Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The cost of choice

Opportunity cost is one of the key concepts in the study of economics and is prevalent throughout various decision-making processes. The opportunity cost is the value of the next best alternative foregone. In simplified terms, it is the cost of what else one could have chosen to do.

Principles of management accounting or corporate finance dictate that opportunity costs arise in the presence of a choice. If there appears to be only one option presented in the decision-making process, the default alternative is “laissez-faire” (to do nothing) with an associated cost of zero. However, if a decision-maker must choose between Decision A or B, the opportunity cost of Decision A is the net benefit of Decision B and vice versa.

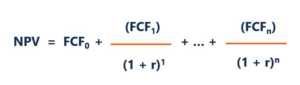

In financial analysis, the opportunity cost is factored into the present when calculating the Net Present Value formula.

Where:

NPV: Net Present Value

FCF: Free cash flow

r: Discount rate

n: Number of periods

When presented with mutually exclusive options, the decision-making rule is to choose the project with the highest NPV. However, if the alternative project gives a single and immediate benefit, the opportunity costs can be added to the total costs incurred in C0. As a result, the decision rule then changes from choosing the project with the highest NPV to undertaking the project if NPV is greater than zero.

Financial analysts use financial modeling to evaluate the opportunity cost of alternative investments. By building a DCF model in Excel, the analyst is able to compare different projects and assess which is most attractive.

For example, assume a firm discovered oil in one of its lands. A land surveyor determines that the land can be sold at a price of $40 billion. A consultant determines that extracting the oil will generate an operating revenue of $80 billion in present value terms if the firm is willing to invest $30 billion today.

The accounting profit would be to invest the $30 billion to receive $80 billion, hence leading to an accounting profit of $50 billion. However, the economic profit for choosing to extract will be $10 billion because the opportunity cost of not selling the land will be $40 billion.

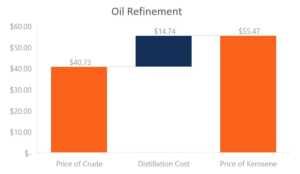

A firm may choose to sell a product in its current state or process it further in hopes of generating additional revenue. For example, crude oil can be sold at $40.73 per barrel. Kerosene, a product of refining crude, would sell for $55.47 per kilolitre. While the price of kerosene is more attractive than crude, the firm must determine its profitability by considering the incremental costs required to refine crude oil into kerosene.

In this example, the firm will be indifferent to selling its product in either raw or processed form. However, if the distillation cost is less than $14.74 per barrel, the firm will profit from selling the processed product. If not, it would be better to sell the product in its raw form.

A sunk cost is a cost that has occurred and cannot be changed by present or future decisions. As such, it is important that this cost is ignored in the decision-making process.

For instance, assume that the firm described above has invested $30 billion to start its operations. However, a fall in demand for oil products has led to a foreseeable revenue of $50 billion. As such, the profit from this project will lead to a net value of $20 billion. Alternatively, the firm can still sell the land for $40 billion.

The decision in this situation would be to continue production as the $50 billion in expected revenue is still greater than the $40 billion received from selling the land. The $30 billion initial investment has already been made and will not be altered in either choice.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: