Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

What to beware of in financial statements

Non-cash expenses appear on an income statement because accounting principles require them to be recorded despite not actually being paid for with cash. The most common example of a non-cash expense is depreciation, where the cost of an asset is spread out over time even though the cash expense occurred all at once.

Here is an example of how a non-cash expense occurs:

As you can see, the $500 depreciation expense is actually a non-cash item, and the capital cost is recorded only once on the cash flow statement.

There are many types to watch out for, but the most common examples include:

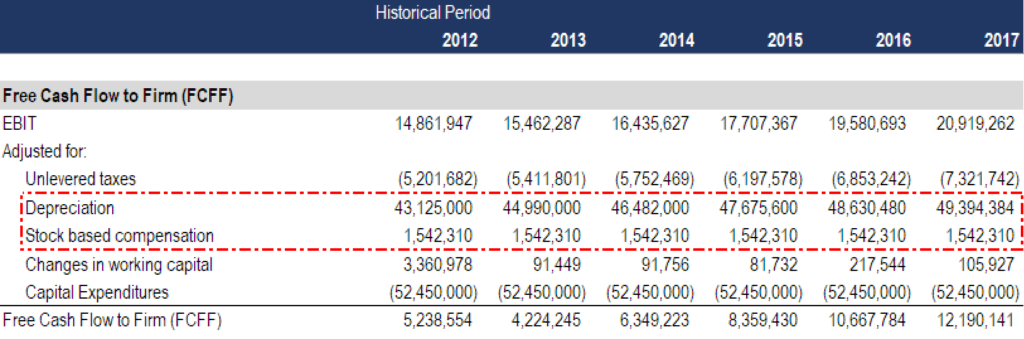

When performing a financial valuation of a company, an analyst typically performs a Discounted Cash Flow (DCF) analysis based on its Free Cash Flow (FCF). FCF is used because it demonstrates the true economic viability of a company.

Since analysts can’t use net income in a DCF model, they need to adjust net income for all the non-cash charges (and make other adjustments) to arrive at free cash flow.

Below is an example of how an analyst would make the above adjustments when building a financial model.

Source: CFI financial modeling courses.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading this guide to non-cash expenses and charges that require adjustment in financial modeling and valuation. CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: