Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The difference between the price paid for a target company and the target’s assessed market value

Acquisition premium is the difference between the price paid for a target company in a merger or acquisition and the target’s assessed market value. It represents the excess amount over the fair value of all identifiable assets paid by an acquiring company. The acquisition premium is also known as goodwill and is maintained on the acquirer’s balance sheet as an intangible asset, post-transaction.

The actual premium paid can depend on many factors, including the following:

In order to arrive at the acquisition premium, the acquiring company must estimate the real value of the target company. It can be done using enterprise value or equity valuation.

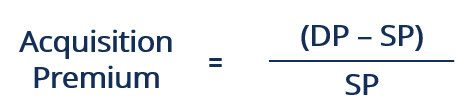

A simpler way to calculate the acquisition premium for a deal is taking the difference between the price paid per share for the target company and the target’s current stock price, and then dividing by the target’s current stock price to get a percentage amount.

Where:

Intuitively, it may not make sense that an acquiring company is paying a price that is higher than what the target company is worth.

It should be noted that the current price of the target company represents what it is worth through the lens of the market. However, an acquiring company may value the target company greater than the market does, often because of the strategic value that it may bring.

Some reasons that an acquiring company may pay a premium are as follows:

The most common motivation for a merger or acquisition is the creation of synergies, where the combined companies are more valuable than the sum of its parts. Synergies generally come in two forms, hard synergies and soft synergies.

Hard synergies refer to cost savings from economies of scale, while soft synergies refer to revenue increases from expanded market share, cross-selling, and increased pricing power.

The management of companies is usually under pressure to grow revenues continuously. Although it can be done organically, it may be faster to grow externally through mergers and acquisitions activity.

Combined companies may have fewer competitors when an industry is more concentrated. It gives the combined company a greater ability to influence market prices. Also, a combined company can control more aspects of the supply chain, reducing reliance on other stakeholders.

A target company, on its own, may be uncompetitive due to various reasons, such as poor management, lack of resources, or poor organizational structure. An acquiring company may have the belief that it can unlock hidden value through the reorganization of the target.

Diversification can be considered from the viewpoint of a company as a portfolio of investments in other companies. Therefore, the variability of cash flows from the company can be reduced if the company is diversified to other industries.

An acquirer may grow through M&A activity to pursue competitive advantages or obtain resources that it currently lacks but that a target company may have. They can be specific competencies or resources, such as an advanced research and development (R&D) team, a strong sales team, or other unique talents.

Through agency problems, management may be personally motivated to maximize the size of their company for greater power or more prestige.

In some cases, it may be beneficial for a profitable acquirer to acquire or merge with a target company with large tax losses, where the acquirer can immediately lower its tax liability.

A merger or an acquisition can be used as a strategic tool to extend the market reach internationally to different countries and markets. Less regulation and more uniform accounting standards will make such a reason more common for M&A deals in the future.

If the perceived value of any of the reasons above is greater than the market value of a target company, then an acquirer can be motivated to engage in an M&A transaction to acquire the target.

As mentioned earlier, the acquisition premium is recorded on the acquirer’s balance sheet as goodwill. The account includes intangibles, such as the value of the target’s brand name, stakeholder relations, reputation, and patents. Goodwill can be impaired or reduced when the market value of the intangible assets falls below the acquisition cost. Impairments result in a decrease in the goodwill account.

An acquirer can also theoretically purchase a target company for less than its market value, resulting in an acquisition discount and a negative goodwill balance.

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.