Get In-Demand Finance Certifications

A clause that allows the insurer to force the insured to settle

A hammer clause (also referred to as a blackmail clause) is a clause relating to an insurance policy that allows the insurer to compel the insured to settle a claim. Settling a claim is much more beneficial than going to court because both parties involved avoid an assortment of different legal fees.

In legal terms, the word compel means to force someone to do something. So, in simpler terms, a hammer clause forces the insured to settle a claim with the insurer.

The insurer is an individual or company that provides insurance policies. The insurer enters into an insurance contract and is responsible for paying compensation. An example of an insurer would be the Insurance Corporation of British Columbia (ICBC).

The insured is an individual or company that is covered under an insurance policy. An example would be someone who pays monthly car insurance.

The hammer clause forces the insured to settle by placing a cap on the indemnification amount that is willing to be provided. Indemnification is a legal term for compensation for harm and/or loss.

The amount the indemnification cap is set to is decided by the insurer. In most cases, both the insured and the insurer may differ on what the indemnification cap should be. The insured may be responsible for their own defense costs if they do not decide to settle.

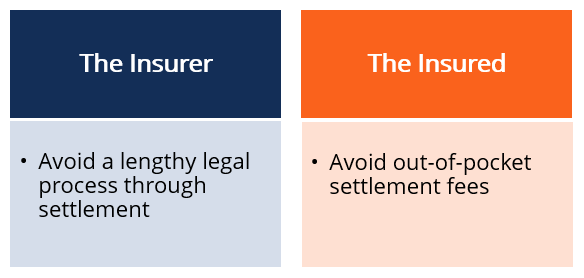

When faced with a hammer clause, both the insurer and the insured aim to capitalize on the best possible outcome for themselves. Each of their goals is shown below:

As mentioned, the insurer sets the indemnification amount they are willing to provide the insured. As such, the goal of the insurer is to reduce the amount of money they will owe in a settlement. If the insured is not satisfied with the amount presented by the insurer, the settlement is taken to court. Regarding legal fees, insurers do not incur them.

The insured wants to limit as many costs as possible. In a perfect world, the cap set by the insurer exactly matches the amount desired by the insured. The settlement fees incurred by the insured include legal fees and claim adjuster fees. The fees continue to grow a considerable amount as time goes on, so it is financially beneficial to finalize the settlement sooner rather than later.

For example, an individual is being sued for denting another person’s car. Because of insurance policies, the insurer is obligated to defend the insured (the individual who dented the other car) in court.

If the insurer believes they can avoid the lengthy defense process by offering a settlement, they will choose that option. It is undesirable for the insured because that would mean they would be liable to pay the settlement costs out-of-pocket. Enacting the hammer clause allows the insurer to force the insured to settle.

As mentioned, a hammer clause allows the insurer to force the insured to settle their claim out of court. Shown below are the number of legal costs avoided if a settlement is chosen:

As a whole, choosing a settlement can be a much more viable option due to avoided costs. It is important to compare the indemnification cap to the potential legal fees incurred if choosing to settle in court so that you may choose the most equitable option.

To keep advancing your career, the additional resources below will be useful: