Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

Learn about the different types of interest

In this article, we will discuss simple interest vs compound interest and illustrate the major differences that can arise between them. Interest payments can be thought of as the price of borrowing funds in the market. They are paid by the borrower to the lender with the payment made at the end of the loan period. Interest payments are usually calculated as a proportion of the principal that the borrower borrowed from the lender.

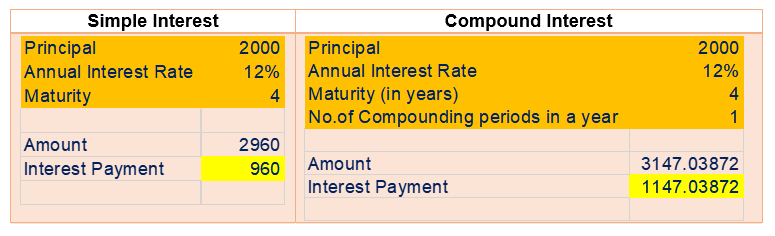

Simple interest calculates the total interest payment using a fixed principal amount. The interest that is accrued over time is not added to the principal amount. Consider the following example:

An investor invests $2,000 in a 4-year term deposit paying simple interest of 12%.

Total Interest Earned = Principal * Interest Rate * Time

= $2,000 * 12% * 4 = $960

Average Annual Interest Earned = Total Interest Earned / Time

= $960 / 4 = $240

Total Amount Repaid = Principal + Total Interest

= $2,000 + $960 = $2,960

Compound interest calculates the total interest payment using a variable principal amount. The interest that is accrued over time is added to the principal amount. For example, the interest for the first year is calculated as a proportion of the initial principal. The interest amount is then added to the initial principal, and the interest for the second year is calculated as a proportion of the revised principal. Consider the following example:

An investor invests $2,000 in a 4-year term deposit paying an annual interest of 12% with interest compounded annually.

Where:

Total Interest Earned = $2,000 * [(1 + 12%)4 – 1] = $1,147.04

Average Annual Interest Earned = Total Interest Earned / Time

= $1,147.04 / 4 = $286.76

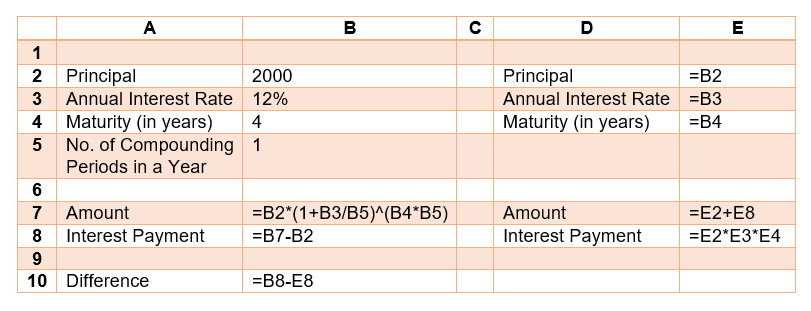

The following Excel spreadsheet can be used to illustrate the large differences between simple interest and compound interest payments:

In the example above, interest was compounded on an annual basis. However, we could’ve just as easily compounded on a semi-yearly or a quarter-yearly basis. In fact, we could’ve also compounded the interest every day.

Continuous compounding recalculates the principal on a continuous basis. Continuously compounded interest can be found using the following formula:

Where:

Continuing with the example above, if $2,000 is lent out for 4 years at an annual interest rate of 12% and the interest is compounded continuously, the total interest earned is $1,232.15. The result can be verified by setting the number of compounding periods in the Excel spreadsheet to a very large number (such as 100,000).

Thank you for reading CFI’s guide on Simple Interest vs Compound Interest. To keep advancing your career, the additional CFI resources below will be useful: