Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

Companies that provide insurance to insurance companies

Reinsurance companies, also known as reinsurers, are companies that provide insurance to insurance companies. In other words, reinsurance companies are companies that receive insurance liabilities from insurance companies.

It is important to realize that, similar to any other businesses, insurance companies require protection against risk. Insurance companies manage their risk through a reinsurance company.

Recall that reinsurance companies provide insurance to insurance companies. How exactly does it work?

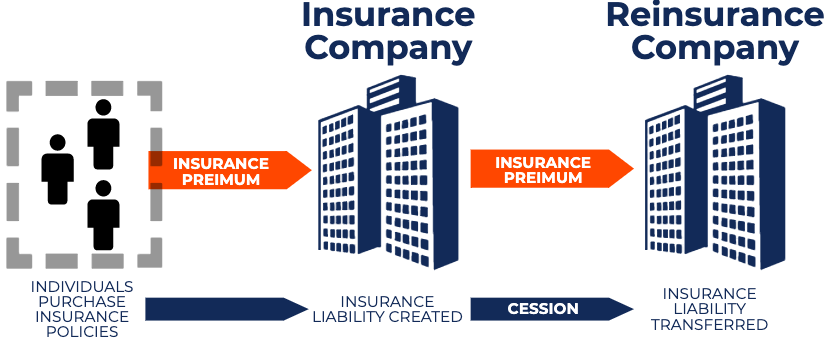

A primary insurer (the insurance company) transfers policies (insurance liabilities) to a reinsurer (the reinsurance company) through a process called cession. Cession simply refers to the portion of the insurance liabilities transferred to a reinsurer.

Similar to the way individuals pay insurance premiums to insurance companies, insurance companies pay insurance premiums to reinsurers for the transfer of insurance liabilities. The diagram below depicts such a relationship.

Reinsurance companies are used by insurance companies to:

Insurance companies can issue policies with higher limits due to some of the risk being offset to the reinsurer.

The income of insurance companies can be more predictable by transferring highly risky insurance liabilities to reinsurers to absorb potentially large losses.

By offsetting the risk of loss in insurance liabilities, insurance companies do not need to keep as much capital on hand to cover potential losses. Thus, they can invest the capital elsewhere to increase their revenues.

Reinsurance enables insurance companies to underwrite more policies, due to a portion of their liabilities being transferred to reinsurers. This enables insurance companies to take on more risk.

Natural disasters such as earthquakes and hurricanes can cause claims to be abnormally high. In such cases, an insurance company can potentially go bankrupt by having to issue out payments to all the claimants. By shifting part of the insurance liabilities to reinsurers, insurance companies are able to remain afloat in such extreme events.

Insurance companies can potentially purchase reinsurance coverage from reinsurers at a rate lower than what they charge their clients. Reinsurers use their own models to evaluate the riskiness of policies. Therefore, reinsurers may accept a lower insurance premium from the insurance company if they deem it as less risky.

Reinsurance companies generate revenue by reinsuring policies that they believe are less risky than expected.

For example, an insurance company may require a yearly insurance premium payment of $1,000 to insure an individual. A reinsurance company may believe that insuring that individual is not as risky as determined by the original insurance company and, therefore, offer to take that insurance liability from the insurance company at a yearly insurance premium payment of $800. The insurance company would be willing to transfer that insurance liability, as they would net $200 yearly from receiving $1,000 to insure the individual and transferring the policy to the reinsurer for only $800. The reinsurer would accept this, as they believe the risk profile of the policy is not as high as determined by the original insurance company.

Additionally, reinsurance companies generate revenue by investing the insurance premiums that they receive. The reinsurer will only need to liquidate its securities if they need to pay out losses. A company that’s been adopting this practice to perfection is Berkshire Hathaway Reinsurance Group.

Lastly, reinsurers generate revenues from insurance companies offloading some of their insurance liabilities related to natural disasters to lower the potential amount of claimant payouts during such unforeseen events.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: