Evidence in an Audit

Information that is collected in the review of an entity’s financial transactions to certify the financial statements as being fairly represented

What is Evidence in an Audit?

Evidence in an audit is information that is collected and required in the review of an entity’s financial transactions, balances, and internal controls to certify the financial statements as being fairly represented.

Evidence is used by auditors and certified public accountants (CPAs) in determining whether an audit results in an unqualified or clean opinion. An unqualified opinion means that the auditor has found reasonable assurance that an entity’s accounting statements are not materially misstated.

Auditing Explained

Auditing is the process of checking and verifying an entity’s financial statements for accuracy and fairness. Transactions that are recorded within the financial records of an entity must be a fair representation of the entity’s financial positioning and actual operations.

Financial statements are generated internally within a company. The process introduces a level of risk for manipulation or fraudulent behavior from insiders who can alter information when preparing the financials. Auditing is an essential process that ensures that manipulation or fraudulent behavior is not being conducted.

Audits are also important in ensuring that an entity is complying with relevant accounting standards, be it the International Financial Reporting Standards (IFRS), Generally Accepted Accounting Principles (GAAP), or other applicable accounting standards.

Public companies are required to provide fully audited financial statements to owners and shareholders periodically. Therefore, auditing is important in maintaining the transparency and accuracy of the financial records to protect shareholders.

Evidence in an Audit Explained

Evidence in an audit protects investors by allowing auditors to issue accurate, transparent, and independent audit reports. Within the United States, the Public Company Accounting Oversight Board (PCAOB) created the Sarbanes-Oxley Act of 2002 to enforce proper auditing and in response to the Enron/Arthur Andersen scandal.

In the Enron scandal, billions of dollars of debt were hidden by using several accounting loopholes. The auditors, Arthur Andersen, allowed the fraudulent behavior to occur.

Evidence is a very important aspect of auditing. Financial statements can easily be misstated. It is required by auditors to verify the truth within financial records.

Evidence provides support and verifies financial information that is provided by internal members of an entity, such as management and internal finance teams. On the other hand, evidence can contradict the information that is provided by internal members, and it is an indication of errors or fraud.

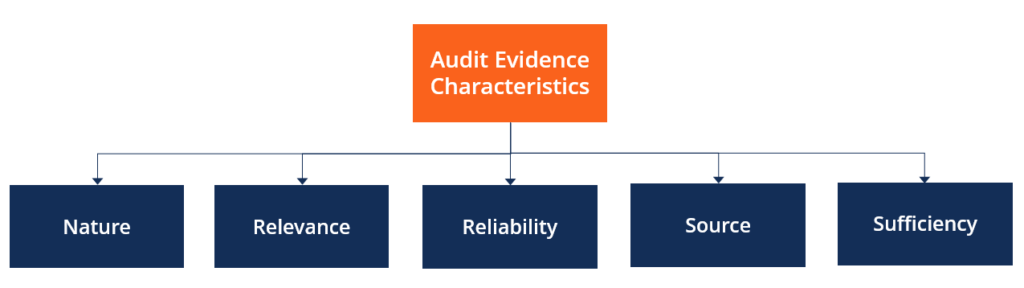

Characteristics of Evidence in an Audit

Evidence in an audit requires a few characteristics to be considered valid. The characteristics are as follows:

- Nature refers to the type of information received. It can be received in many forms – presentations, orally, or through physical records.

- Relevance refers to the pertinence of the information to provide an opinion.

- Reliability refers to determining whether the material can be trusted or relied upon to form an opinion. The source of the information needs to be considered.

- Source refers to whether the accounting evidence was obtained directly from the audited company or an external source. External source information is preferable since it is less subject to manipulation than internally sourced information.

- Sufficiency refers to whether the information provided is enough to provide an opinion or make an accurate judgment.

Examples of Evidence in an Audit

Evidence in an audit is collected to complete the auditing process. Some examples include:

- Bank statements

- Bank accounts

- Transaction records

- Management accounts

- Payrolls

- Billing invoices

- Receipts

- Inventory counts

The compilation of the items of evidence is used to conclude whether financial statements have been accurately presented.

Evidence in an Audit Example

Consider a company that has enlisted the auditing services of a professional services firm to audit its financial statements for a fiscal year. The company has prepared its financial statements and will rely on the professional services firm to provide a fair opinion.

The professional services firm will request information regarding the company’s revenues, expenses, and bank balances. For compiling accurate and reliable information, the auditing team requests all sales receipts, invoices, and a physical examination of inventories.

All bank statements and balances are collected from the company’s bank as well. All of the information is considered auditing evidence for the audit process.

Related Readings

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.