Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A component of shareholders’ equity that reflects the price investors are willing to pay above the par value of issued stock

Additional paid-in capital (APIC) is a component of shareholders’ equity that reflects the price investors are willing to pay above the par value of issued stock.

APIC can be thought of as the surplus amount or premium a company receives from stock issued in an initial public offering (IPO) or a follow-on offering over and above the shares’ par value. It is important to note that additional paid-in capital occurs only in the primary markets; in other words, when an investor buys shares directly from the company.

Transactions in the secondary market, or between shareholders after the IPO, do not result in cash for the company. As such, they are not included in additional paid-in capital. APIC can apply to both common and preferred stock.

In order to calculate APIC, you will need the following information:

APIC is derived from the difference in the issue price and par value, which will give you the premium per share resulting from the stock issue. The premium per share is then multiplied by the number of shares outstanding to give the company’s APIC value. The above relationship can be expressed by the following formula:

By applying the formula above to all public offerings, you will be able to determine the APIC of an organization.

Par value is a nominal amount a company assigns to a common or preferred share of stock. The par value is determined by a company’s management even before there is a market value for the security. In many cases, companies may issue no-par-value stock. However, in some jurisdictions a company is required to have a par value, which represents the lowest price a company can sell a share. Because of this, most companies assign a very low par value, such as $0.01 per share.

On the other hand, the issue price is reflective of investor expectations of the company’s valuation. The difference between the par value and what the market thinks a share is worth determines the additional paid-in capital in the above equation.

To frame our understanding of APIC, we will use a relatively recent real-world example. In early 2019, Beyond Meat Inc., a Los Angeles-based producer of plant-based meat alternatives, held its initial public offering.

Pre-IPO, Beyond Meat attributed a par value of $0.0001 per share, while the issue price was $25 per share. The number of common shares the company issued at IPO was 9.625 million. Putting it all together, the additional paid-in capital from common stock at Beyond Meat’s IPO would be:

APIC = ($25 – $0.0001) * 9,625,000

APIC = $240,624,037.50

Therefore, the cash collected as a result of additional paid-in capital at IPO attributed to common stock was approximately $240.6 million. The par value is a mere $962.50.

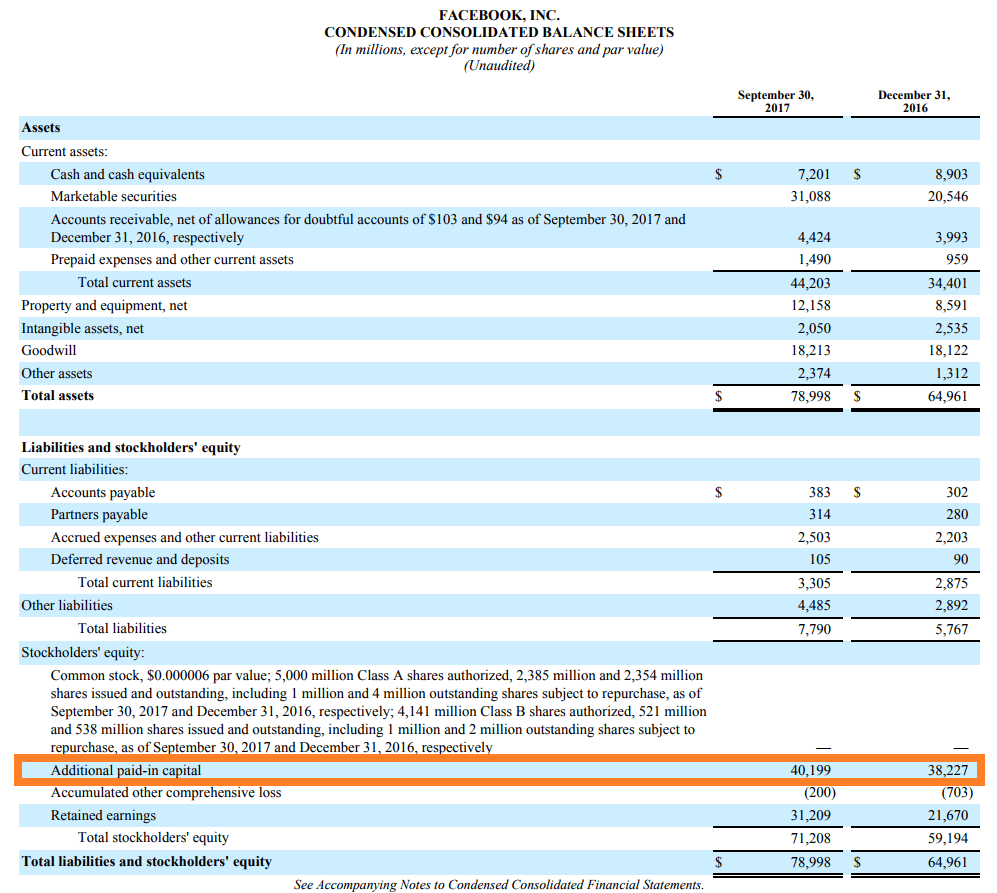

APIC is accounted for in shareholders’ equity and serves to counterbalance the increase in the cash account on the assets side of the balance sheet. Along with retained earnings, it is generally the largest component of shareholder equity.

In fact, additional paid-in capital will usually reflect a large majority of shareholder equity immediately after a company’s IPO, as retained earnings may have yet to accumulate.

Download CFI’s Excel template to advance your finance knowledge and perform better financial analysis.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.