Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

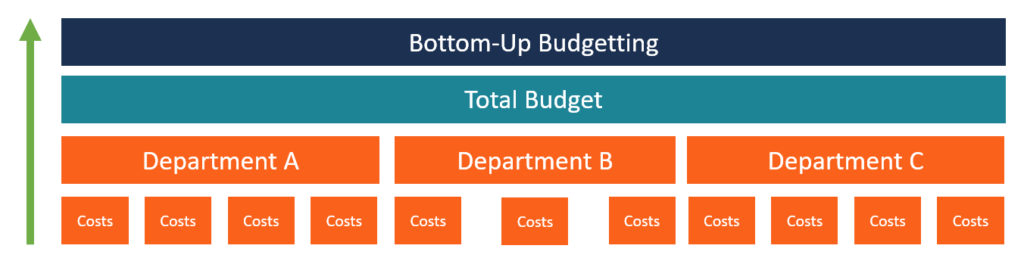

A budgeting method that starts at the department level up to the top level

Bottom-up budgeting is a budgeting method that starts at the department level, moving up to the top level. Each department within the organization is required to compile a list of the things it needs, the projects it plans to carry out in the next financial period, and cost estimates. The estimates of all the departments are then summed up to get the overall company budget. The managers of each department are required to give their input since they know the cost estimates for the projects to be implemented.

The following is the basic process that organizations follow when formulating a bottom-up budget:

The first step when creating a bottom-up budget is to identify the individual components of the business and projects that the organization plans to carry out in the coming financial year. List the components and projects and establish the estimated cost to be incurred.

For example, a department may include costs like wages for employees, furniture and fittings, equipment purchases and hires, administrative costs, conference fees, etc. If the organization uses individual projects to get budget estimates, it must first obtain a list of all projects to be carried out in the coming year and then come up with cost estimates for each project.

After departments finish preparing a list of planned projects and expenditures, the costs should be added up to get the total budget for the department. For example, the cost estimates of the human resource department may include $10,000 for recruiting personnel, $20,000 for employee salaries, and $6,000 for administrative costs, bringing the department’s total budget to $36,000. The departmental managers of other departments should come up with the totals for their respective departments.

After getting the budgets of all the departments or identified projects, the budgets should be summed up to get the overall budget for the organization. The totals should be obtained from the departmental heads or head of projects appointed by the organization’s management.

The final stage of the bottom-up budgeting process is submitting the budget estimates to the management for approval. When reviewing the budget, management is interested in knowing if the budgets are aligned with the goals and objectives that the company wants to achieve in the next financial period.

If satisfied with the budget, the management will approve the budget estimates and send it to the finance department to make allocations to individual departments. However, if the company’s leadership is not satisfied with the budget estimates, they can ask the departmental managers to make necessary changes before the budget is again submitted for approval.

The following are some of the benefits that organizations receive when they use bottom-up budgeting:

Bottom-up budgeting calculates budget estimates from the lowest level, which helps boost the accuracy and accountability of the budget. The process involves all the individuals in each department. The estimates given will be as close as possible to reality since the employees are better placed to understand the costs, resources, expenses, and requirements of their respective departments. When the estimates for all departments are added up to get the overall budget, the senior management should know what to expect in the coming year.

When employees are involved in the budget-making process, they are motivated to work hard to achieve the organization’s goals. The employees in each department of the organization are involved in formulating the budget estimates, giving them a sense of ownership in the budget-making process.

Top-down budgeting and bottom-up budgeting are the two most popular types of budgets in corporate budgeting. Top-down budgeting starts with the senior management creating a budget for the entire organization and allocating budgets to the departments.

The departments are then required to create their own budget estimates that are confined to the amounts allocated by the top management. Although the top-down budgeting process takes less time, some departments may struggle to fit into the amounts allocated by management since management may not be aware of all the associated costs a department may incur.

Bottom-up budgeting gives the departmental heads more power in contributing to the organizational budget. The department-level budget estimates are summed up to get the overall organizational budget that is sent to the senior management for approval.

The bottom-up budgeting process allows employees to own the process since they are familiar with the expenditures at the departmental levels. They will also be motivated to work hard since they feel that their input in the organization is valued by the management. On the downside, the departments may produce budgets that are off-target and not in line with the company’s objectives. The budget may need to be modified to reflect the company objectives and remove unnecessary expenditures.

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.