Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A payment towards the total principal amount owed

A principal payment is a payment toward the original amount of a loan that is owed. In other words, a principal payment is a payment made on a loan that reduces the remaining loan amount due, rather than applying to the payment of interest charged on the loan. In accounting and finance, a principal payment applies to any payment that reduces the amount due on a loan.

Bond Principals are further analyzed on CFI’s Fixed Income Fundamentals Course.

Understanding the components of a loan is very important. Every loan comprises two components – the principal and the interest. The principal is the amount borrowed, while the interest is the fee paid to borrow the money.

Consider an individual who saved $400,000 to pay for a $1,000,000 home. They would need to borrow $600,000 from the bank to complete the transaction. The $600,000 is the principal amount – the money borrowed. A bank may require 5% annual interest on the principal amount – the fee paid to borrow the money.

The individual in the situation above would need to make an annual total payment that consists of both principal and interest payments. The principal payment goes to reducing the outstanding principal amount due, while the interest payment goes to paying the fee to borrow the money.

There are generally two types of loan repayment schedules:

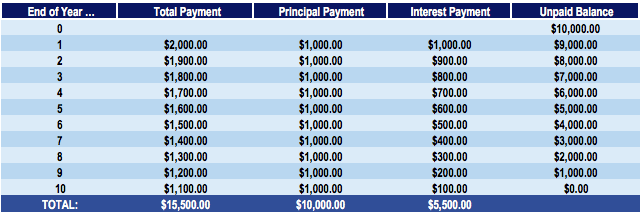

In an even principal payment loan, the principal payment amount is the same every period. Consider John, who takes a $10,000 loan with a 10% annual interest over 10 annual payments. The loan repayment schedule would look as follows:

In the loan repayment schedule above, the loan amortizes over 10 years with even principal payments of $1,000. In 10 years, the unpaid balance is $0.

The principal payment each year goes to reducing the unpaid balance. Since this amount each year is $1,000, the unpaid balance is reduced by $1,000 yearly. The interest payment is calculated on the unpaid balance. For example, the end of year one interest payment would be $10,000 x 10% = $1,000. Note that while the payment of principal remains the same, the total payment due each year, including interest, changes.

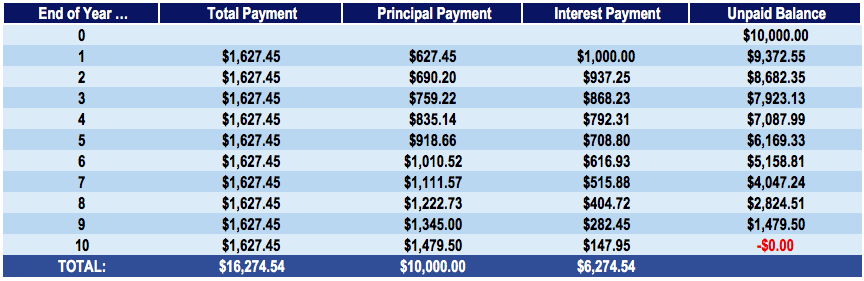

In an even total payment loan, the total payment amount is the same every period. Consider John, who takes a $10,000 loan with a 10% annual interest over 10 annual payments. The loan repayment schedule would look as follows:

In the loan repayment schedule above, the loan amortizes over 10 years with even total payments of $1,627.45. In 10 years, the unpaid balance is $0.

As opposed to an even principal payment schedule, the amount paid to principal here increases yearly. This is due to much of the initial total payment going toward paying interest rather than principal. In the first year, the amount of interest would be $10,000 x 10% = $1,000. With a total payment of $1627.45, the unpaid principal balance is only reduced by $1627.45 – $1,000 = $627.45. In such a schedule, interest payments decrease and payments on the principal increase over time.

Over the amortization of the loan, the total of payments in an even principal payment schedule is $15,500 while the total payment in an even total payment schedule is $16,274.54. This indicates that by repaying a higher principal amount each year, an individual saves money over the amortization of the loan.

A higher principal payment on a loan reduces the amount of interest owed and, in turn, reduces the total amount paid over the life of the loan. Therefore, principal payments play a significant role in the amount an individual must pay over the lifetime of a loan.

Thank you for reading CFI’s guide to Principal Payment. To keep learning and advancing your career, the following CFI resources will be helpful:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.