Microeconomics

The study of how individuals and companies make choices regarding the allocation and utilization of resources

What is Microeconomics?

Microeconomics is the study of how individuals and companies make choices regarding the allocation and utilization of resources. It also studies how individuals and businesses coordinate and cooperate, and the subsequent effect on the price, demand, and supply. Microeconomics refers to the goods and services market and addresses economic and consumer concerns.

Why are seniors receiving discounts on public transportation systems? Why do flight tickets cost so much during the holiday season? Such questions are considered to be microeconomic, as they are focused on markets or individuals in an economy. Microeconomics also analyzes market failures where productive results are not achieved.

Summary

- Microeconomics deals with the study of how individuals and businesses determine how to distribute resources and how they interact.

- The supply and demand theory in microeconomics assumes that the market is perfect.

- Microeconomics uses various principles, such as the Law of Supply and Demand and the Theory of Consumer Demand, to predict the behavior of individuals and companies in situations involving financial or economic transactions.

Assumptions in Microeconomic Theory

- Microeconomic theory begins with a single objective analysis and individual utility maximization. To economists, rationality means an individual’s preferences are stable, total, and transitive.

- It assumes continuous preference relations to ensure that the utility function is differentiable when you compare two different economic outcomes.

- The microeconomic model of supply and demand assumes that the markets are perfect. It means that there are a large number of buyers and sellers in the market, and none of them can influence the price of products and services significantly. Nonetheless, in real-life cases, the principle fails when any buyer or seller controls prices.

Theories in Microeconomics

1. Theory of Consumer Demand

The theory of consumer demand relates goods and services consumption preference to consumption expenditure. Such a correlation provides a way for consumers, subject to budget constraints, to achieve a balance between expenses and preferences by optimizing utility.

2. Theory of Production Input Value

According to the production input value theory, the price of any item or product is determined by the number of resources spent to create it. Cost may include several of the production factors (including land, capital, or labor) and taxation. Technology may be regarded as either circulating capital (e.g., intermediate goods) or fixed capital (e.g., an industrial plant).

3. Production Theory

The production theory in microeconomics explains how businesses decide on the quantity of raw material to be used and the quantity of items to be produced and sold. It defines a relationship between the quantity of the commodities and production factors on the one hand, and the price of the commodities and production factors on the other.

4. Theory of Opportunity Cost

According to the opportunity cost theory, the value of the next best alternative available is the opportunity cost. It depends entirely on the valuation of the next best option and not on the number of options.

The Demand and Supply Model of Microeconomics

The demand and supply model of microeconomics explains the relationship between the quantity of a good or service that the producers are willing to produce and sell at different prices and the quantity that consumers are willing to buy at such prices. In a market economy, price and quantity are considered basic measures to gauge the goods produced and exchanged.

Basic definitions

Demand: In microeconomics, demand is referred to as the quantity of product or service that the consumers are willing to purchase at a particular price level. The quantity demanded by the consumers also depends on their ability to pay.

Supply: In microeconomics, supply refers to the amount of product or service that the producers are willing to provide at a particular price level. Moreover, companies seek to maximize their profit; hence, they would manufacture and supply a larger quantity of products if they can be sold at higher prices.

Law of Demand and Supply

In microeconomics, the law of demand states that the quantity of commodities demanded by consumers varies inversely with prices of the commodities, all other factors being constant. This implies that if the price of any commodity increases, the demand for that commodity will decrease.

The law of supply states that an increase in the price of any commodity will lead to an increase in supply and vice versa, all other factors being constant. The producers attempt to maximize their profit by increasing the quantity when the price rises.

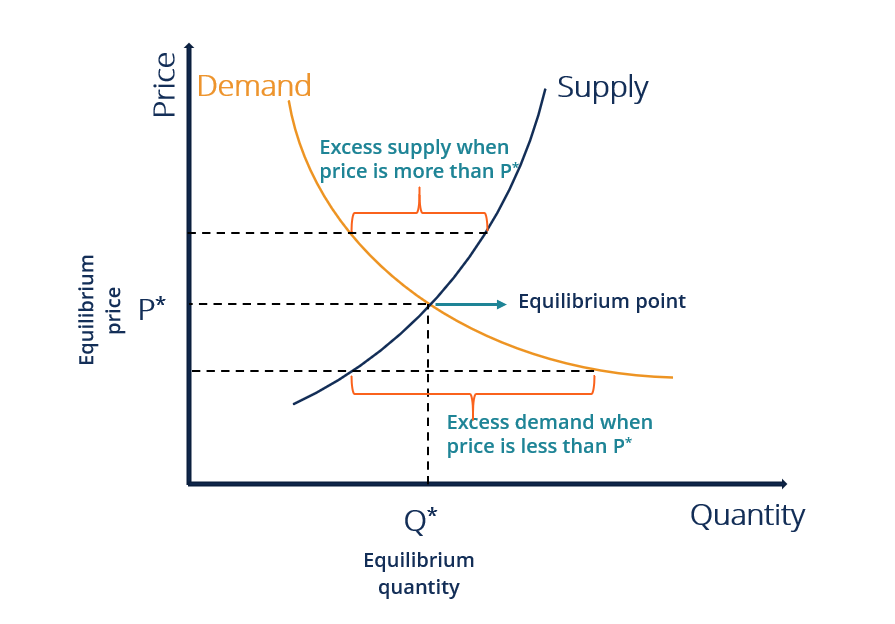

The point of intersection of the demand curve and supply curve is called the equilibrium point. At the equilibrium point, the price and quantity are respectively known as the equilibrium price (P*) and equilibrium quantity (Q*). Due to a change in any of the economic or consumer factors, the market shifts away from the equilibrium point. However, the economy behaves accordingly to bring the market back to the equilibrium point.

Now, assume that the price of a certain commodity falls below P*. In such a case, the demand for that commodity will surge. The quantity supplied will not be enough to cater to the quantity demanded, resulting in excess demand or shortage. The producers will realize that they have an opportunity to sell whatever quantity they have at a higher price and make profits.

Consequently, the price will rise toward the equilibrium. Similarly, if the price of a commodity increases above P*, there will be a drop in quantity demanded. At the new price, the quantity supplied is more than the quantity demanded, which results in excess supply or surplus. The producers will eventually start selling at lower prices, causing an increase in demand, and the market will move towards the equilibrium point.

Structure of the Market

Market structure is determined by various aspects, such as the number of buyers and sellers in the market, the distribution of market shares between them, and how convenient it is for the companies to enter and leave the market.

1. Pure competition

Pure competition is a market structure in which numerous small firms compete against each other. The demand and supply determine the quantity of the commodities produced and the market prices. The firms cannot influence the prices, and the commodities produced by all the firms are identical.

2. Monopoly

In such a monopolistic market structure, there is a single company controlling the supply in the entire market. As there are no substitutes, the company reduces the quantity supplied, increases the price, and earns considerable profits.

3. Oligopoly

In an oligopoly, a few companies control the entire market. The companies can either compete or collaborate to raise prices and earn more profits.

4. Monopsony

A monopsony exists when only one buyer is controlling the demand for commodities, whereas there are many sellers in the market.

5. Oligopsony

An oligopsony exists when there are only a small number of buyers but many sellers. In such a market, the buyers exert more power than sellers, unlike oligopoly, where sellers control the market.

More Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: