Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

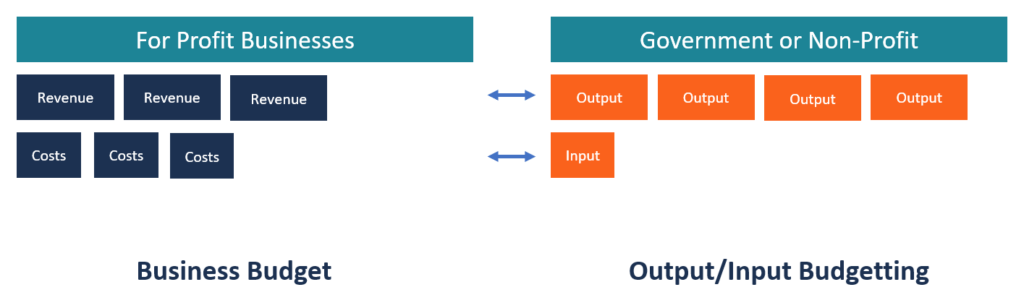

A type of budget that reflects both the funding levels (input) and the expected output from each unit of the organization

An output/input budget is also known as a performance budget. It is a type of budget that reflects both the funding levels (input) and the expected output from each unit of the organization.

The output/input budgeting method is often used by governments to show the relationship between taxpayer funds (input) and the output of services provided by the state and federal governments. It mainly focuses on the expected results rather than the funding levels, which leads to the optimum use of resources in both the public and the private sector.

An output/input budget is prepared based on the management’s evaluation of the performance of the various units in the organization. Units that generate the highest profitability or results are allocated a larger share of the budget, while the trailing units are allocated fewer inputs. This method of allocating resources aims at making optimum use of scarce resources such as expertise, finances, and use of productive time.

For an output/input budget to be efficient, the organization must continually evaluate the performance of the budget and the productivity of the staff in each financial period. This helps management know the results achieved by each unit of the organization and determine how well they are functioning.

Government departments use the results to justify the allocation of different levels of funding to each unit. Since the government relies on taxpayer money to finance its activities, it must ensure that it possesses accurate information on the performance of all departments or projects.

Below are the steps involved in output/input budgeting:

The first step when formulating an output/input budget is to prepare a list of objectives that the organization plans to achieve in the next financial period.

For example, the government’s health department may set the goal of achieving 95% healthcare coverage in the next year. The objectives should be clear. They should be clearly communicated to the employees who are responsible for the successful implementation of the objectives.

After identifying the objectives, the next step is to identify the programs, projects, or units to implement the objectives. The department should secure the required resources, such as finances, infrastructure, and expertise, to accomplish the set goals.

Using the healthcare coverage example above, the government can assign the goal of implementing the 95% healthcare coverage objective to one of the programs under the health department.

The unit should have a positive track record of successfully implementing government directives in the healthcare sector. It should be able to access enough finances, personnel, and other resources required to sign up citizens into the national healthcare program.

The management should develop criteria against which the performance of the program or units will be evaluated. The criteria can be in terms of the number of labor hours, the number of enrollments into a program, or the achievement of certain performance targets.

For example, the success of the 95% healthcare coverage can be evaluated based on the number of citizens enrolled in the program.

The next step is to prepare financial plans for each program or unit. Where several programs or units are involved, the management should allocate funds according to the profitability or resource requirements of each project.

The unit that is expected to produce the biggest results should be allocated a larger share of the budget, compared to other units that produce medium to low results. The allocations should then be summed up to get the overall budget for the organization.

The organization should conduct periodic evaluations of the performance of each unit or program to determine how well they are performing against the budgeted performance.

The management should formulate a systematic approach to evaluation in order to maintain consistency in evaluations from one period to another. The performance is evaluated against the criteria developed by management for each organizational unit or program.

The evaluations show units that are on track to achieving the set targets, as well as units that are lagging behind. The well-performing units should be praised for their good performance, while units that are slow in achieving set targets should be reviewed and corrective actions should be suggested.

The management can identify factors that are slowing down performance and suggest ways of solving the issues and restoring normal performance.

The following are some of the advantages of an output/input budget:

Government entities rely on taxpayer’s money to fund their activities, which means that they need to show how the money is spent. Such a sense of responsibility makes employees accountable by quantifying a specific goal based on its importance and the amount of money allocated to it.

Taxpayers are interested in knowing if their funds have been used correctly; the government entity must make public its results.

An output/input budget allocates a larger share of the funds to departments or projects with the highest results based on the previous year’s performance. The practice can motivate departments to continually improve their performance, while those with the highest results will work hard to retain their top positions.

As a result, the organization will experience operational efficiency from one period to the next.

Below are a few drawbacks of output/input budgeting:

A performance budget is easy to manipulate, and employees can manipulate data to meet the specific targets that the management expects. This can influence the amount of funds allocated to the specific departments, as each department competes to outdo each other.

Organizations should put in place strong internal control systems to prevent manipulation of records by staff.

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.