Get In-Demand Finance Certifications

The part of a company’s income that is not attributable to its core business operations

Non-operating income refers to the part of a company’s income that is not attributable to its core business operations. It is a category in a multi-step income statement. Investment income, gains or losses from foreign exchange, as well as sales of assets, writedown of assets, interest income are all examples of non-operating income items.

Some of the non-operating income items are recurring, for example, dividend income, and interest income. Others are non-recurring, such as asset writedowns and gains or losses from the sale of an asset.

A company’s income can be classified into two categories: operating and non-operating. Operating income is also known as earnings before interest and taxes (EBIT). It is the income generated through the company’s core business operations. It shows the company’s performance on its recurring day-to-day operations.

Non-operating income includes the gains and losses (expenses) generated by other activities or factors unrelated to its core business operations.

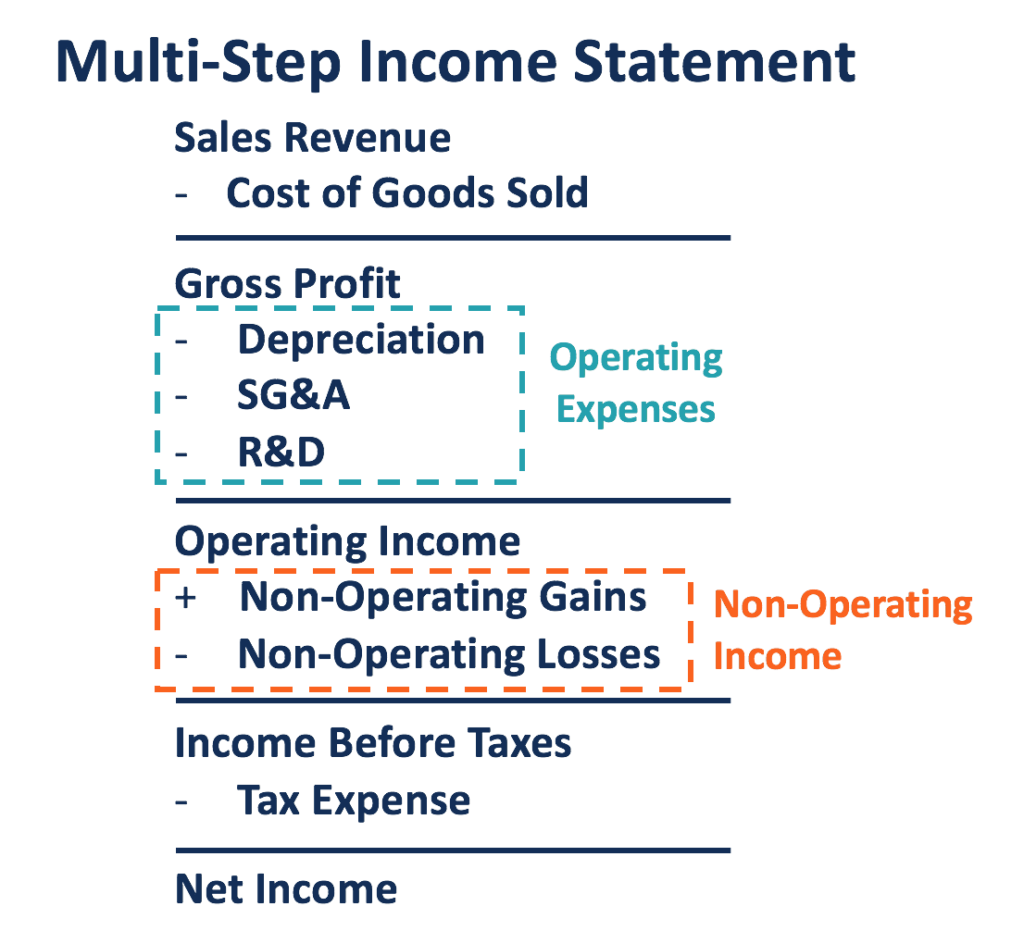

A company’s operating income and non-operating income are identified in a multi-step income statement, as shown below:

Operating income is calculated by subtracting the cost of goods sold and all the operating expenses from the company’s sales revenue. Operating expenses are the expenses incurred to run its core operations. Examples include depreciation, SG&A expenses, as well as R&D expenses.

By adding up the non-operating income to the operating income, the company’s earnings before taxes can be calculated. If the total non-operating gains are greater than the non-operating losses, the company reports a positive non-operating income. If the non-operating losses exceed the total gains, the company realizes a negative non-operating income (loss).

Operating incomes are recurring and are more likely to grow along with the expansion of the company. Compared with non-operating income, operating income provides more information about the fundamentals and growth potential of the company.

A company that performs better in and generates the majority of its income through its core business operations is more favorable than one that makes most of its income from non-operating activities. Distinguishing a company’s ability to profit from its core business and profit from other activities or factors is essential to evaluating its real performance.

A multi-step income statement can better reveal a company’s financial health than a single-step income statement, which does not classify incomes or expenses into the operating and non-operating categories.

Assuming after subtracting the cost of goods sold and all of the operating expenses from the sales revenue, a company reported an operating income of $200,000 for one year. In addition to running its core business, the company also made some investments, which brought in $10,000 in dividends and $8,000 in interest income. During the year, the company paid a $6,000 interest for its previous financing and sold a piece of land at a loss of $4,000. Also, it was sued and was charged for $15,000.

The company’s gains from investment (dividends and interests), interest expense to credit-holders, and losses caused by the sale of land and lawsuit are all non-operating gains or losses. Overall, the company incurred a net non-operating loss of $7,000 for the year after adding up the gains and subtracting losses. Its income before taxes is $13,000. Assuming a 25% tax rate, the company’s net income is $9,750.

Many non-operating gains or losses are non-recurring, which leaves room for accounting manipulation. A company may record a high non-operating income to hide its poor performance on core operations. It may also manipulate its operating income by including gains incurred by activities unrelated to the core business. A sudden, substantial increase in profit could be caused by by the inclusion of non-operating income.

Thank you for reading CFI’s guide to Non-Operating Income. To keep advancing your career, the additional resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: