Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The first sale of company shares to the public

An Initial Public Offering (IPO) is the first sale of stocks issued by a company to the public. Before an IPO, a company is considered a private company, usually with a small number of investors (founders, friends, family, and business investors such as venture capitalists or angel investors).

When a company goes through an IPO, the general public is able to buy shares and own a portion of the company for the first time. An IPO is often referred to as “going public,” and the underwriting process is typically led by an investment bank.

Companies that are looking to grow often use an Initial Public Offering to raise capital. The biggest advantage of an IPO is the additional capital raised.

The capital raised can be used to buy additional property, plant, and equipment (PPE), fund research and development (R&D), expand, or pay off existing debt. There is also an increased awareness of a company through an IPO, which typically generates a wave of potential new customers.

In addition, private investors/founding partners/venture capitalists can use an IPO as an exit strategy. For example, when Facebook went public, Mark Zuckerberg sold nearly 31 million shares worth US$1.1 billion. A public offering is one of the most common ways venture capitalists make a significant amount of money.

The top reason to go public… to raise money!

The first step in an Initial Public Offering is to hire an investment bank, or banks, to handle the IPO. Investment banks can either work together with one taking the lead, or one bank can work alone.

Next, everyone involved in the IPO – the management team, auditors, accountants, the underwriting banks, lawyers, and Securities and Exchange Commission (SEC) experts – attend a meeting to discuss the offering and determine the timing of the filing. Similar meetings happen throughout the entire underwriting process.

After the meeting, due diligence is required to be conducted on the company to make sure the registration statements are accurate. Tasks include market due diligence, legal and IP due diligence, financial and tax due diligence.

The end result of the due diligence is the S-1 Registration Statement. The information in the statement includes historical financial statements, key data, company overview, risk factors, and more.

A pre-IPO analyst meeting is held after the S-1 Registration Statement is filed to educate bankers and analysts about the company. Bankers and analysts are also briefed on how to sell the company to investors. A preliminary prospectus can also be drafted.

Pre-marketing is conducted to determine whether institutional investors like the sector and the company and the price they would likely be willing to pay per share. In conjunction with the internal valuation, a price range for the offering is set by the banks. The S-1 Registration Statement is amended with the price range.

After the pre-marketing work and S-1 Registration Statement is completed, the management team travels around to meet with investors and market the company. It is a very important process as orders for the number of shares by investors and the price they are willing to pay are determined. The price range may be further revised.

The management team will meet with the investment banks to decide on the final price of the deal based on the orders. If there are a lot of orders (oversubscribed), the company will price the shares higher.

Once the IPO is priced, the investment banks will allocate shares to investors, and the stock will start trading in the market for the public to buy and sell.

Although there are benefits to going public, there are notable drawbacks to consider as well. An Initial Public Offering (IPO) can take anywhere from six months to a year. During this time, the management team of the company is likely focused on the IPO, creating a potential for other areas of the business to suffer.

In the United States, public companies are monitored by the Securities and Exchange Commission (SEC). Public companies are made up of thousands of shareholders and are subject to rules and regulations. A board of directors must be formed, and auditable financial and accounting information must be provided quarterly.

Going public is an expensive process, which is why, historically, only private companies with strong fundamentals and high profitability potential go through an IPO. Lastly, the information of a public company is readily available online, which may be useful to competitors.

Investment bankers spend a lot of time trying to value the company going public. Ultimately, it will be the investors who decide what the company is worth when they decide to participate in the offering and when they buy/sell shares after it starts trading on the exchange.

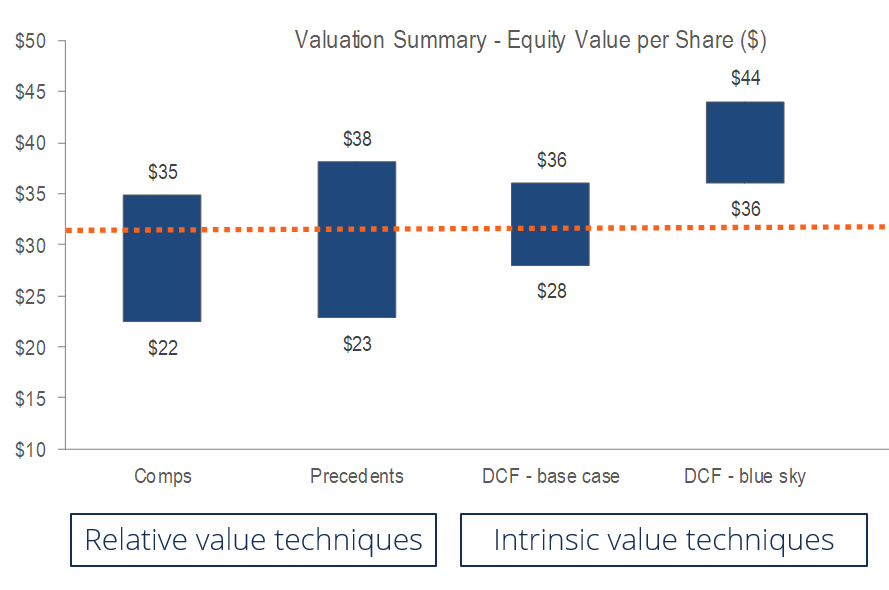

The main methods bankers use to value the company before it goes public are:

By combining these three methods, bankers are able to triangulate on what they think is a reasonable value an investor would be willing to pay for the business.

Valuation can be more of an art than a science, and for this reason, many IPOs have a lot of volatility in their first few days of trading.

To learn more, check out CFI’s business valuation techniques course.

Despite all the valuation work mentioned above, there is still a tendency for IPO underpricing to occur when companies go public (i.e., they are intentionally priced significantly lower than what the first-day trading price will be). For example, LinkedIn Corporation went public at $45 a share but traded as high as $122 at day’s end. This is often referred to as “leaving money on the table.”

Underwriting a public offering can be disastrous for a company. Assume Company A prices its one-million share IPO at $20 a share. If the shares end up trading at $40 a share, this would indicate that Company A received $20 million (1 million * $20) when it could’ve made $40 million (1 million * $40) if the IPO was not underpriced.

A popular theory in corporate finance as to why IPOs are underpriced can be illustrated by the following example:

Assume there are two categories of investors who invest in an IPO – insiders and the rest of the market (outsiders). Insiders know the actual value of the company and would stay away if it is overpriced. If the IPO is underpriced, insiders will purchase the shares.

Outsiders do not know the actual value of the company but know that the insiders know. With this knowledge, outsiders would follow suit with the action of the insider:

Thus, it is in the best interest of the issuer and its bank to underprice the offering.

Thank you for reading CFI’s guide to Initial Public Offering (IPO). To keep learning and advancing your career, the following resources will be helpful: