Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A measure of the return earned by the "capital owners"

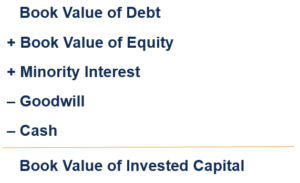

Return on Invested Capital is a profitability or performance measure of the return earned by those who provide capital, namely the firm’s bondholders and stockholders. Return on Invested Capital (ROIC) can be defined as follows:

Where:

There are three key insights to be gained from this definition:

Download the free Excel template now to advance your finance knowledge!

The primary reason for comparing a firm’s return on invested capital to its weighted average cost of capital – WACC – is to see whether the company destroys or creates value. If the ROIC is greater than the WACC, then value is being created as the firm invests in profitable projects. Conversely, if the ROIC is lower than the WACC, then value is being destroyed as the firm earns a return on its projects that is lower than the cost of funding the projects.

In macroeconomic theory, when a firm gains economic profits in a certain industry, there is an incentive created for new entrants to compete for profits until there are no more economic, or growth, profits to be made – only “normal” profits. A firm being able to consistently earn an ROIC greater than its WACC is an indicator of a strong economic moat and of the firm’s ability to sustain its competitive advantage. Following this logic, it would make sense to assume that ROIC converges to WACC in the long run.

Return on assets (ROA), return on equity (ROE), and return on invested capital (ROIC) are three ratios that are commonly used to determine a firm’s ability to generate returns on its capital, but ROIC is considered more informative than either ROA and ROE.

ROA is calculated by taking net income over total assets. However, ROA can be substantially skewed either higher or lower based on a firm’s cash balance.

ROE is calculated as net income over shareholders’ equity and is used to compare firms with the same capital structure. However, ROE can be positively impacted by actions that reduce shareholder equity (e.g., write-downs, share buybacks), but that does nothing to net income. Another limitation of ROE is that a firm may take on excess leverage and still look as if they are handling things well.

ROIC addresses the issues with ROA and ROE in calculating profitability. Cash is netted out when solving for invested capital in the denominator, solving the issue of differences in cash balances across firms. Furthermore, we can compare ROIC across firms with different capital structures, since NOPAT in the numerator is a measure of earnings available to all of the providers of capital.

Return on Invested Capital is a measure of return that can be useful to all professions in finance. Portfolio managers can compare the spread between WACC and ROIC to identify value across investments. Research analysts use ROIC to check their financial model’s forecast assumptions (e.g., no perpetual ROIC growth). Management teams use ROIC to plan capital allocation strategies and benchmark investment opportunities. Investment bankers use ROIC to pitch appropriate financial advisory services and make benchmark valuations.

It is critical for both companies and their investors to be able to measure how well a company is performing with the capital it is provided with. The following CFI resources can help you become more skilled at investment analysis and business valuation.

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: