Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

An informal method of transferring money without any money physically moving from one place to another

Hawala, originating from an Arabic term for transfer or trust, is an informal method of transferring money without any money physically moving from one place to another. It is based on a system of money lenders known as hawaladars, which is generally used in the Middle East, Africa, and on the Indian subcontinent outside traditional banking systems common among the Western world.

The hawala system was first developed in India during the 8th century, remaining in use ever since, primarily in Islamic countries. Hawala provided its users with an alternative system of conducting fund transfers across geographical borders instead of the traditional method of using bank wire transfers.

The system became quite sophisticated over the last few centuries, was used for trade along the Silk Road, and later developed into a fully-fledged money market instrument in South Asia. Indeed, it only got replaced by the more traditional and formal banking systems common in Western nations in the middle of the 20th century.

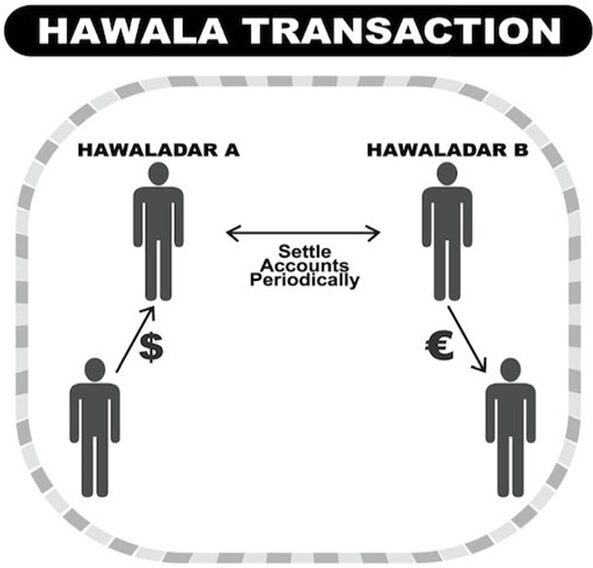

Central to understanding the hawala system is to get a sense of the importance of the hawaladars, or hawala dealers who play an integral role, as well how the system is built on the heavy reliance on trust, family relationships, and connections, and regional affiliations.

For example, Amir lives and works in New York City and wants to send $1,000 to his cousin Iqbal in Pakistan. Amir decides to visit a hawaladar, Mohammad, in New York and provides him with the details of the transaction, which includes the name of his cousin, city of residence, and a password.

Amir also gets in touch with Iqbal to provide him with the password as well. Mohammad then contacts Shirin, a hawaladar in Iqbal’s city, through his list of contacts and asks her to meet up with Iqbal to provide him with Amir’s $1,000.

Shirin and Iqbal meet, and he gets the money after correctly stating the password he received from his cousin Amir. Shirin transfers $1,000 to Iqbal immediately from his own account and now is owed that amount by hawaladar Mohammad back in New York.

The above illustrates the important steps in the hawala system and confirms the importance of hawaladars.

Transactions of similar nature occur all the time, and it is important to note that the transfer of funds between Amir and Iqbal through intermediaries Mohammad and Shirin take place within one or two days, or even a few hours, even when time differences are taken into consideration. It makes the entire process much quicker than if the transfer were to go through the traditional banking system.

As mentioned, the hawala system is unique when compared to formal banking systems because it is built on an honor system and, often, strong family connections.

Another important distinguishing fact is how there is little written record documentation, and promissory notes or notes payable are not exchanged between the hawala dealers. The dealers keep informal records of all the credit and debit transactions on their accounts that can be settled in various forms, such as cash, property, services, or others.

As such, the hawala system operates independently of any legal, judicial system, which means that it does not rely on the legal enforceability of claims or other types of legal action.

It is where the use of connections, often familial ones, and a system of honor and trust come into play since many of the hawala networks are built by members of the same family, clan, village, or other association, and those in the network are expected to abide by the implied contractual system.

Individuals who cheat will lose respect and trust among the other members and may be excommunicated.

In addition to the hawala system being much quicker and convenient in terms of transferring payments, its users are also attracted by other advantages such as the ability to transfer money between poorer, less developed countries where formal banking systems are expensive or harder to access by those from a lower socioeconomic status.

It is particularly true for migrant workers who send money and remittances to relatives in their home countries. Furthermore, hawala users are also attracted by the relatively lower commission rates compared to those charged by banks within the traditional banking systems.

Hawala is often considered a form of underground banking and has been frequently used by money launderers and terrorists to transfer funds globally across geographical borders.

One of the main concerns that countries have with this system is how it can be used for money laundering due to the lack of bureaucracy in the system since they are not routed through the banking system and do not face governmental regulation by official bodies.

It provides anonymity in its transactions, as the source of money being transferred cannot be traced, and there are relatively few written and official records.

To keep learning and developing your knowledge base, please explore the additional relevant resources below: