Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The rate of interest after taking into account the effects of compounding to normalize the interest rate

The Annual Equivalent Rate (AER) is the rate of interest after taking into account the effects of compounding to normalize the interest rate. The AER is the actual interest rate an investment, loan, or savings account will yield after accounting for compounding.

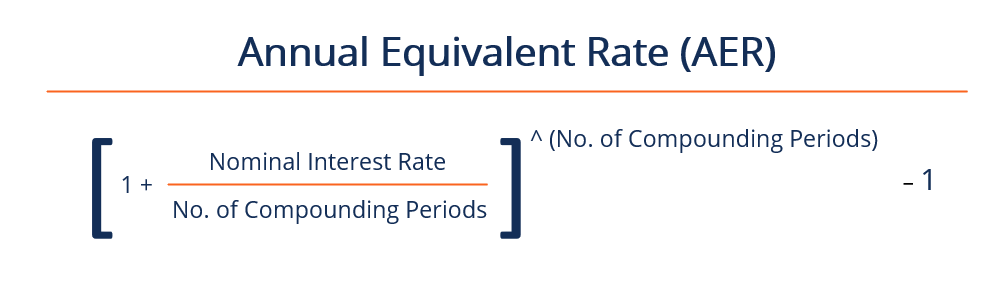

The formula for the annual equivalent rate is given below:

The annual equivalent rate is used to compare the interest rates between loans or investments with different compounding periods, such as weekly, monthly, half-yearly, or yearly. Therefore, it can be used by both an individual looking for the best savings account or an investor comparing bond yields.

The AER is crucial in finding the true return on investment (ROI) from interest-bearing assets. The nominal rate, or the stated rate, can be materially different than the AER due to the effects of compounding. It means that the AER is always higher than the nominal rate when considering compounding.

The table below visualizes the potential differences in the annual equivalent rate and the nominal rate with different compounding frequencies:

| Annual Equivalent Rates of Different Compounding Frequencies | |||||

| Nominal Interest Rate | Semi-Annually | Quarterly | Monthly | Weekly | Daily |

| 1% | 1.0025% | 1.0038% | 1.0046% | 1.0049% | 1.0050% |

| 2% | 2.0100% | 2.0151% | 2.0184% | 2.0197% | 2.0201% |

| 3% | 3.0225% | 3.0339% | 3.0416% | 3.0446% | 3.0453% |

| 4% | 4.0400% | 4.0604% | 4.0742% | 4.0795% | 4.0808% |

| 5% | 5.0625% | 5.0945% | 5.1162% | 5.1246% | 5.1267% |

| 6% | 6.0900% | 6.1364% | 6.1678% | 6.1800% | 6.1831% |

| 7% | 7.1225% | 7.1859% | 7.2290% | 7.2458% | 7.2501% |

| 8% | 8.1600% | 8.2432% | 8.3000% | 8.3220% | 8.3278% |

| 9% | 9.2025% | 9.3083% | 9.3807% | 9.4089% | 9.4162% |

| 10% | 10.2500% | 10.3813% | 10.4713% | 10.5065% | 10.5156% |

| 15% | 15.5625% | 15.8650% | 16.0755% | 16.1583% | 16.1798% |

| 20% | 21.0000% | 21.5506% | 21.9391% | 22.0934% | 22.1336% |

| 25% | 26.5625% | 27.4429% | 28.0732% | 28.3256% | 28.3916% |

For example, let’s say Bond A offers a semi-annual coupon rate of 3%. The nominal rate of the bond is 6% since it is two 3% coupons. However, the AER of the bond will be higher given that interest is paid out two times a year. Therefore, the AER of the bond will be calculated as:

AER = (1+ (0.06 / 2 )^2)) – 1 = 6.09%

Bond B, on the other hand, offers a quarterly coupon rate of 1.5%. The nominal rate of the bond is still 6%. However, the AER will be even higher, as the coupons are paid out four times a year. Therefore, the AER of the bond will be:

AER = (1+ (0.06/4)^4)) – 1 = 6.14%

After analyzing the AER of the two bond options, a rational investor will select Bond B, assuming all else equal, even though both bonds are the same from face value.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: