Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A finance lease is a lease agreement where the lessee effectively controls and uses an asset while assuming most of the risks and rewards of ownership, even though legal ownership may not transfer immediately. For accounting purposes, a finance lease is treated similarly to purchasing an asset using borrowed funds, meaning both an asset and a lease liability are recorded on the balance sheet.

In accounting standards such as U.S. GAAP (ASC 842), the term finance lease replaced the older term capital lease. Under these standards, finance leases are recognized on the balance sheet and expensed through amortization of the asset and interest on the lease liability, rather than as a single lease (rent) expense.

The main difference between a finance lease and an operating lease is how lease costs are recorded on the income statement. Finance leases split costs into amortization and interest, similar to buying an asset with debt, while operating leases record a single lease expense, similar to renting an asset.

Both finance and operating leases appear on the balance sheet under Generally Accepted Accounting Principles (GAAP) in the U.S. However, their expense recognition and financial impact differ as follows:

The key difference between finance lease accounting in U.S. GAAP and IFRS is that IFRS uses a single lessee accounting model, while GAAP distinguishes between finance and operating leases. As a result, all lessee leases under IFRS are treated like finance leases on the income statement, whereas under GAAP, income statement treatment depends on lease classification.

The table below summarizes the main differences in how finance leases are accounted for under IFRS and U.S. GAAP.

| Lease Classification | Single lease model; all leases treated like finance leases | Two types: finance leases and operating leases |

| Balance Sheet Treatment | Right-of-use asset and lease liability recognized for all leases | Right-of-use asset and lease liability recognized for both lease types |

| Income Statement Treatment | All leases: amortization + interest | Finance leases: amortization + interest |

| Cash Flow Treatment | Principal: Financing cash outflow | Operating leases: single lease expense |

| Comparability Across Companies | Interest: Operating or financing cash outflow (policy choice) | Principal: Financing cash outflow (finance leases only) Interest: Operating cash outflow |

| Comparability Across Companies | Higher due to uniform lease expense treatment | Lower, due to mixed lease expense treatment |

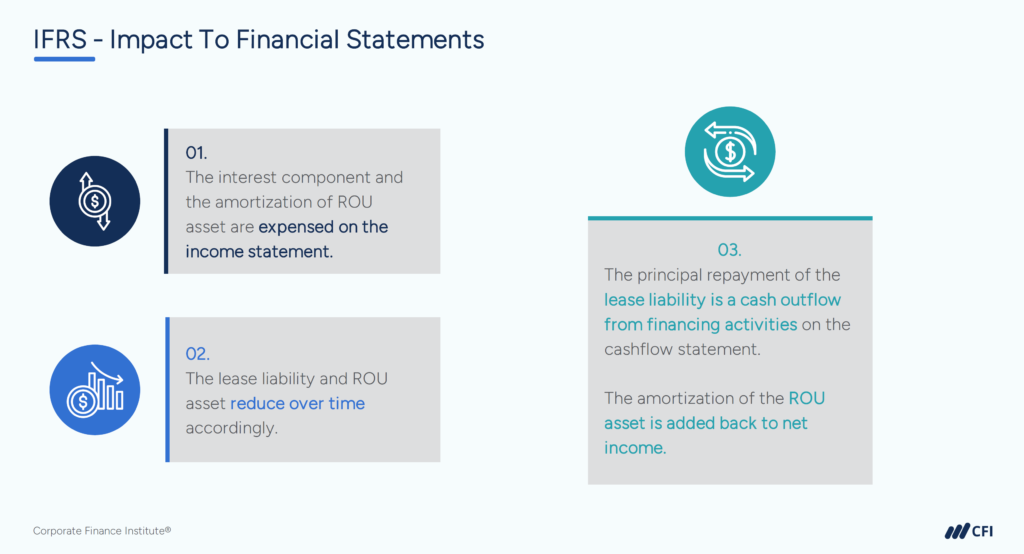

Under IFRS, lessees apply a single accounting model to most leases, recognizing a right-of-use asset and lease liability with expenses split into amortization and interest. Under GAAP, lessees classify leases as either finance or operating, which determines how lease costs appear on the income statement.

IFRS requires all lessee leases to recognize amortization and interest expense. Under U.S. GAAP, only finance leases use this approach, while operating leases recognize a single lease expense.

Under IFRS, principal repayments are financing cash flows, while interest expense may be classified as operating or financing. Under U.S. GAAP, interest expense is an operating cash flow, and principal repayments are financing cash flows for finance leases.

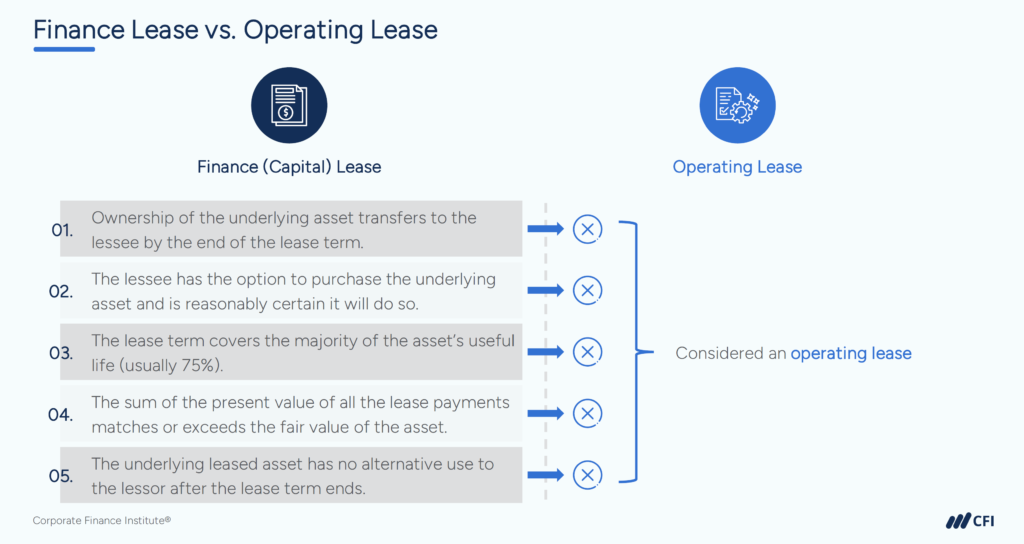

The four criteria for a finance lease are ownership transfer, bargain purchase option, lease term, and present value of payments. If any one of these criteria is met, the lease must be classified as a finance lease:

There is also a fifth criterion under updated US GAAP: if the asset is so specialized that it has no alternative use to the lessor at the end of the lease term, it is also deemed a finance lease.

If none of these criteria are met, the lease is classified as an operating lease.

In a finance lease, the lessee records both the leased asset and a matching lease liability at inception, then recognizes amortization and interest expense over the lease term—just like an asset purchased with a loan. This example shows how that treatment works in practice using leased equipment.

Suppose a company acquires equipment with a fair value of $2 million through a finance lease rather than purchasing it outright. The lease provides 100% financing over 10 years with a 6% interest rate and straight-line amortization of the asset.

At lease inception, the company records the equipment as a non-current asset (PP&E) at $2 million and recognizes an equal lease liability, split between current and long-term portions.

Over time, the asset is amortized, interest expense is recognized on the outstanding liability, and lease payments reduce the principal balance.

Finance Lease Example – Year 1 Snapshot

| Item | Amount (USD) | What This Represents |

| Fair value of equipment | $2,000,000 | Value of the leased asset |

| Initial lease liability | $2,000,000 | Present value of lease payments at inception |

| Lease term | 10 years | Period over which the asset is used |

| Interest rate | 6% | Rate applied to the lease liability |

| Annual amortization | $200,000 | $2,000,000 ÷ 10 years |

| Year 1 interest expense | $120,000 | 6% × $2,000,000 |

| Total Year 1 expense impact | $320,000 | Amortization + interest |

Summary:

A finance lease is a long-term agreement where the lessee uses an asset and takes on most of the risks and rewards of ownership. For accounting purposes, finance leases are treated like a financed purchase. Companies record finance leases on the balance sheet as assets and corresponding lease liabilities.

Another name for a finance lease is capital lease. “Capital lease” is a historic term used until 2018 when the term was changed to “finance lease” under U.S. GAAP standards.

To determine if a lease is finance or operating, assess whether it effectively works like a purchase. Under U.S. GAAP, a lease is treated as a finance lease if it transfers ownership, includes a bargain purchase option, covers most of the asset’s useful life, or has payments that equal most of the asset’s fair value.