Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Additional information for individuals reading financial statements

Financial statement footnotes are used as additional information by individuals reading financial statements. Otherwise known as explanatory notes or notes to the financial statements, the footnotes help add supplementary information to help further explain the related information in the financial statements without clouding the primary information that the statements are trying to convey.

Footnotes are often quite long and help to clearly describe the smaller details that connect with specific parts of the financial statements. The financial statement footnotes provide greater information to specific portions of the statements, which helps improve the flow of information for the reader and makes sure the essential explanatory details are included.

Footnotes are mainly used by analysts reviewing the financial statements to give them a much more detailed and comprehensive outlook on the company’s financial situation. It helps the analysts understand the accounting policies and how they might affect the company’s underlying financial health.

Auditors will also use the financial statements and their footnotes to help understand the company’s financial position. Their findings within the audit will be based almost as heavily on the footnotes as the other core areas of the financial statements.

Footnotes also depend heavily on the accounting framework that is being followed for the specific company. For example, the financial statement footnotes will look different for a company that follows IFRS standards compared to US GAAP. Publicly held companies will require even more extensive financial statements and footnotes mandated by authorities like the Securities and Exchange Commission (SEC) in the United States.

Footnotes are an essential part of any financial statement. However, they come with a few disadvantages. Footnotes are required only to the point “beyond the legal minimum” to protect the company from liability. How footnotes are conveyed and which information is included is up to the discretion of management.

Some footnotes will be filled with accounting jargon, which may make the information conveyed difficult for the reader to understand. It could be to hide something from the public, and investors should be wary of any financial statements like them.

There is a long list of the different types of financial statement footnotes. Any information that is needed to clarify or add additional detail to a financial statement will be found in the footnotes.

Examples can include unexpected changes from the previous year, required disclosures, adjusted figures, accounting policy, etc. Footnotes may also contain notable future activities that are expected to have a significant impact on the company’s future.

Below is a list of some of the common footnotes found in a company’s financial statements. The list below is by no means comprehensive and just an example to showcase a few of the footnotes you might expect to see. Depending on the company and industry, the financial statements can include some very niche explanatory footnotes.

Again, the list above is only a shortlist of some common financial statement footnotes. The content of each footnote and the different explanatory notes will vary tremendously between companies and industries, so it is essential to read them whenever analyzing a company’s financials thoroughly.

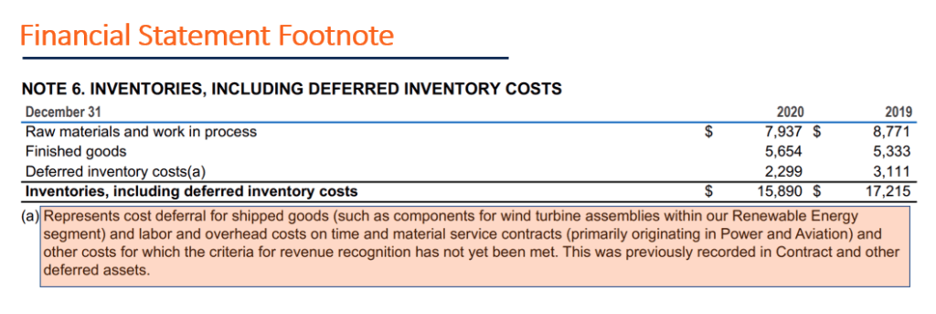

Below are some examples of financial statement footnotes pulled from General Electric Company’s financial statements (fiscal year ended December 31, 2020). Specific line items that require more explanation will almost always come with a related footnote to help clarify any missing information.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.