Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Shares that are repurchased and canceled by a company

Retired shares are shares that are repurchased and canceled by a company. They don’t possess any financial value and are void of ownership in the company.

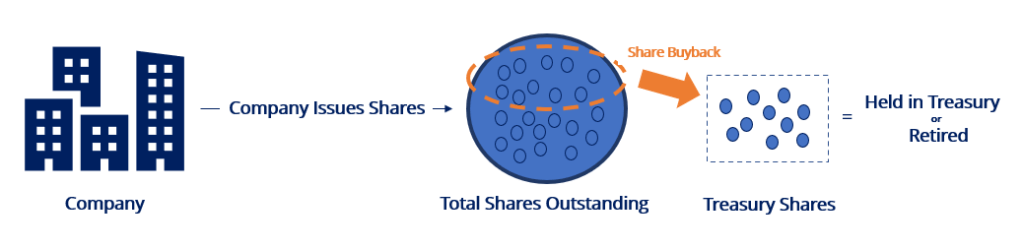

Companies issue shares to raise money and expand business operations. Subsequently, companies can choose to buy back shares from the market for numerous reasons, such as meeting stock option obligations, improving financial ratios, taking advantage of an undervalued share price, increasing ownership, and reducing dilution.

Repurchased shares either sit in the treasury (called treasury shares) or are retired (retired shares). Shares that sit in the treasury can be reissued at a future date, while retired shares cannot.

Retiring shares reduces the number of authorized shares by the company. Investors may get nervous if a company holds many authorized and unsold shares, as it gives a greater potential indication of share dilution in the future.

Retiring shares may signal a lower chance of future dilution. If a company wants to reissue the retired shares, a shareholder vote must be conducted.

These are two common methods to account for the buyback and retirement of shares:

The cost method is the most used method to account for the repurchase of shares. To retire shares under the cost method, two sets of journal entries are conducted:

Accounting for the Repurchase of Shares: Record the entire amount of the purchase in the treasury stock account. The cost method ignores the par value of the shares and the amount received from investors when the shares were originally issued.

Assume that Company A repurchases 10,000 shares of its stock at $10 per share (total consideration is $100,000). The shares come with a $1 par value.

From the journal entries above, the repurchased shares now sit in treasury and are considered treasury shares.

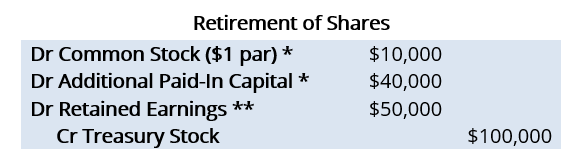

Accounting for the Retirement of Shares: Reverse the par value and additional paid-in capital associated with the original stock issue. Any remaining amount is further charged to paid-in capital (until the balance reaches zero) and retained earnings.

Assume that Company A now wants to retire the 10,000 shares that were purchased. The original per-share issue price was $5.

*When shares are retired, the common stock and additional paid-in capital accounts are debited for the amounts recorded when the stock was originally issued. When Company A issued 10,000 shares at $5 per share, the following journal entries would’ve been made:

**If the repurchase price is greater than the original issue price, as in our example, the difference is a debit to additional paid-in capital until its account balance reaches zero.

Once additional paid-in capital reaches zero, the remaining amount is debited to retained earnings. Here, we were not given the relevant details on the balance in additional paid-in capital, and, as a result, retained earnings were debited.

The opposite would be true if the repurchase price is lower than the original issue price.

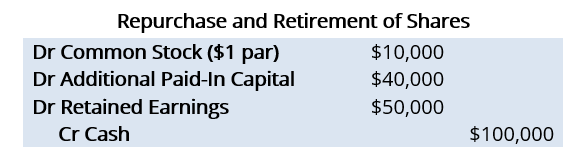

The constructive retirement method is used when it is assumed that the shares will not be reissued in the future. Under such a method, the journal entries for the repurchase and retirement of shares are conducted at the same time (i.e., only one set of journal entries are required). If we reuse the same example as above, the journal entries would be as follows:

The key difference between the constructive retirement method and the cost method is that the constructive retirement method does not involve the treasury stock account.

It is due to the constructive retirement method, assuming that the shares will not be reissued. Under the cost method, a treasury stock account indicates that the shares could be reissued at a later date.

Thank you for reading CFI’s guide to Retired Shares. To keep advancing your career, the additional resources below will be useful: