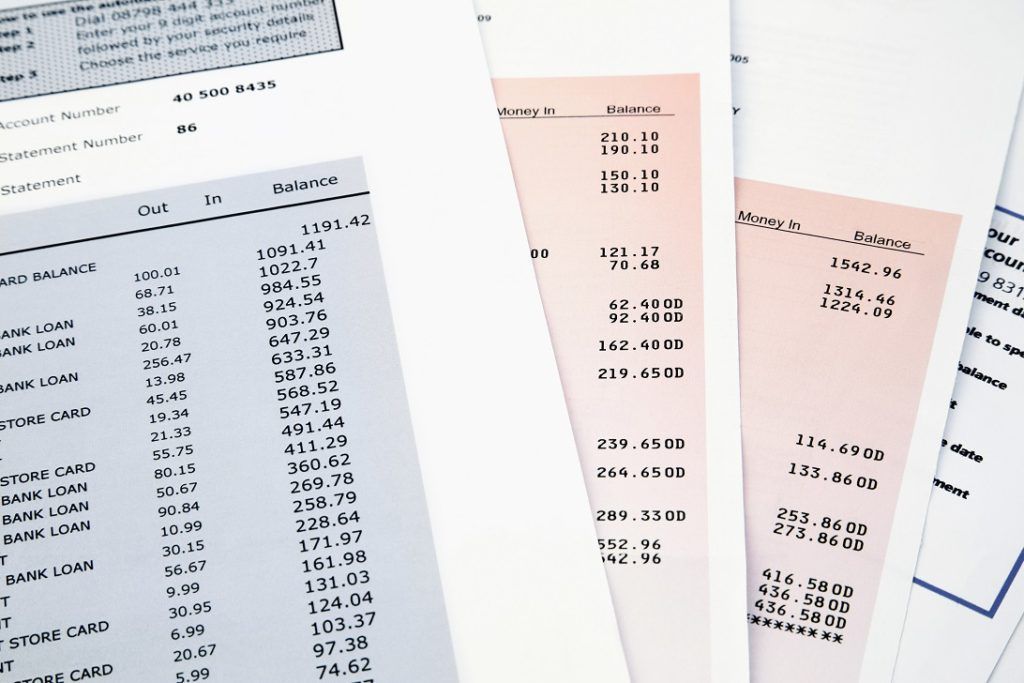

Bank Statement

A monthly financial document that provides a summary of the account holder’s activity

What is a Bank Statement?

A bank statement is a monthly financial document that provides a summary of the account holder’s activity. Bank statements are generally prepared by the bank for the account holder at the end of each month.

Bank statements can be found online via online banking or be obtained from a branch of the bank. They are also commonly known as account statements or transaction summary statements.

Breaking Down a Bank Statement

The top of a bank statement generally shows the name of the account holder along with sensitive information such as bank account number and branch number. It also contains a summary table that shows the time period, opening balance, deposits, withdrawals, and closing balance.

The closing balance is calculated as Opening Balance + Deposits – Withdrawals.

Below the account summary, the bank statement shows every transaction the account holder engaged in, along with the corresponding payees, dates, and amounts of the transactions. Most bank statements show transactions in chronological order.

By looking at a bank statement, one can see exactly how much, where, and when the account holder spent money. Account holders can get a good estimate of monthly revenues and expenses by analyzing their bank statements for the last few months. It can help with financial planning and budgeting.

What is an e-Statement?

An e-statement is the electronic equivalent of a bank statement. As mentioned above, account holders are given several options to access bank statements. Bank statements can be accessed in print form at a physical branch location or via the bank’s online banking system/email.

Due to their ease of accessibility and storage, e-statements are more common than print statements.

Why are Bank Statements Important?

Budgeting and Financial Planning

A bank statement is like a personal P&L statement. It allows account holders to keep track of their finances and plan for future expenditures. Bank statements are also extremely helpful for budgeting, as they allow account holders to decipher how much they are spending on different categories.

For example, an account holder can calculate their monthly expenditure on food by adding up individual transactions.

Reconciliation and Identification of Fraudulent Activities

Once the bank prepares a bank statement or e-statement at the end of the month, account holders are usually given 30-60 days to analyze the charges and reconcile their cash balance.

Since the bank statement contains all charges, along with the corresponding dates and payees, it can help account holders identify any fraudulent activity. For example, if the bank statement shows a charge for a transaction that the account holder did not engage in, they can contact the bank and request that they look at the fraudulent transaction.

Credit Verification

Bank statements can also be useful to analyze the creditworthiness of the account holder. Most banks and financial institutions require verification of bank statements for the last 2-5 years before giving loans to individual clients.

Banks use the individual’s bank statements and other credit documents to analyze the creditworthiness of the borrower. It applies to most types of loans, including residential mortgages, student loans, and loans for small businesses.

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep learning and advancing your career, the additional CFI resources below will be useful:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.