Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

When a party to a contract voluntarily surrenders a claim or a right

When a party to a contract voluntarily surrenders a claim or a right, it is known as a waiver. A written form of waiver is usually a legally binding provision in a contract wherein any party agrees to forfeit their right to a claim without imposing any liability on the other party.

Essentially, the giving up on the claim must be voluntary, and the waiver must free the other party to the contract of any liability. It means that the other party will be relieved of any obligation to pay.

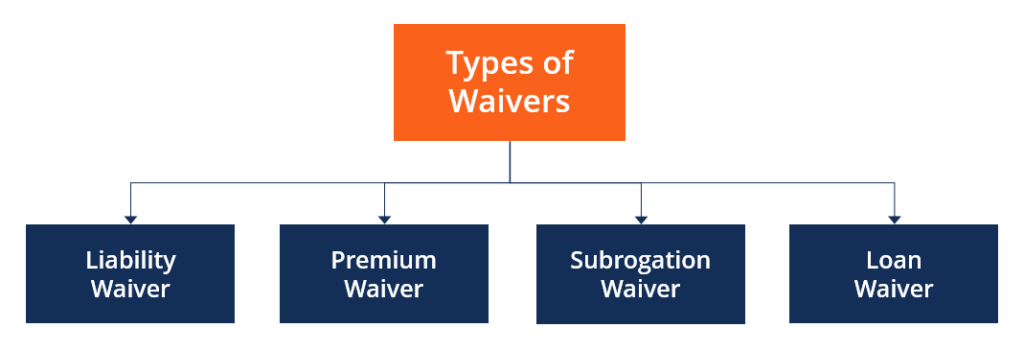

A waiver is applicable in various situations, some of which are explained below:

A waiver of liability is a provision in a contract by which any person participating in an activity forfeits the right to sue the organization conducting the activity in case of injuries. By signing a liability waiver form, a person acknowledges the risk associated with the activity they are about to perform and relieves the organization of all liability in case an untoward incident occurs.

For example, in recent times, restaurants and hotels require their guests to sign a COVID-19 liability waiver. Any guest signing the form relinquishes the right to hold the enterprise responsible if they contract the virus during their stay on the premises.

Included in an insurance policy, the premium waiver clause states that the insured can be relieved from paying the premium under certain conditions. Such conditions commonly include disabilities or death, which might render the insured unable to pay the premium.

The insurer may charge a higher premium if the insured opts for a waiver of premium to compensate for the risk of non-payment. For example, a premium waiver will ensure that the insurance company will still cover a house insured by its owner even after the owner suffers from a permanent disability and is unable to pay the premium.

Sometimes, the insured person or property might be harmed due to the actions of a third party, post which the insurer must pay for the damage. The right of subrogation allows the insurer to recover the loss by issuing claims against the third party. A waiver of subrogation takes away the insurer’s right to make a claim and puts them at a higher risk.

For example, a contract between a landlord and a tenant contains a waiver of subrogation in case the latter suffers any loss while staying on the premises of the landlord. If the tenant gets electrocuted due to faulty electrical wiring in the building, their insurance company cannot pursue the landlord to pay for damages. Since the insurance company assumes a higher risk, in such a case, it charges a higher premium from the insured.

When a lender voluntarily relieves a borrower of the obligation or liability to repay a loan, it is known as a loan waiver. The lender agrees to assume the burden of the loan, partially or fully, upon themselves. For example, the U.S. government sometimes waives an education loan through the Stafford Loan Forgiveness Program if the student fulfills certain service criteria. The criteria include volunteering in federal programs, such as the Peace Corps or military service.

As mentioned before, waiving a loan means that the lender will no longer ask for repayment from the borrower. The burden of the unpaid amount of the loan will be completely borne by the lender, and no attempt will be made by them to recover the amount.

The unpaid amount is usually deducted from their capital reserve, thus reducing the amount of capital surplus. The capital reserve is the account made out of profits earned through non-operational activities, or capital profits. A loan waiver is, therefore, a capital loss for the lender.

When borrowers fail to repay their loans, probably due to bankruptcy, the lender writes them off in order to clear their balance sheet. Writing off loans is an operational loss for the lender, and is shown as a loss in their P&L Statement. However, the lender still tries to recover the amount by auctioning the personal assets of borrowers. After a loan is written off, any subsequent recovery is entered as an operational profit for that year.

| Waiving Loans | Writing Off Loans |

|---|---|

| No further attempt to recover the amount | Consistent attempts to recover written off amount |

| A capital loss, deducted from the capital reserve | An operational loss, shown in the Statement of Profit and Loss |

| No subsequent recovery | Subsequent recovery entered as operational profit |

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: