Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

Four common ways to creating a budget

There are four common types of budgets that companies use: (1) incremental, (2) activity-based, (3) value proposition, and (4) zero-based. These four budgeting methods each have their own advantages and disadvantages, which will be discussed in more detail in this guide.

Source: CFI’s Budgeting & Forecasting Course.

Incremental budgeting takes last year’s actual figures and adds or subtracts a percentage to obtain the current year’s budget. It is the most common type of budget because it is simple and easy to understand. Incremental budgeting is appropriate to use if the primary cost drivers do not change from year to year. However, there are some problems with using the method:

Activity-based budgeting is a top-down type of budget that determines the amount of inputs required to support the targets or outputs set by the company. For example, a company sets an output target of $100 million in revenues. The company will need to first determine the activities that need to be undertaken to meet the sales target, and then find out the costs of carrying out these activities.

Source: CFI’s Budgeting & Forecasting Course.

In value proposition budgeting, the budgeter considers the following questions:

Value proposition budgeting is really a mindset about making sure that everything that is included in the budget delivers value for the business. Value proposition budgeting aims to avoid unnecessary expenditures – although it is not as precisely aimed at that goal as our final budgeting option, zero-based budgeting.

As one of the most commonly used budgeting methods, zero-based budgeting starts with the assumption that all department budgets are zero and must be rebuilt from scratch. Managers must be able to justify every single expense. No expenditures are automatically “okayed”. Zero-based budgeting is very tight, aiming to avoid any and all expenditures that are not considered absolutely essential to the company’s successful (profitable) operation. This kind of bottom-up budgeting can be a highly effective way to “shake things up”.

The zero-based approach is good to use when there is an urgent need for cost containment, for example, in a situation where a company is going through a financial restructuring or a major economic or market downturn that requires it to reduce the budget dramatically.

Zero-based budgeting is best suited for addressing discretionary costs rather than essential operating costs. However, it can be an extremely time-consuming approach, so many companies only use this approach occasionally.

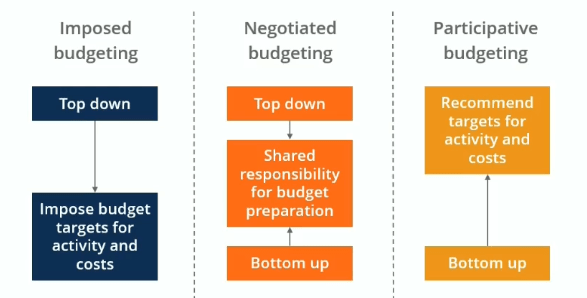

We want buy-in and acceptance from the entire organization in the budgeting process, but we also want a well-defined budget and one that is not manipulated by people. There is always a trade-off between goal congruence and involvement. The three themes outlined below need to be taken into consideration with all types of budgets.

Imposed budgeting is a top-down process where executives adhere to a goal that they set for the company. Managers follow the goals and impose budget targets for activities and costs. It can be effective if a company is in a turnaround situation where they need to meet some difficult goals, but there might be very little goal congruence.

Negotiated budgeting is a combination of both top-down and bottom-up budgeting methods. Executives may outline some of the targets they would like to hit, but at the same time, there is shared responsibility for budget preparation between managers and employees. This increased involvement in the budgeting process by lower-level employees may make it easier to adhere to budget targets, as the employees feel like they have a more personal interest in the success of the budget plan.

Participative budgeting is a roll-up approach where employees work from the bottom up to recommend targets to the executives. The executives may provide some input, but they more or less take the recommendations as given by department managers and other employees (within reason, of course). Operations are treated as autonomous subsidiaries and are given a lot of freedom to set up the budget.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.