Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The removal of one-time, irregular, and non-recurring items from EBITDA

Adjusted EBITDA is a financial metric that includes the removal of various one-time, irregular, and non-recurring items from EBITDA (Earnings Before Interest Taxes, Depreciation, and Amortization).

The purpose of adjusting EBITDA is to get a normalized number that is not distorted by irregular gains, losses, or other items. It is frequently used in valuation by financial analysts, investment bankers, and other finance professionals.

The adjustments that are made to EBITDA can vary widely by industry, company time, and case by case. Some examples of items are that commonly adjusted for include:

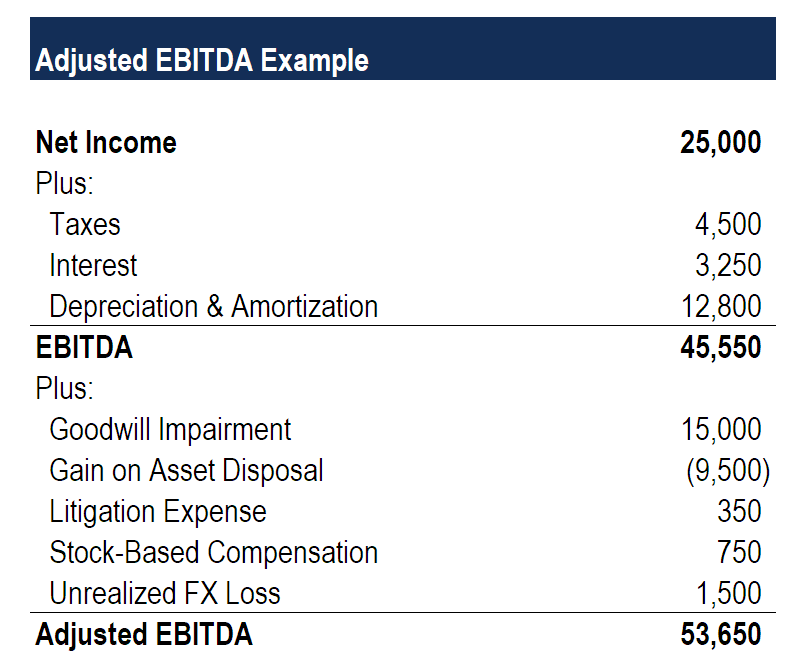

Here is an example of how to calculate the adjusted EBITDA of a hypothetical business. Below, we show the build-up to calculate regular EBITDA, and then the adjusted number. Following that is an explanation of each item on the list.

To arrive at the unadjusted figure, we start by taking a net income of $25,000 and adding back to it taxes of $4,500, plus an interest expense of $3,250, plus depreciation and amortization of $12,800. It produces an EBITDA of $45,550.

Moving on to the adjusted figure, we continue to add back more items, including a $15,000 goodwill impairment expense, the reversal of a $9,500 gain on the sale of a non-core asset, plus a one-time litigation expense, plus stock-based compensation of $750, plus an unrealized loss on foreign exchange (FX) of $1,500. The final result is an adjusted EBITDA of $53,650.

As you can see, there is a huge difference between the net income ($25,000), EBITDA ($45,550), and Adjusted EBITDA ($53,650).

There are many reasons to use Adjusted EBITDA; some are good, and some are not. Adjustments usually take place when a business is being valued for mergers and acquisitions (M&A) that are taking place, or when actual results are being compared to forecast/budget/guidance/expectations.

“Good” adjustments include items that are truly non-recurring and don’t reflect future expectations for the business. It makes sense to remove these items as accounting principles don’t smooth them out over time and can result in a significant earnings volatility.

“Bad” adjustments are items that are being removed for the purpose of inflating or manipulating financial results, or those that don’t fairly reflect the economic impact on a business.

For example, while stock-based compensation is a non-cash expense (and many analysts add it back), there is an economic impact on shareholders from the dilution they experience on the issuance of additional shares. This particular line item is quite debated, and you can read more about it from Prof. Aswath Damodaran at NYU Stern.

Adjusted EBITDA is most useful when valuing a business as part of a major corporate transaction, such as raising capital or mergers and acquisitions. The reason for this is that if a company is valued on a multiple such as EV/EBITDA, the impact of increasing the number is very large.

For example, if a business is valued at 8.5x EBITDA, then simply adding back $1 million of unusual or one-time expenses adds $8.5 million to the purchase price. This is why investment bankers and equity research analysts pay very close attention to these adjustments.

Thank you for reading CFI’s guide to Adjusted EBITDA. To continue learning and building your career, check out these relevant resources: