Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Re-acquisition of company’s outstanding shares from investors

Treasury stock, or reacquired stock, is the previously issued, outstanding shares of stock which a company repurchased or bought back from shareholders. The reacquired shares are then held by the company for its own disposition. They can either remain in the company’s possession to be sold in the future, or the business can retire the shares and they will be permanently out of market circulation.

Treasury stock is one of the various types of equity accounts reported on the balance sheet statement under the stockholders’ equity section as a contra-equity account.

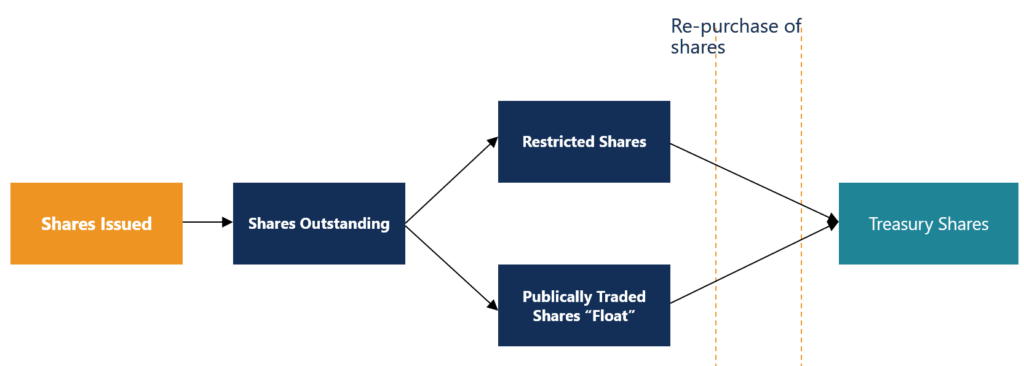

Every company is authorized to issue a certain number of shares. This is referred to as “shares outstanding,” or the total shares that exist for a company. Of those outstanding shares, some shares are restricted (meaning they cannot be traded unless certain conditions are met) while most shares are publicly traded (known as the “float”).

Treasury stocks are shares that were originally part of “shares outstanding” but that have been repurchased by the company.

There are several reasons why companies reacquire issued and outstanding shares from the investors.

Treasury stock is often a form of reserved stock set aside to raise funds or pay for future investments. Companies may use treasury stock to pay for an investment or acquisition of competing businesses. These shares can also be reissued to existing shareholders to reduce dilution from incentive compensation plans for employees.

The repurchase action lowers the number of outstanding shares, therefore, increasing the value of the remaining shareholders’ interest in the company. The reacquisition of stock can also prevent hostile takeovers when the company’s management does not want the acquisition deal to push through.

When the market is not performing well, the company’s stock may be undervalued – buying back the shares will usually boost the share price and benefit the remaining shareholders.

When treasury stocks are retired, they can no longer be sold and are taken out of the market circulation. In turn, the share count is permanently reduced, which causes the remaining shares present in circulation to represent a larger percentage of shareholder ownership, including dividends and profits.

If there is a sound motive for the buyback of stocks, the improvement of financial ratios may just be an after-effect of such good management decisions. This results in an increase in the return on assets (ROA) ratio and return on equity (ROE) ratio. This then illustrates positive company market performance.

A stock buyback, or share repurchase, is one of the techniques used by management to reduce the number of outstanding shares circulating in the market. It benefits the company’s owners and investors because the relative ownership of the remaining shareholders increases. There are three methods by which a company may carry out the repurchase:

The company offers to repurchase a number of shares from the shareholders at a specified price it is willing to pay, which is most likely at a premium or above market price. The company will also disclose the duration for which this offer is valid, and shareholders are welcome to tender their shares to the company should they be willing to sell at the specified price.

Direct buying of shares in the open market. When a company announces the repurchase of stocks, it often causes the share price to increase, which is perceived by the market as a positive outcome. The company then simply proceeds to purchase shares as other investors would on the market.

In a Dutch auction, the company specifies a range, and the number of shares it wishes to repurchase. Shareholders are invited to offer their shares for sale at their personally desired price, within or below this range. The company will then purchase their desired number of shares for the lowest cost possible, by purchasing from shareholders who have offered at the lower end of the range.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Treasury Stock. To keep advancing your career, the additional CFI resources below will be useful: