Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Assess the contribution of a particular product or business unit

Contribution analysis is used in estimating how direct and variable costs of a product affect the net income of a company. It addresses the issue of identifying simple or overhead costs related to several production projects.

Contribution analysis aids a company in evaluating how individual business lines or products are performing by comparing their contribution margin dollars and percentage. Direct and variable costs incurred during the manufacturing process are subtracted from revenue to arrive at the contribution margin. This is, therefore, a very crucial procedure or tool to manage the growth of a business.

To learn more, check out our Financial Analysis Fundamentals course.

The formula for contribution margin dollars-per-unit is:

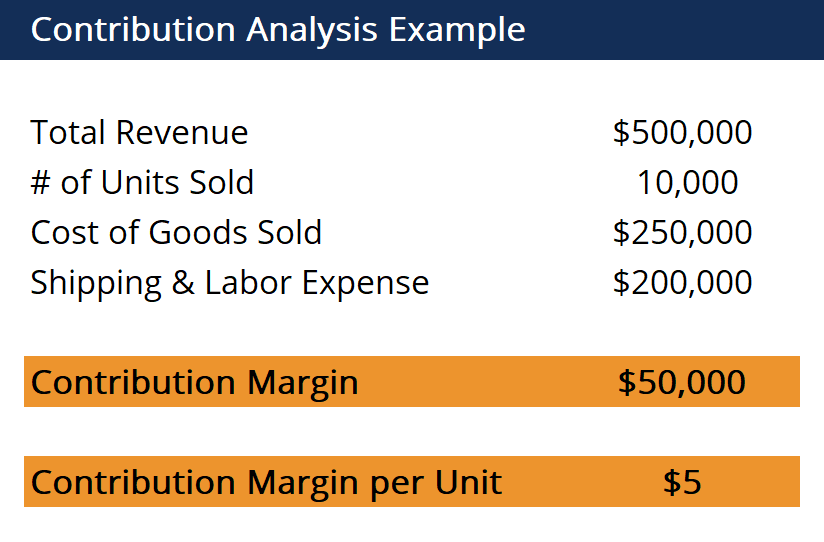

(Total revenue – variable costs) / # of units sold

For example, a company sells 10,000 shoes for total revenue of $500,000, with a cost of goods sold of $250,000 and a shipping and labor expense of $200,000.

The contribution margin per shoe is ($500,000 – $250,000 – $200,000) / 10,000

Contribution = $5.00 per shoe

Contribution analysis helps compare how individual products are profitable to the company and is easy to use.

The significance of contribution analysis is that it indicates the profitability of each product and helps you understand the various components and specific external and internal factors that influence a company’s income, and it utilizes existing information.

Some disadvantages of contribution analysis are that its assumptions are unrealistic:

Thank you for reading CFI’s guide to Contribution Analysis. To learn more, see the CFI resources listed below and check out our Financial Analysis Fundamentals course.