Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A bond with a maturity or par value of less than $1,000

As the name suggests, baby bonds are fixed-income securities with the size characteristics of babies in the sense that their par values are small. Baby bonds have a par value of less than $1,000 but typically range in values between $25 and $500. A sample baby bond from New Mountain Finance Corporation is depicted below (as of January 4, 2021):

The notes/bonds were issued at $25, and as a result of a change in the yield required, the bond is trading at $25.28. The coupon rate is 5.75%, and since the bond is trading at $25.28, the yield is slightly lower than 5.75% (5.67% as of January 5, 2021).

To learn more about bond pricing, duration, and yield curve analysis, check out CFI’s Fixed Income Fundamentals course!

The usual maturity range for baby bonds is five to 15 years. However, even 50-year bonds are available in the market. The bonds are also frequently issued by state and local governments, such as municipalities and counties. As a result of the taxation power of such entities, the credit and default risks are low. Therefore, municipal baby bonds are usually highly rated (A or above).

A significant amount of baby bonds are issued as zero-coupon bonds. These bonds do not pay any intermediate interest/coupon payments and just pay the par value (generally $25) at maturity.

Since they are issued at a significant discount, the investment amount is reduced even further. For example, a zero-coupon bond similar to the previous example but with no interest payments will cost $21.09 with three years to maturity and provide a 5.75% return.

Baby bonds are advantageous for several reasons. They include:

Despite their significant advantages, baby bonds come with their own set of drawbacks, which may include:

Baby bonds may also refer to the policy proposed by economists William Darity and Darrick Hamilton in 2010, which aimed to reduce racial income inequality in the U.S. They proposed that families in the lowest wealth quartile should receive $50,000 to $60,000 for their newborns. The said amount invested in federally managed funds can be accessed by the newborns when they turn 18. The bonds were slated to significantly reduce wealth inequality. However, the policy remains unimplemented.

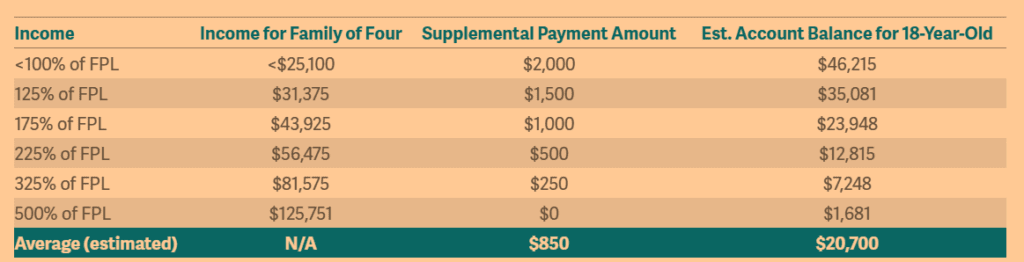

Most recently, Cory Booker, a U.S. senator and a former Democratic presidential candidate, proposed a similar plan to provide each family of four people with an annual supplemental payment amount based on their income level. The supplemental payments would increase as income in relation to the federal poverty line decreases. The proposed payments are depicted below:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Capital Markets & Securities Analyst (CMSA)® certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: