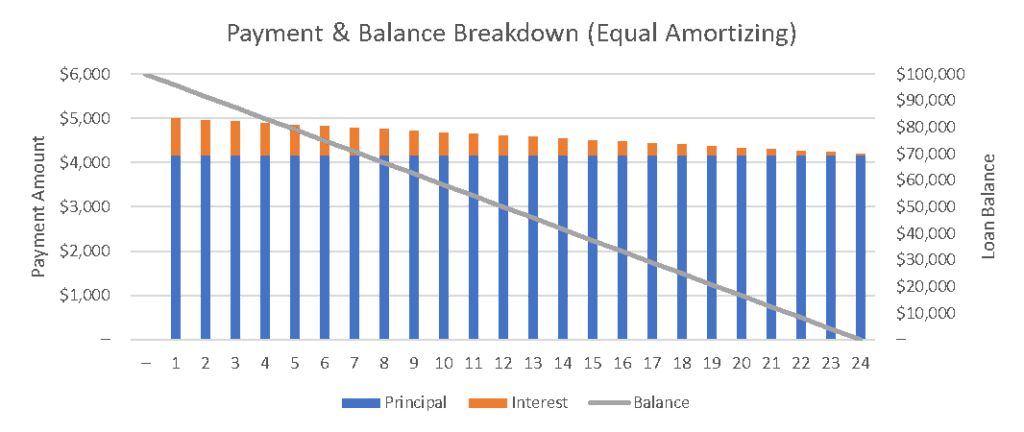

Here’s an easy way to visualize loan payments on a 2-year (24-month) amortization schedule:

Since interest is calculated on the principal amount outstanding at the end of the previous period, the proportion of interest embedded in the loan payment (orange) is higher earlier on, then lower later.

The secondary vertical axis shows the total loan balance, represented graphically by the gray line. You’ll notice that the outstanding loan balance decreases with each installment of principal (blue bars).

This is often referred to as a P&I structure (principal + interest). In an equal amortizing structure, the loan amount is divided by the total number of payments; this becomes the principal payment amount each period, with interest being charged over and above the principal amount.

Here is the same loan as before ($100,000 over 24 months) but using an equal amortizing structure instead of an equal payment structure:

Here, the blue “principal” bar remains constant throughout the loan amortization period, while the orange interest is added incrementally.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their banking careers to the next level. To keep learning and advancing your career, the following resources will be helpful: