Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A financial statement line item that occurs on financial statements of a firm on an irregular basis

A one-time charge, or non-recurring item, is a line item that is reported on the financial statements of a firm on an irregular basis. It is unrelated to a firm’s normal business operations and arises from unexpected events like lawsuits, layoffs, asset sales, etc.

It is important to recognize and highlight a one-time charge because it can distort the financial picture and significantly change the results of important analyses like financial statement forecasting and valuation.

It is common for management to use one-time charges to understate or overstate the financial performance to change investors’ perception of the company. In the following sections, we will see some examples of misuse and what can be done to deal with one-time charges.

Sometimes, a company will boost its earnings by including an unusual gain within a regular line item on the income statement. One way is to include investment income in the total revenues.

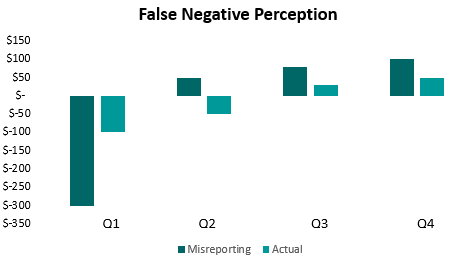

Example

Airline companies are often involved in fuel hedging to control their costs. Sometimes, hedging activities generate large profits. A company may decide to include such profits in its revenue numbers even though fuel hedging is not its core business.

A company can misuse one-time charges to gain important performance metrics by manipulating one of its components.

Example

The P/E ratio comprises two components: price P and earnings-per-share E. The company cannot control the price as it is determined by the market, but it can reduce its earnings per share to inflate the P/E ratio. It can do this by writing down assets or aggressively booking expenses for one period.

A company may not always overstate performance. It can create a false one-time charge by aggregating most of their expenses in one period, say a quarter. This creates a false perception of a better future for the company, as other quarters will look like improvements from the previous performance, which was intentionally understated. This is sometimes referred to as sandbagging.

A company may correctly report a one-time charge on one statement but improperly report it on another.

Example

A company reports a one-time gain separately on the income statement, which makes it transparent to any reader of the financial statements. However, it then includes the increased net income on the income statement and uses it without an adjustment on the cash flow statement. It can easily mislead investors who do not examine all statements closely. A better way to report the one-time charge is to report it separately on the cash flow as well.

The above examples are only a few ways in which a one-time charge may be misused by a company. There are a lot of possibilities, and it is hard to document every instance of such misreporting. However, one can take certain measures to minimize the distortion. Some of the measures are:

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: