Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

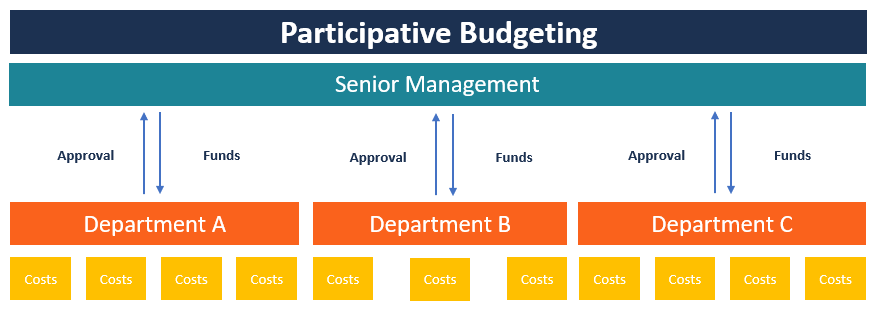

A budgeting process that involves lower-level management

Participative budgeting is a budgeting process in which the people who are in the lower levels of management are involved in the budget preparation process. Unlike the imposed budgeting process, participative budgeting shares the responsibility with lower-level managers to give them a sense of ownership in the business.

Participative budgeting also tends to produce budgets that are more achievable since lower-level employees are better positioned to inform their supervisors where funds need to be allocated. When an organization implements participative budgeting, it shows the top management’s confidence in its staff. The employees’ sense of ownership gives them the motivation to work hard and attain the goals that they helped prepare.

A budget faces a higher chance of being achievable if the people preparing the budget are knowledgeable about the costs that are incurred within the organization. While the top management may possess the necessary information about the running of the company, they may not be privy to the costs incurred at the departmental level. It means that they may underestimate the costs or overestimate the projected revenues. It will eventually affect the running of the department due to cash shortfalls.

However, involving the subordinate managers in coordinating the budget preparation process will benefit the company since these managers have better information about the running of their respective departments.

A participative budgeting process will be more effective when the organization adopts a system of checks and balances to prevent unruly managers from abusing their power. Since the budget moves from the lower managers to the middle and then to the top management, the budget draft can be reviewed at each level of management, with the top managers having the final say.

At each managerial level of review, the managers are interested in identifying any costs that may result in wastage and inefficiencies in the company. Before any changes are made to the budget draft, the lower-level managers must be involved to give their reasons for making certain suggestions in the budget. This will result in the effective use of funds when the managers work hand-in-hand with the accounting staff.

The following are some of the benefits of implementing a participative budgeting approach in an organization:

One of the advantages of participative budgeting is the sharing of information from departmental-level managers to top management. It means that subordinate managers are given the opportunity to present their views on certain organizational issues.

The managers also get a chance to discuss the difficulties that they encounter in budget preparation and brainstorm ways of solving the problems. Both the top managers and the subordinates are also able to share their points of view on certain issues of interest.

When employees are involved in the budget preparation process, they get to own a part of the budgeting process. It gives them a sense of ownership when their suggestions are taken into account by senior management. They also feel appreciated by management when they are given an opportunity to sit down with the top managers and share their views on certain points of interest. Employee involvement in the process improves their morale, providing them with a greater urge to work harder towards the attainment of the goals that they helped set.

Goal congruence refers to the agreement between the employee’s goals and the overall company goals. In order for the company to create a budget that is achievable, both the management and the staff must set goals that move in the same direction.

For example, if the goal of the company is to double the production capacity in the next year, it should be shared with the employees since they are the people tasked with implementing the proposal. If there is no agreement between the company’s goals and the subordinate managers’ goals, it will be impossible to attain the set targets.

The most common limitation of a participative budget is that it is time-consuming compared to an imposed budget. Since the budget preparation starts from the department level to the top, too much participation may occur, which may derail the process.

Involving all employees in each department will mean that the negotiations may take too long before the staff reaches an agreement. If there is no agreement, the management will need to make the final decision, which means that the staff will need to accept an imposed decision.

The other limitation is budgetary slack. The employees may overestimate the costs and/or underestimate the revenue projections as a way of manipulating the budget to their advantage. It means that the subordinate managers will set targets that they are sure to achieve and even exceed in the next financial year.

This mostly happens when the manager’s performance is measured on the basis of the attainment of the budget. By making the budget easy to achieve, the managers will be seen as exceeding their targets.

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.